by Aussie Firebug | Jul 17, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

Super quick update for June.

It has mostly been Groundhog Day for us during this cold Victorian month.

Family, business, gym, Jiu-Jitsu and House of the Dragon every week.

In June, I hired my first full-time employee for my data company, which is exciting. The junior data engineer helps relieve some pressure on me to fix every issue and aligns with my vision of building a small team to solve problems and have fun with.

Lifestyle businesses can be a lot of fun, but they can also end up consuming all your spare time, which I’ve worked hard to free up through passive income. I found a great book to tackle this called Buy Back Your Time by Dan Martell.

I love running the data company and being part of the new co-working space in town. However, I don’t want these activities to take over my life. Hiring people to handle jobs I don’t love doing is a good solution to combat this.

Net Worth Update

Not much to report on here. Decent month overall, but the cash reserves took a hit.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

.

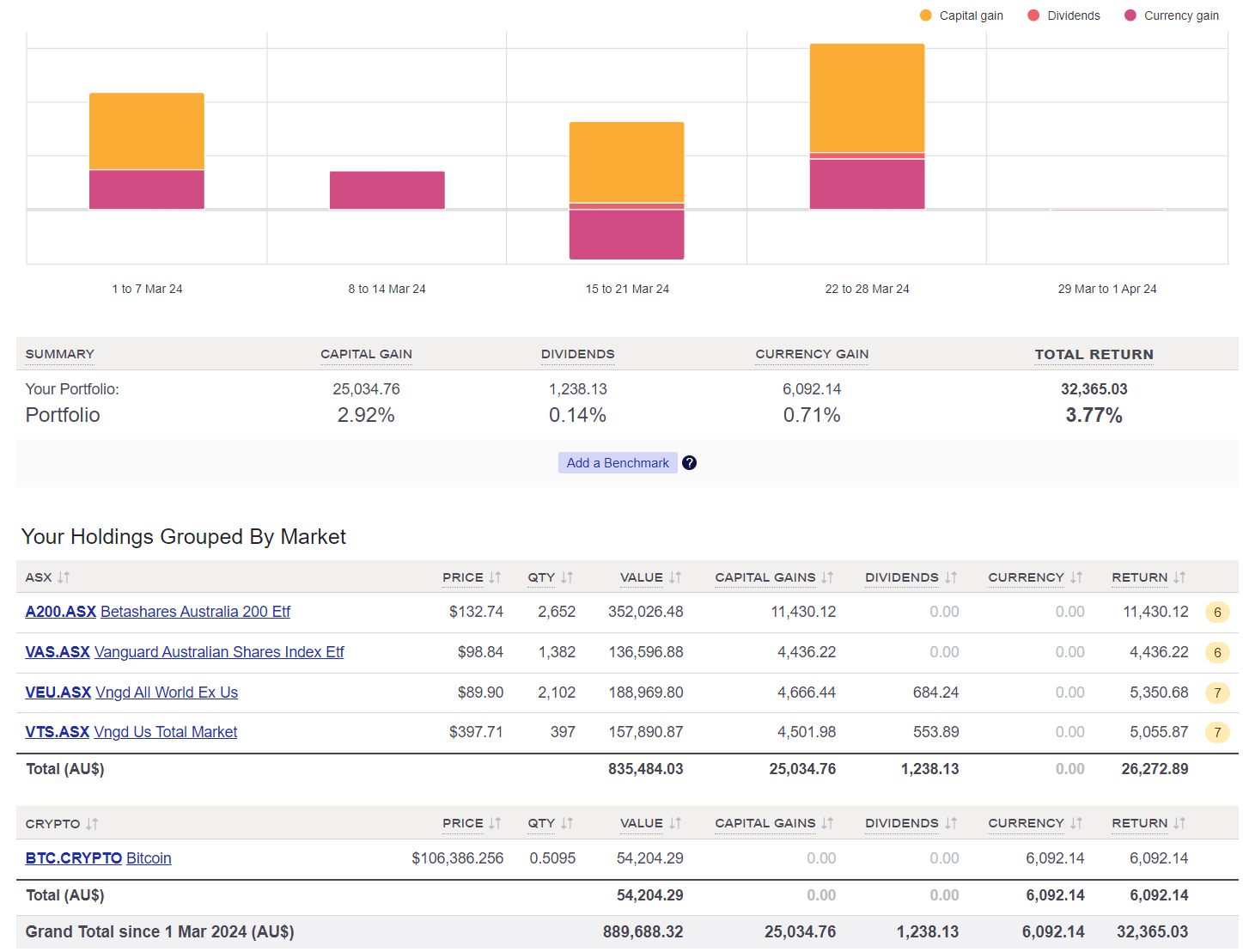

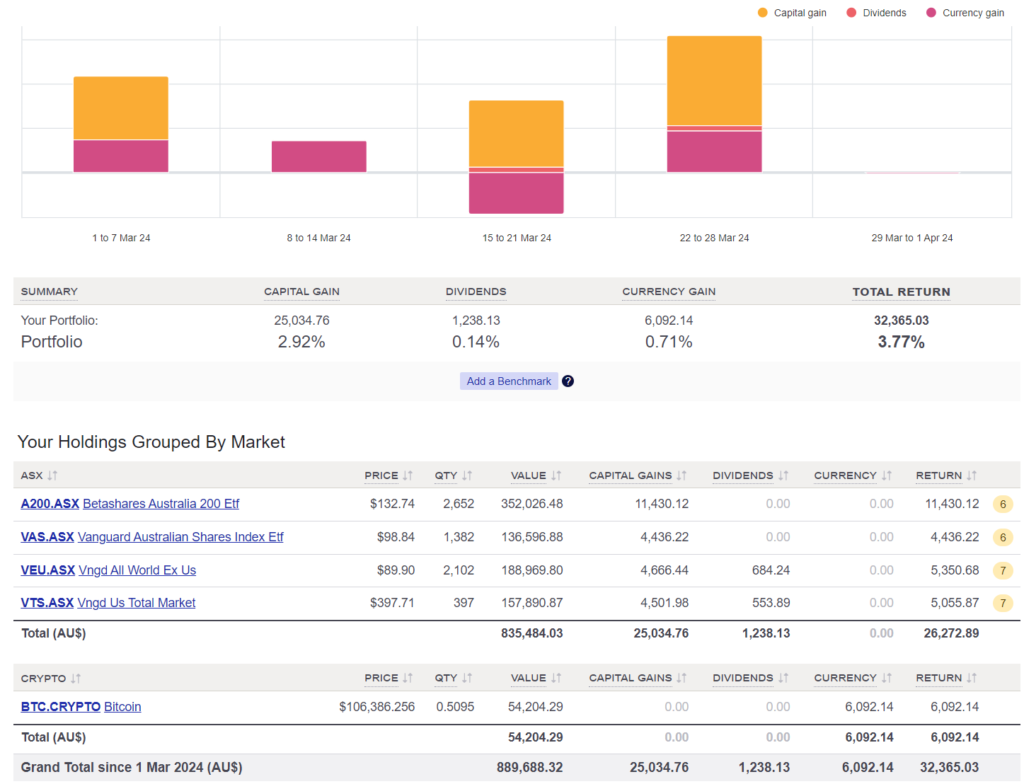

Shares

The above graph was created by Sharesight

It’s always nice to see the dividends hit the account. BTC takes a dip in June.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Jun 8, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

