by Aussie Firebug | Feb 4, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

*Updated 08/02/2024: There was a miscalculation for this update that was originally published. I’ve updated the title and numbers to be accurate. The oversight was due to failing to record the sale of 87 VTS units on 08/12/2023 in my personal spreadsheet during a busy period, which has now been updated for accuracy.

I’m not one for making New Year’s resolutions, but if there’s one area where I really want to improve in 2024, it’s getting stuff done now and not later.

“Tomorrow is often the busiest day of the week.” – Spanish Proverb

This quote really hits home for me. It perfectly captures how I often catch myself thinking, “Ah, I’ll just do it tomorrow,” but then, before I know it, four weeks have flown by and it’s still not done.

I’ve made it a real priority to just do the bloody job (whatever they my be) today and don’t push it out unless it’s absolutely necessary.

I used to stroll by the weeds sprouting in my garden, always telling myself, “I’ll tackle that over the weekend.”

But this year, I’ve changed my tune. Now, the moment I spot them, I simply bend down and yank them out.

Starting off strong is key for me. I make it a point to pick out a couple of tasks in the morning, be it something on my laptop or just tidying up around the house, that I know I can knock out fast and easy.

It’s all about building that initial momentum. Once I’m on a roll, it’s easy.

This productivity hack does have its drawbacks… it’s harder to kick back and relax since it feels like there’s always something on the to-do list.

I’ve wrestled with this dichotomy my whole FIRE journey.

I want to reach financial independence so I can relax and prioritise all the other non-working aspects of my life. Yet, I can’t help but feel like I’m squandering an amazing opportunity if I’m not being productive.

One thing’s for sure… procrastination is no friend to either goal.

Another NY reoslution I’ve made that’s done wonders for my productivity (and probably hygiene) – no phone when I’m on the throne.

It’s unbelievable how much time I waste scrolling on my phone when I’m on the loo. It’s also kinda gross as well 😂.

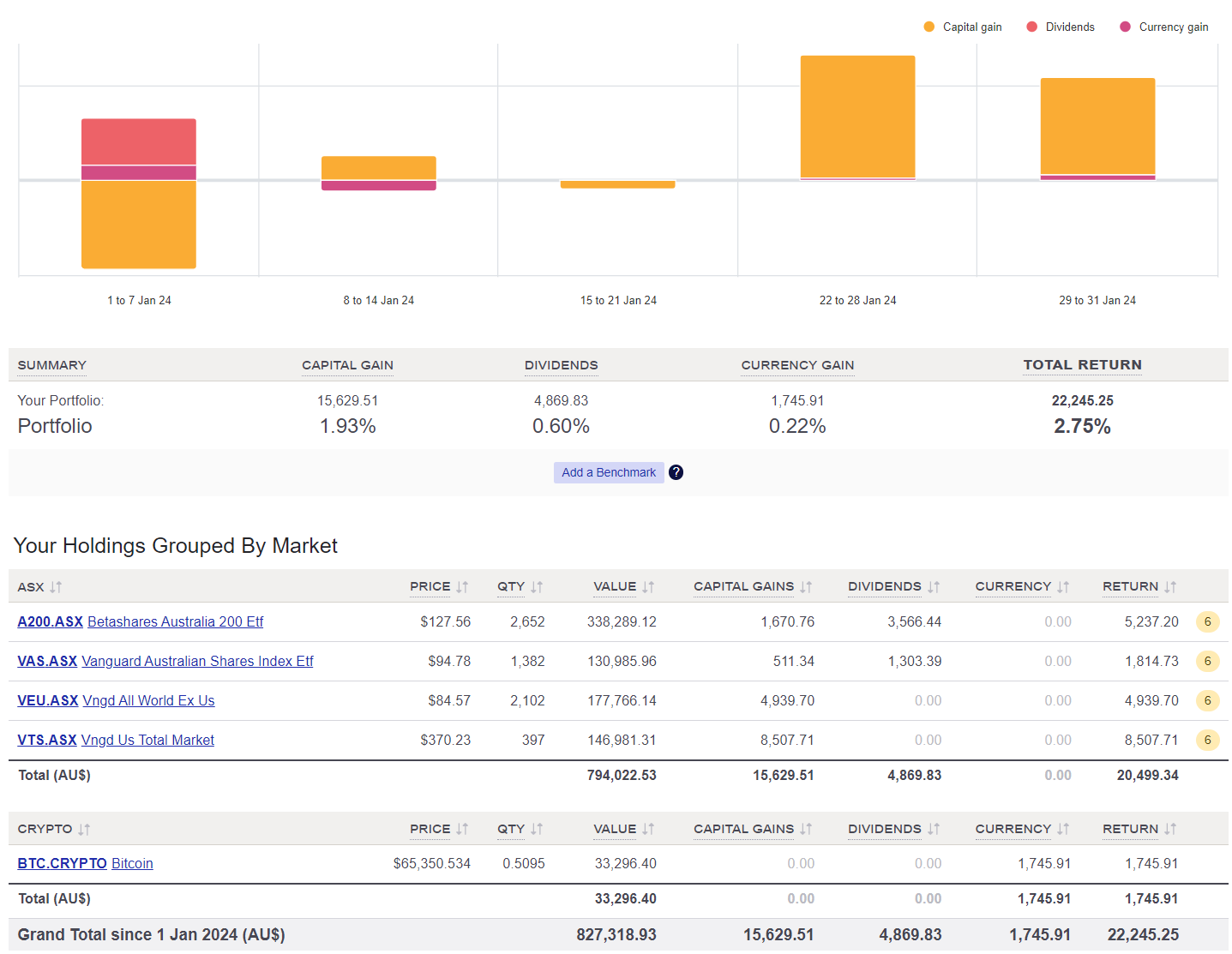

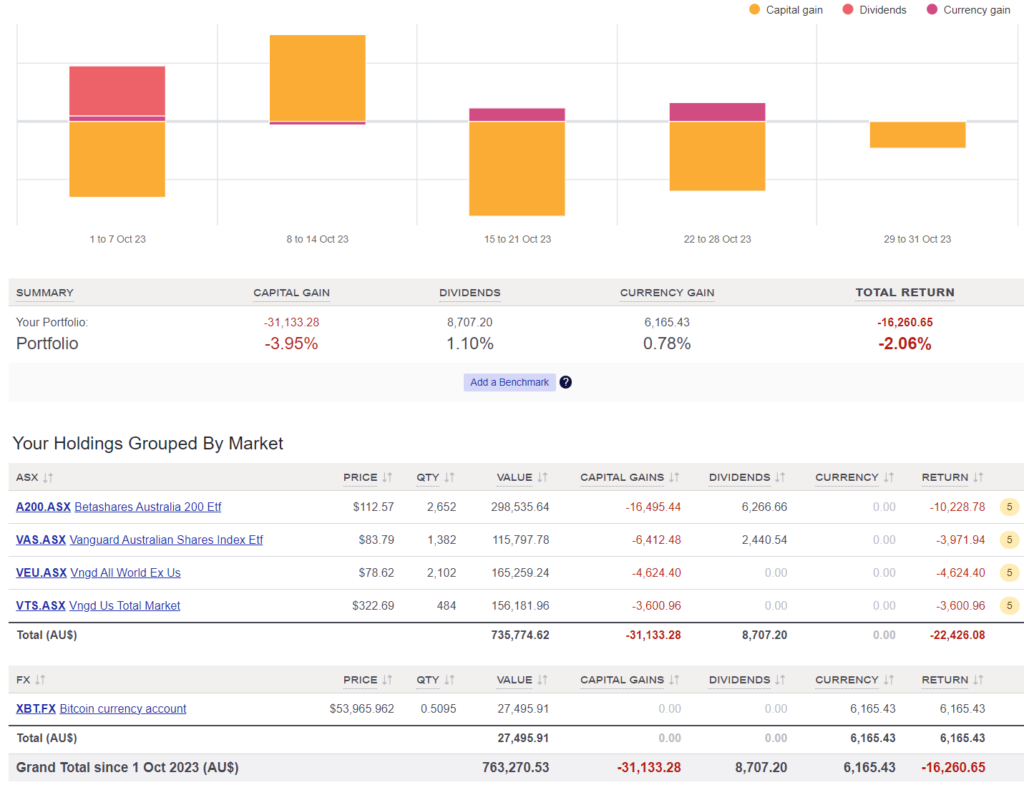

Net Worth Update

The share market had another great month In January which propelled the NW to all time highs.

We saw a pretty hefty chunk of cash go out the door, thanks to a few pricey buys we needed for setting up the co-working space. I’m not including those in our ‘expenses’ chart below since they weren’t about keeping up our standard of living. Instead, they were one-off purchases tied to getting the new business off the ground.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

.