I turned 35 in May, which firmly places me in my mid-thirties and the start of what some might call middle adulthood (35-49).

I’ve always been a ‘man with a plan’ kinda guy, and turning 35 got me thinking back to when I was 25, wondering where the younger Matt expected to be in 10 years’ time.

I had a few milestones I wanted to achieve:

- Married ✅

- Kids ✅ (one is a start)

- Home ✅

- Millionaire by 30 ❌

- Win a seniors flag ❌

- Live overseas ✅

- Reach financial freedom ❌

- Escaped the corporate grind ✅❌ (I still do some ‘grindy’ stuff for my business)

- Maintain good health and fitness ✅

- Write a book ❌

- Buy a Tesla ❌

There was probably more, but that’s all I can think of.

The 25-year-old me would probably be quite shocked that I haven’t reached FIRE yet. We were on track to get there well and truly before 35 with no show-stoppers in the way.

I had the right job, a low-cost-of-living area, and an amazing partner who was on the same page.

What happened, dude?

Well, heaps, actually.

The main factor being how fantastic meaningful work, blended with a better work-life, could be. This combination greatly diminishes the urge to race towards financial freedom.

I would have loved to have sat down and told my younger self to head overseas sooner rather than wait another four years.

That trip was the catalyst for a lot of great stuff that’s in my life right now.