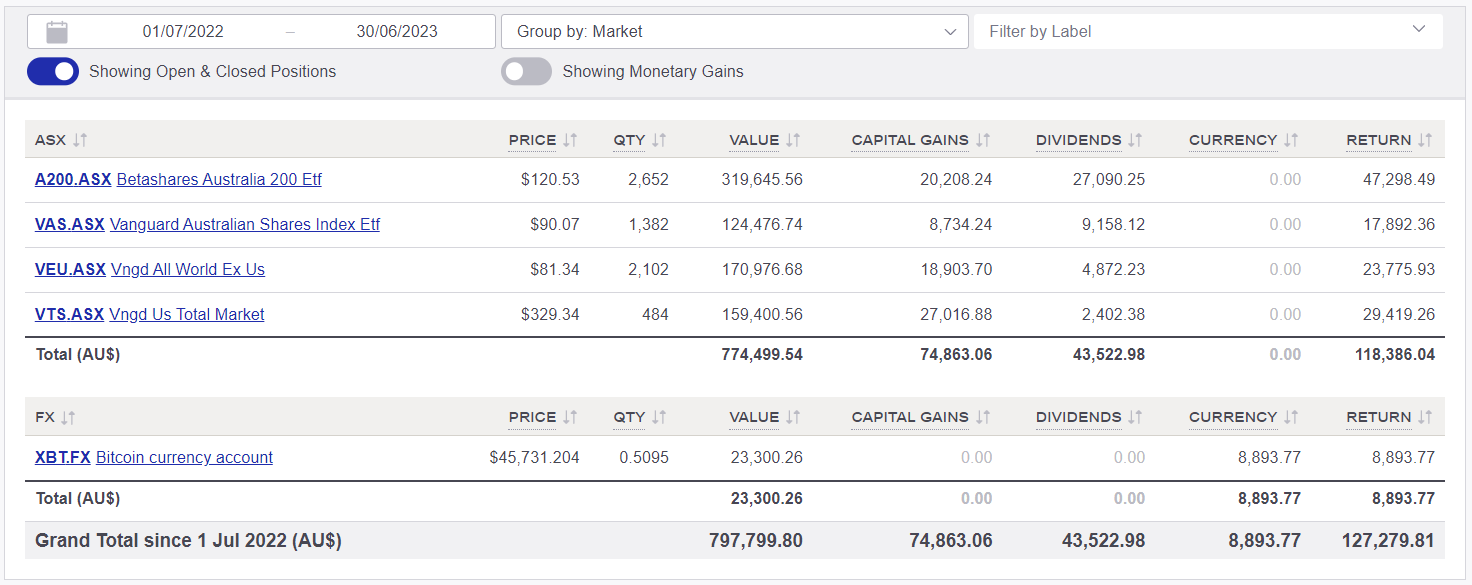

Shares

The above graph was created by Sharesight

Seeing nearly $5K in dividends come through in January was definitely a welcomed sight.

I found myself mulling over our passive income setup recently.

We’ve got five days each year that we really look forward to. There are the four days when dividends get paid out, plus that extra special day when we receive our refund from the franking credits. And honestly, the wait between those five days never feels long. Just as one batch of dividends lands in our account, it feels like the next payout is just around the corner.

I love this way to invest, especially from a psychological point of view. It’s like having a mini payday always on the horizon.

Passive investing. Simply amazing!

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Jan 7, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

As a relatively new father of three months now, I feel compelled to write about a device that has significantly improved the well-being of both my wife and me.

And I promise I’m in no way, shape, or form affiliated with the company selling this product.

The greatest invention of the 21st century

The bad boy pictured above is called a SNOO, and it’s basically a smart device for your little bambino.

This thing is crazy:

- It has 4 different levels of ‘rocking’, which helps soothe your baby to sleep.

- It has a microphone to detect if your baby is crying (which can then increase the levels up or down depending on what pre-made settings you have assigned in the app).

- It has a speaker for white noise and a ‘hushing’ sound if your baby starts to get upset.

- The app tracks your baby’s sleeping patterns, which apparently is useful if you want to sleep train (we haven’t got this far yet)

But most importantly, it helps you and your partner get better sleep for the first 6 months, which is invaluable.

We got our SNOO second-hand for $800, which might sound like a lot of money (and it is), but good God, that sum seems laughably low compared to the value it has brought us.

Picture this:

It’s 4:30 AM, and you have been jolted awake by your baby’s cries.

You’re smack bang in the middle of some REM goodness and so tired you could nearly throw up. You’re just about to flick the covers off and rock your baby back to sleep when you hear the SNOO’s responsive rocking motion kick it up a notch and start soothing your baby.

You give it a minute or two, and, to your absolute astonishment, your baby goes back to sleep, and you get another glorious sleep cycle.

🙌

Words can’t explain how glad I am that we set ourselves up before having kids. Now, spending nearly $1,000 on a device like this doesn’t cost me a wink of sleep. I would have never done that in my 20’s and it gives me anxiety to think I would have forgone such a great innovation for the sake of getting ahead financially.

The SNOO has been a godsend for us so far, but I’ve also read that it bites you in the ass when you have to take it away… but I’ll take 6 months of sleep and then deal with the consequences any day of the week.

Good luck, future Firebug 😅

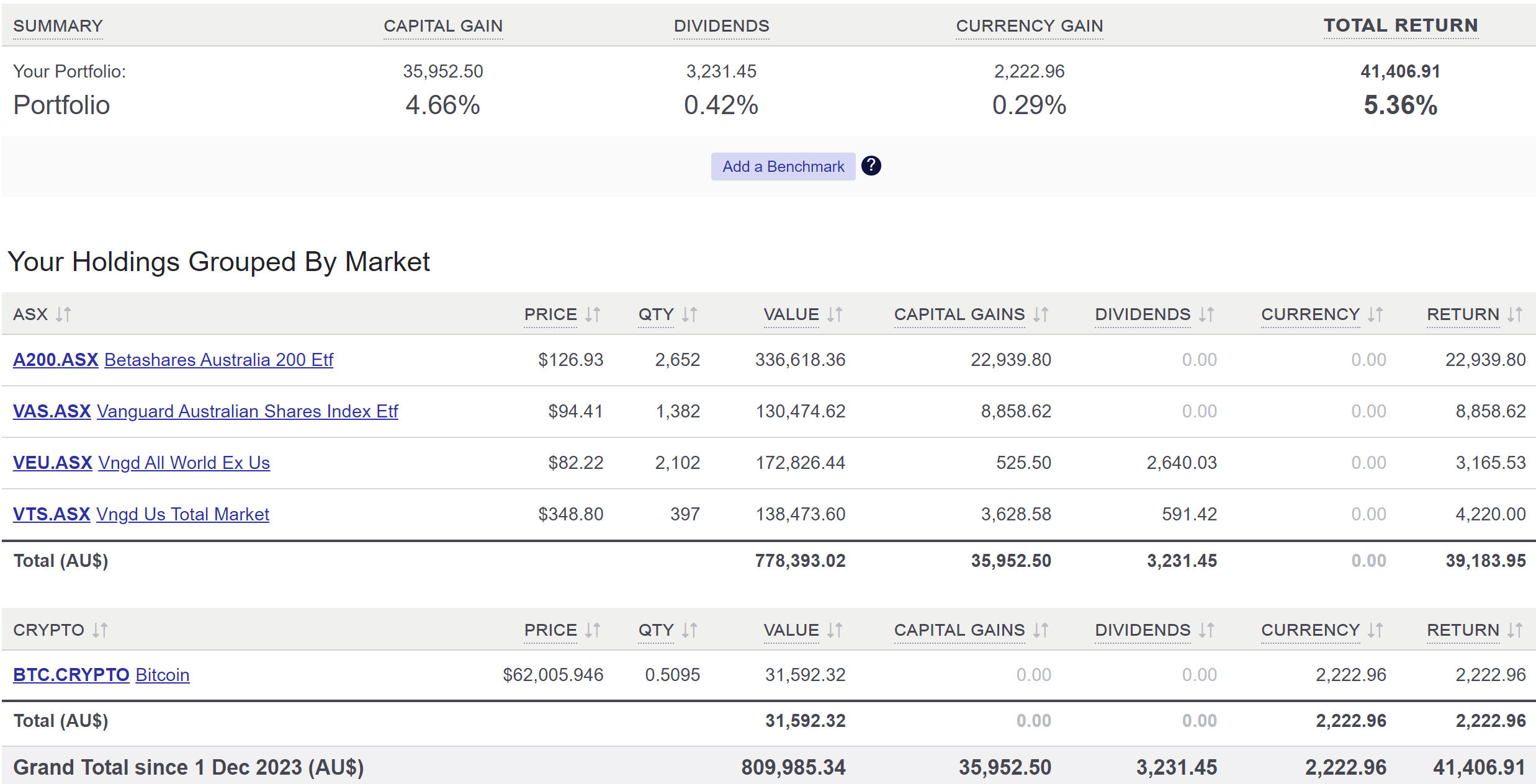

Net Worth Update

Santa came early for us share market investor in December.

A huge month for all asset classes to boost our NW to a record high of $1,283,257.

| Years End |

Net Worth |

| 2021 |

$1,038,417 |

| 2022 |

$1,171,120 |

| 2023 |

$1,283,257 |

We started 2023 at $1,149,655, which means we increased our net worth by $133,602 during the year.

But here’s the astonishing thing… we didn’t make any investments throughout the year, and we spent all of our dividends!

Yeah yeah yeah, I know 2023 was an exceptional year, but still.

The power of compounding is crazy!

We spent all our investment income, took two trips abroad, had a baby, didn’t work for six months, made no new investments, and yet our net worth still grew by over $130K — absolutely mind-blowing! 🤯

For anyone reading this who might be just beginning their journey, I have one message for you:

Keep going.

The snowball is so bloody hard to get going. But once it’s rolling, it gets easier and easier. And you get to a point where it feels like you’re playing this money game on easy mode.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

A pretty normal month spending-wise.

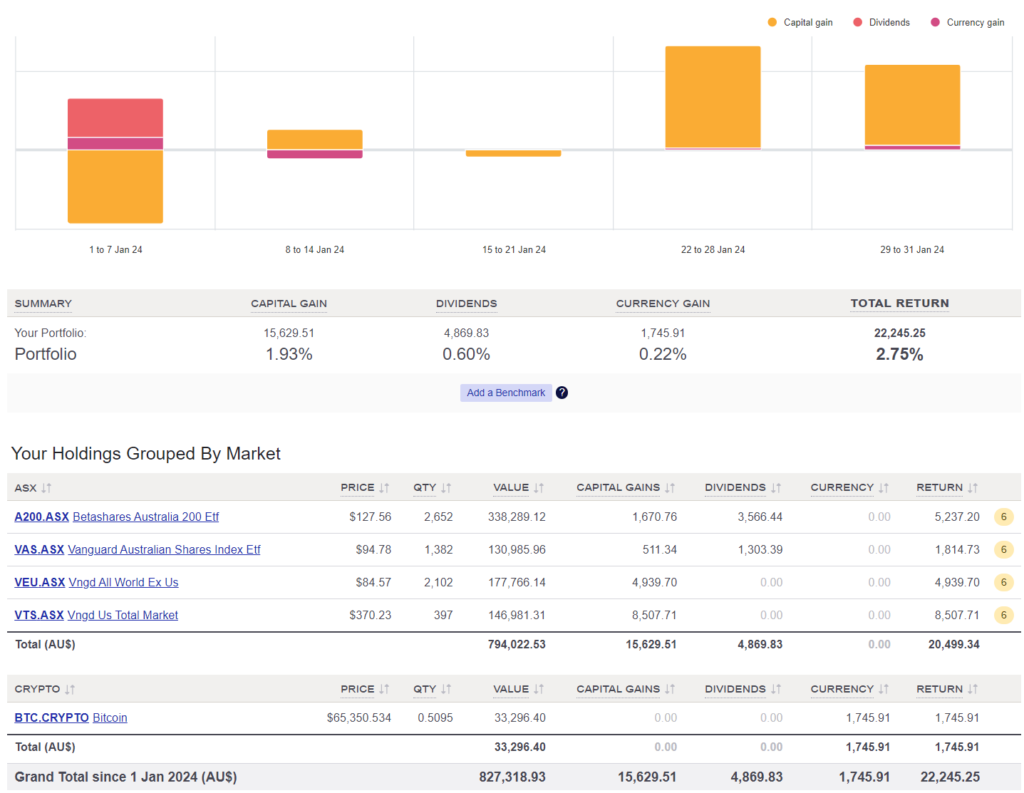

Shares

The above graph was created by Sharesight

For the first time ever, we sold a significant amount of shares in December.

We sold $30K worth of VTS to help seed our co-working dream.

We opted for VTS as it had become the most out-weighted holding compared to VEU.

I didn’t want to sell any of our Australian shares (A200 and VAS) because they will naturally decrease in weight over time as they typically distribute larger dividends.

Mentally, I struggled with the decision to sell such a significant number of shares, but I had to keep reminding myself what was actually important.

Do I care more about missing out on market gains, or is it more important to me to chase a dream?

Given that my family and I are in a comfortable financial position, I believe the above question is rhetorical.

The $30K is going to be used to help set up our space with furniture, management software and security management.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Dec 21, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

We secured the lease for our co-working dream in November 🥳.

Our new Co-working space

This was the first step towards our goal of creating a community-focused shared environment for small business owners and entrepreneurs.

There are so many unknowns when you start a venture like this one.

- What’s the demand?

- How much do you charge?

- What are the ongoing costs?

- What type of permits do you need?

I thought adjusting to life without the stability and assurance of a full-time job was challenging enough. However, pouring money into such an unknown project tops it.

But here’s the rub: it’s so bloody exciting!

There’s a profound sense of fulfilment that comes from being in charge of your own destiny.

I’ve also noticed something very interesting when discussing this idea with friends and family. People love to point out all the things that can go wrong and rarely see the potential upside.

And it’s not like they are doing it deliberatively to be nasty. There seems to be an inherent truth about humans: our operating system is wired more to avoid losses than to actively seek gains.

Many people are comfortable remaining in their 9-5 jobs, contributing to their boss’s dreams, rather than taking the leap to pursue and build their own.

That’s not to say there’s anything wrong with the old 9-5. But I do wonder how many kick-ass products/services have remained unrealised because those capable of starting them were too risk-averse to take the plunge.

FIRE has given us the financial courage to give this a go without worrying about my family suffering if it fails.

And even if we do fail, the satisfaction of having a crack will remain. In the end, it’s the effort and the journey that counts.

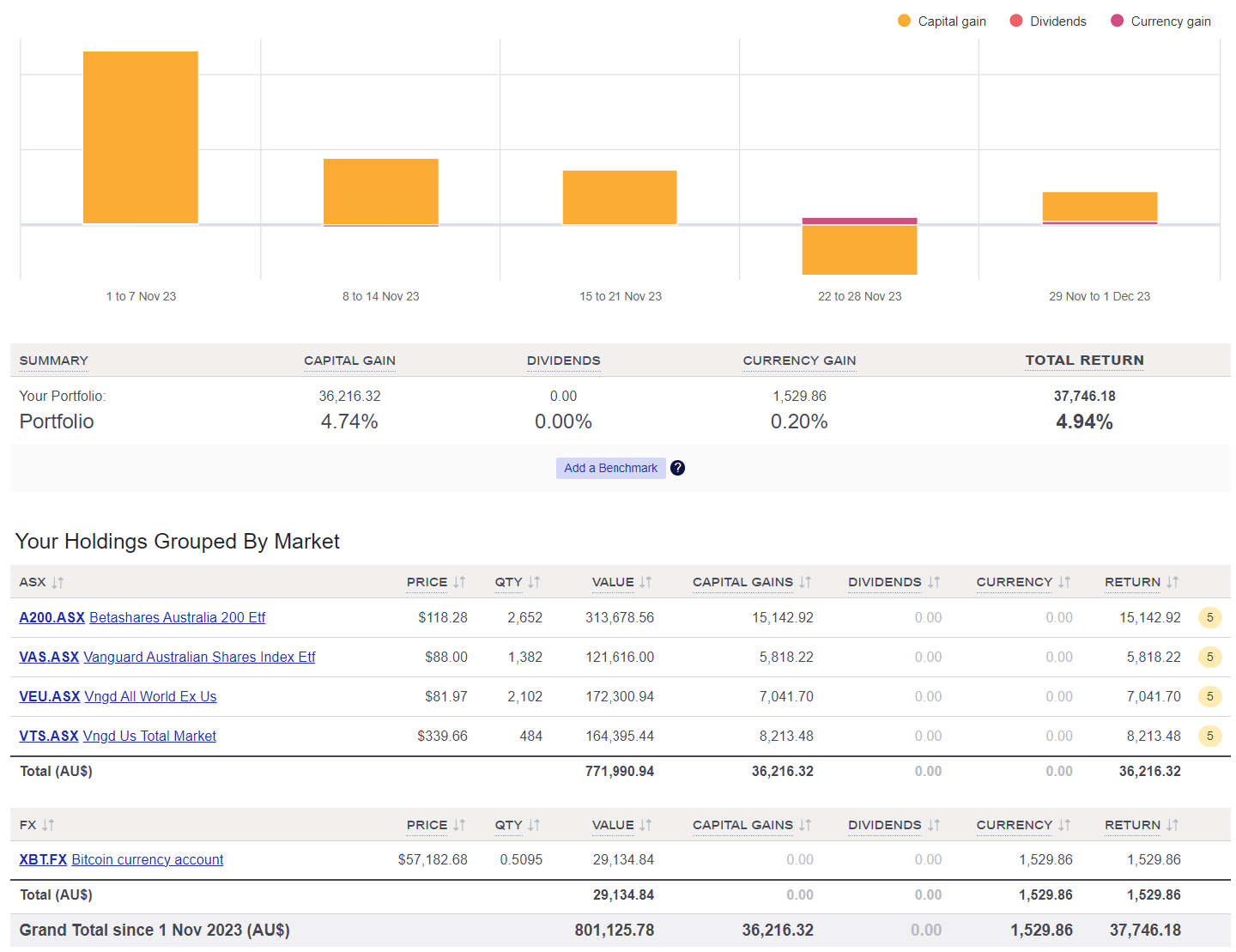

Net Worth Update

Wowee!

What a huge month for our portfolio, Super and BTC.

This is coming off a three-month slide that saw our net worth decrease by over $76k!

That encapsulates the essence of the volatility game in the stock market. It’s the reason we earn the returns we do as investors. Not everyone can withstand these fluctuations, and those who can are rewarded accordingly.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Booking another Bali holiday for next year saw a spike in our spending in November.

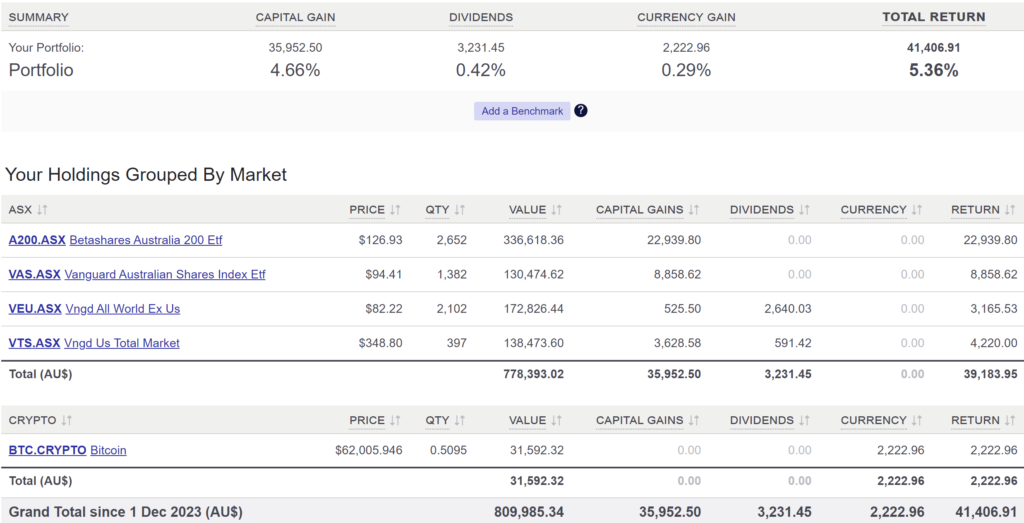

Shares

The above graph was created by Sharesight

It seemed like the entire world was on an absolute tear in November.

VTS has a whopping 5.26% gain in a single month followed by our Aussie shares (~5.05%) and then VEU (4.26%).

BTC continues to climb up and up increasing in value by 6.04%.

We made no purchases in November.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Nov 19, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

My second month of dad life has been going great.

Yes, there are times when getting enough sleep can be difficult. But boy oh boy it’s all worth it when you see your little one’s adorable smile 🙂

I’m not kidding; it’s like black magic. I’m pretty sure evolution has developed this way to give parents an additional gear they can tap into when things get hard haha.

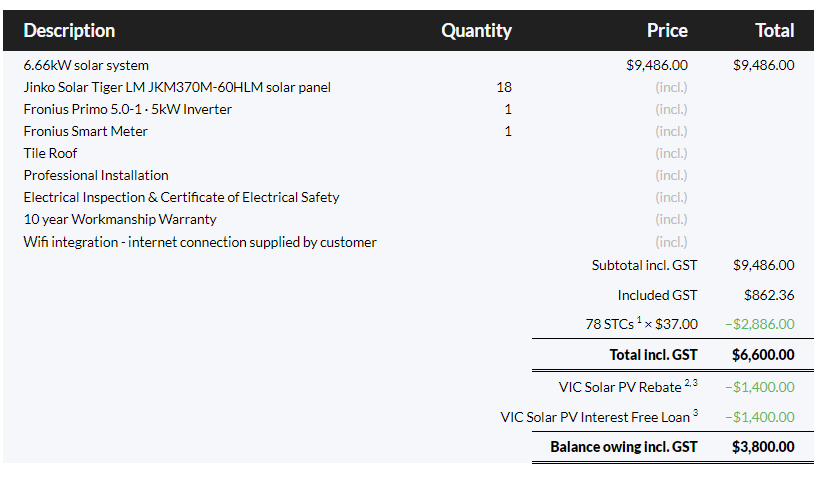

As a data nerd, I’ve been looking forward to seeing how much more electricity we would use when the baby arrives. This was one of my biggest motivators for installing our 6.66 kW solar system in October 2021.

Our out-of-pocket cost for that system was $3,800.

Solar Install

Our usage comparing October last year to October this year has been the following:

| Month |

Grid usage |

Consumed directly from solar |

Total Usage |

Self-sufficiency |

$ Saved (based on 39c/kWh) |

| 22-Oct |

115 kWh |

102 kWh |

217 kWh |

47% |

$40 |

| 23-Oct |

153 kWh |

151 kWh |

304 kWh |

50% |

$59 |

Since the three of us are home most days, our energy usage has increased by over 40%. And I suspect this will only increase as our baby grows up.

The other significant factor is we will be buying an electric car next year (trying to hold out until the new model Y drops). Our solar panel energy consumption will skyrocket from that point onwards and the payback period will significantly speed up.

It’s going to be cool to calculate how much our panels save us in a few years and compare that to how much we would have received if we invested it instead.

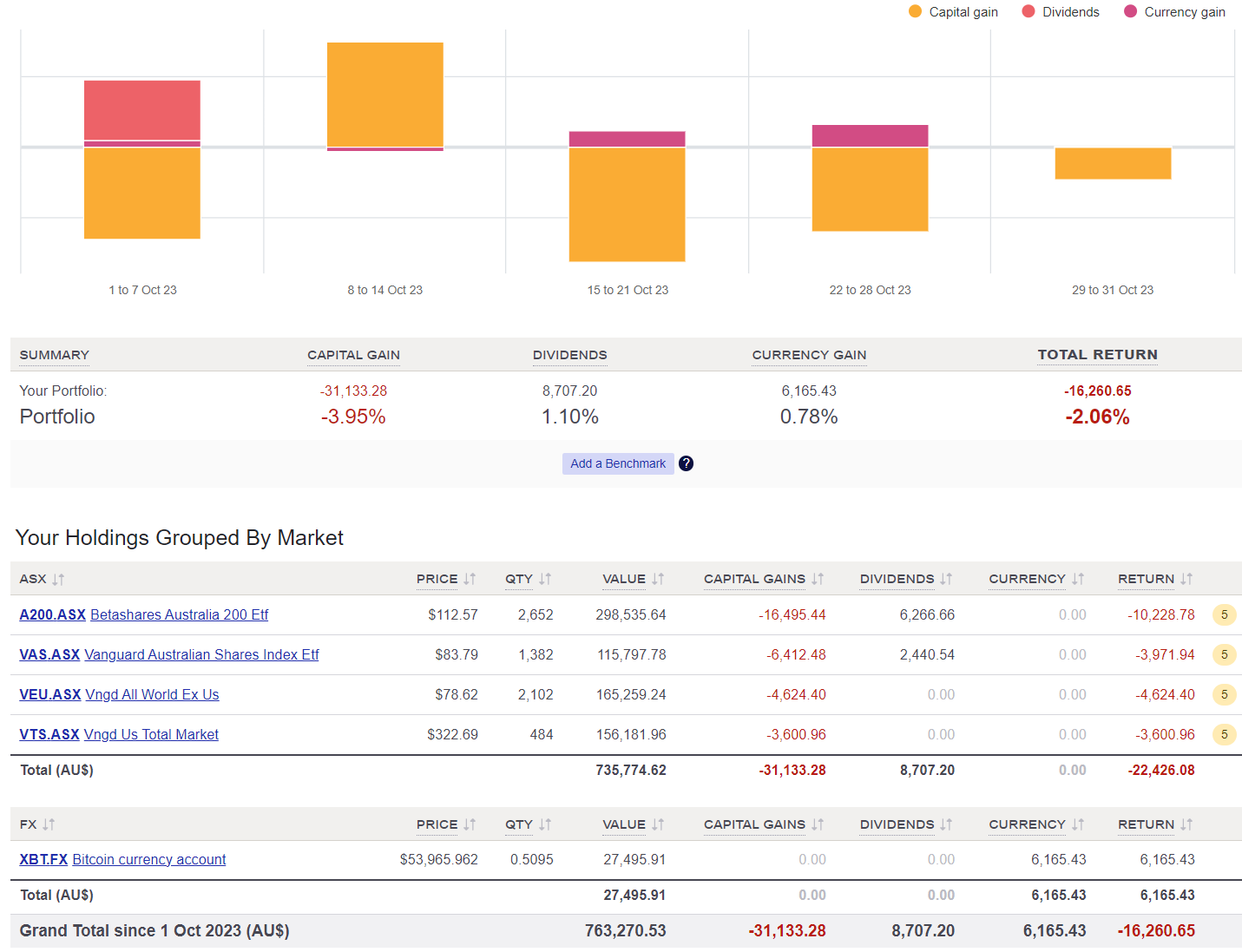

Net Worth Update

Another brutal month with our shares and Super being hit the hardest.

On a positive note, Bitcoin increased by 30% in October!

I haven’t used my Bitcoin yet, but I’m interested in finding out where I can spend it. Does anyone know of any cafes or stores in Melbourne that accept BTC or are on the lightning network? I’m curious to see how easy the process will be.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Another quiet month on the expense front. We’re really not spending a lot of money at the moment.

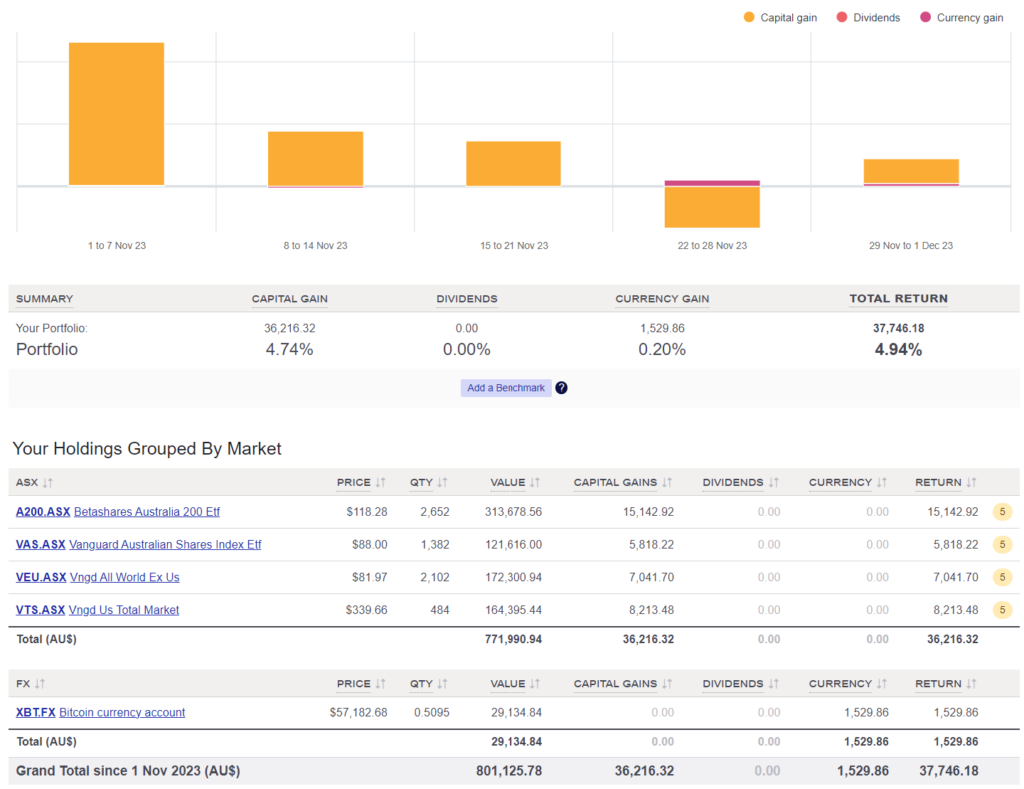

Shares

Monthly Performance

The above graph was created by Sharesight

$8.7K in dividends slightly softens this bad month from a psychological point of view, but still, not great.

We made no purchases in October. We are still keeping our cash position high until I secure some contracts that will be landing in the coming months.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Oct 23, 2023 | Retire Early

I’ve been thinking about this post for the past 18 months, and to be honest, it’s long overdue.

So much has changed over the last 11 years since I first stumbled across FIRE.

And if the article’s feature image wasn’t obvious enough, I recently became a father. So, now is the perfect time for a big update/recap on life at the Firebug household.

Are We Still Chasing FIRE?

A few people have noticed we haven’t invested in shares since October 2022 (over a year ago!). Some community members have been commenting on my net worth articles and emailing me directly, asking if we’re still actively pursuing FIRE.

The short answer is yes.

The long answer is more interesting.

For the first time since we started our FIRE journey, we have switched from accumulation to consumption. We’ve been dipping into our portfolio (spending some of our dividends) every now and then for the last two years.

And believe me when I say this was not a simple task to accomplish. When you’ve dedicated over a decade to pursuing a goal and have structured your life around constant optimisation and channelling every available dollar into investments, it goes against your instincts to spend rather than save.

Old habits die hard.

Imagine asking a seasoned marathon runner who has spent years training for endurance races to suddenly become a professional weightlifter.

But what’s the point of investing if you never switch from accumulation to consumption?

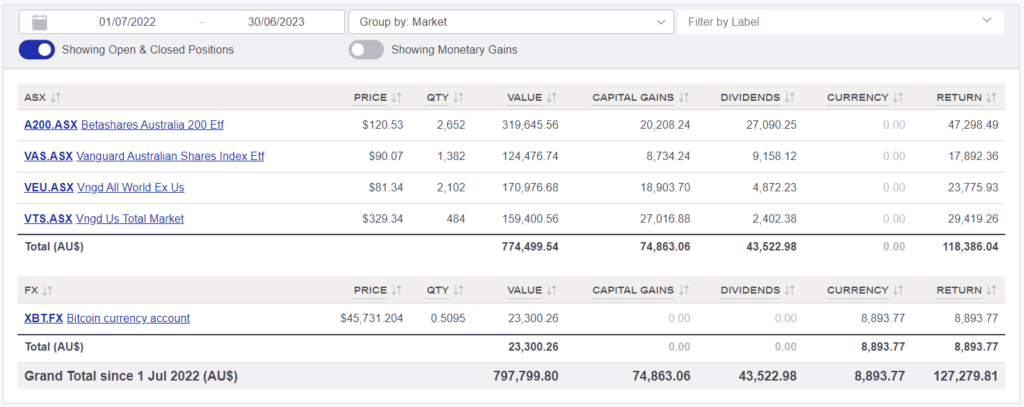

We earned ~$43K in dividends last financial year.

Last F/Y performance

Even though the markets had an above-average return last year, $43K is not enough for us to live off completely. However, it’s a fair chunk of change that allows us to buy back our time now rather than waiting to hit some arbitrary number in a spreadsheet.

During our FIRE journey, our priorities changed, and the race to financial freedom no longer seems so important (more on this below).

Side note: This is a major consideration point that many