I’m still working on the rest of the list that isn’t tied to a specific age (this includes my football career 😅).

You bet I’ve been watching the latest Model Y price drops with great interest.

I think the Tesla might turn from a red cross to a green tick any month now 😎🚗

Net Worth Update

Decent month all around with the big influx of cash coming from a recent contract.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Our passive income has never been this close to covering our expenses! It won’t be long before it crosses over. At that point, I might reduce these updates, as my goal was to continue them until our passive income exceeded our expenses. I’ll write more about this as we get closer to reaching this milestone.

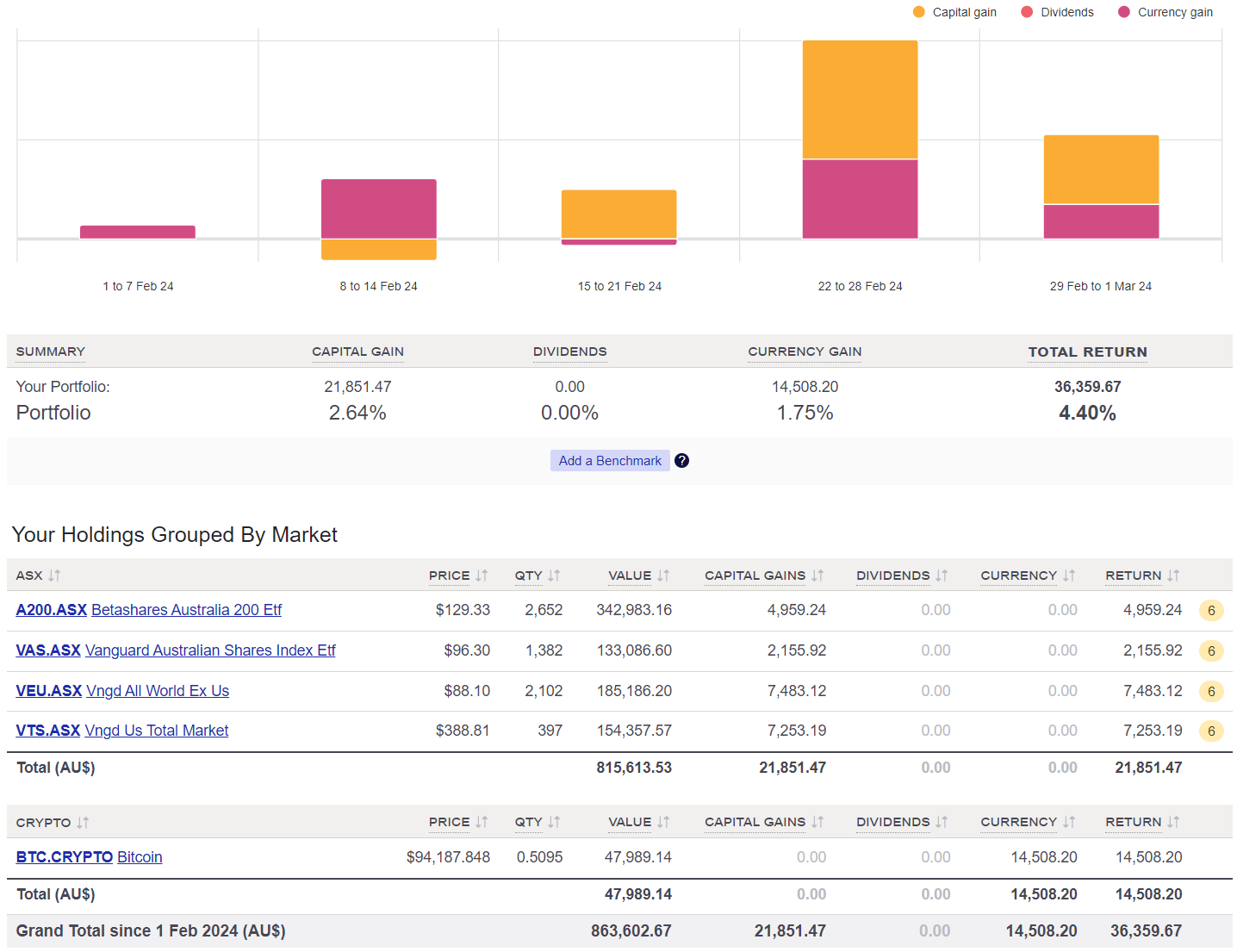

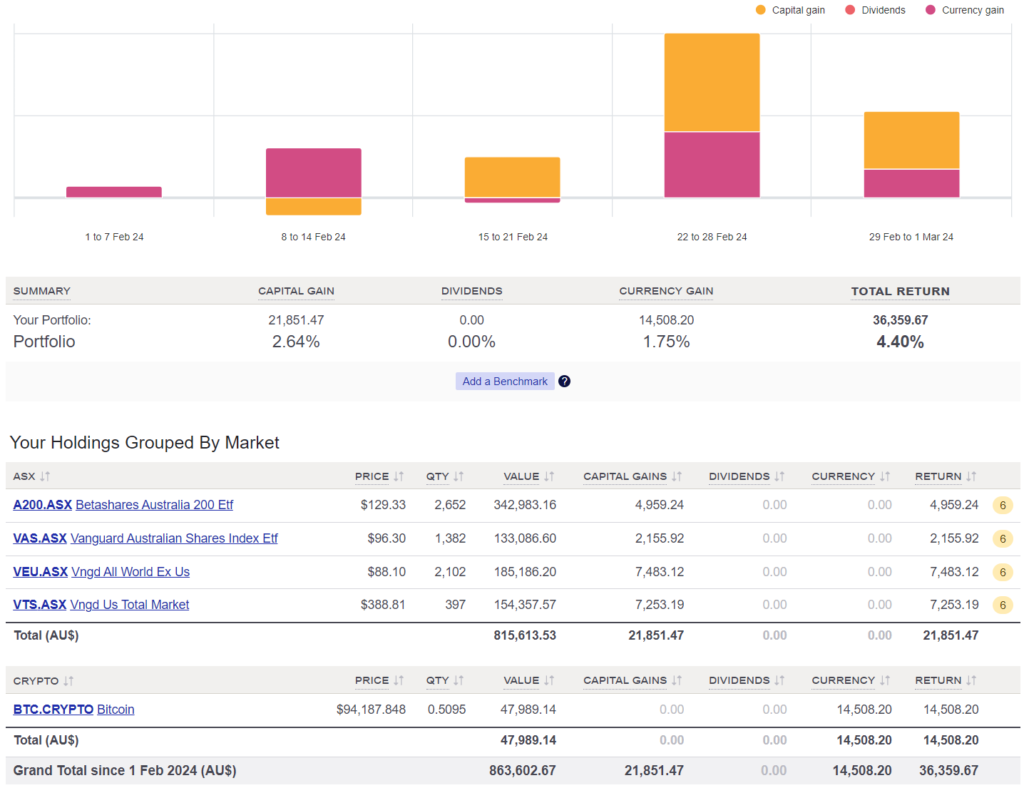

Shares

The above graph was created by Sharesight

Solid month all around.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | May 11, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

April was yet another hectic month.

Honestly, I only have myself to blame, having started a new business on top of scaling up my data-focused one.

Meanwhile, my daughter continues to grow and bring us joy. There’s nothing better than waking her up each morning to see her beaming smile. It’s been beneficial to have that clear divide between work and home, thanks largely to the co-working space.

Funny enough, home/work separation has been the number one feedback we have received when asking members what they like about the co-work.

We put a lot of emphasis on building a community, incorporating natural light, and creating a beautiful work environment. However, nearly everyone has mentioned that they just can’t get work done at home—too many distractions, chores, and kids around during school holidays make it nearly impossible.

I can also relate to that in other aspects of my life.

During Covid, maintaining a consistent workout routine at home was a struggle. At the gym, it’s a whole different story. I’m there to get shit done!

There are fewer distractions, and seeing others crush their workouts is a huge motivator.

I hope things will start to ease up so I can spend a few weekends focusing on AFB content again. It’s been a while, and there are some fantastic topics I’m eager to write about.

Net Worth Update

In April, all assets took a hit except for cash.

One significant invoice came through in my data business that really bolstered our figures this month. It almost offset the downturn, but the markets were too harsh, and we still had a significant deficit.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

It was a relatively normal month with no major expenses or out-of-the-blue hiccups.

Shares

The above graph was created by Sharesight

The Aussie dividends hitting the account is always a nice feeling!

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Apr 15, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

We officially launched the co-working space in March.

This was a big moment for the team. After dreaming about it for over 18 months, it was very cool to see our vision come to life.

Something unexpected that crept up on me was the almost full-time nature of this venture. I’ve been at the space nearly daily, ensuring everything runs smoothly and doing walkthroughs for potential customers.

For someone who hasn’t needed to leave the house for five consecutive days in almost four years, it’s been quite exhausting, to say the least 😅😮💨.

It’s been a stark reminder of how draining a full-time job can be—even when it’s just working on a computer, for heaven’s sake!

Honestly, I’m tried just thinking about how most people manage five days a week, non-stop, for over 40 years, dealing with kids and everything else 😴.

Physical activity was one of the first things to suffer when we opened up. Since then, I’ve only managed to hit the gym once a week, which isn’t a great habit to fall into.

We’re working on a solution by trying to arrange for two university students from the area to help run the space. In exchange, they’ll get free study space for the year. This should free up some of our time, and I’m hoping to get back to spending three days a week on my data business.

In other news…

I’m looking forward to dedicating more time to AFB content in the upcoming months. There are a few podcasts currently being edited and plenty of unread emails, but my family and other ventures have been my priority these past few months. I promise new content is on the way soon.

Thanks for staying patient 🙏

Net Worth Update

Another exceptional month for BTC, accompanied by strong performances from stocks and Super, resulted in a fantastic month overall.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

I had some big bills to pay for the business but our lifestyle expenses were very low in March.

Shares

The above graph was created by Sharesight

Some nice dividends were announced in March which will hit the account in April.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Mar 9, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

First off, I want to address a mistake from last month’s update.

I forgot to record the sale of 87 VTS units on 08/12/2023 in my personal spreadsheet during an extremely busy December period. Although it was recorded in Sharesight, I forgot to add that sale to my Google Doc File, which is where these updates are ultimately calculated.

I’ve updated the February figures, and all future updates will now include the VTS sale.

Special thanks to Pat and David for spotting the discrepancy and bringing it to my attention.

In other news…

I’ve been pouring my weekends into making our co-working space dream a reality, and we’re almost at the finish line for our big launch in April!

This project has been so much fun.

I’ve gone into business with one of my best mates, and we’re both building this dream to address a core problem in our lives.

We work from home and want to connect more with other creatives in our community.

The best part about this project for me was the incentives from both parties involved.

Of course, we need to cover our costs, and turning a profit would be a bonus, but what truly matters is creating an amazing communal working environment for us and other locals. At this point in our lives, this pursuit holds greater value than any financial gain.

And that’s the cool part. We are both in a fortunate position (financially speaking) to start pursuing fun and fulfilling projects that ignite the soul.

We worked all weekend last week, but it didn’t feel like work at all. I was with one of my best mates installing sound baffles, pumping Kanye on the speakers, talking smack, and dreaming of what this place could turn into!

If I think back to my previous ~10 years in the corporate world, work was never this fun. Ever!

On the other hand, I’ve hardly had any free time in the last two months (the podcast is coming back soon, I swear😅).

Between my Data business, the co-working dream and tending to my 5-month-old daughter… it’s been a tad hectic.

But at least we have secured our first member at the space 🥰.

Net Worth Update

Another big month for all our assets across the board, especially BTC.

BTC has surged to occupy more than 5% of our portfolio, a significant jump from its initial position of less than 2%. This year, it’s seen an incredible rally, and it’ll be fascinating to observe its trajectory in 2024, whether it continues to climb or perhaps takes a dip.

We don’t have any hard rules about when we would consider selling off part of our BTC split.

From the beginning, I’ve always said that I’m looking forward to actually using our BTC one day and not just hodling it indefinitely.

But I can’t lie… If BTC truly went to the moon, I would, at some point, have to reconsider our strategy and potentially sell some of it down to rebalance the portfolio. It would need to get up towards 50% of our portfolio, though, so it’s a long way off.

That’s only in an environment where I couldn’t spend BTC directly.

It’s a shame Tesla stopped accepting BTC as payment a few years ago. We would have legitimately considered paying for the new Model Y in BTC instead of fiat.

Maybe Musk will bring that feature back one day 🤞.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

We had a pretty low month expense-wise, but I spent quite a bit of the company’s money onboarding my first staffer, which was exciting!

The demand for data engineering work with government departments continues to grow, and onboarding some help was part of my overall dream of having a small local data team.

Shares

The above graph was created by Sharesight

It seemed like the whole world was on the rise in Feb.

Huge returns across the board.

We did not buy any shares in this month.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth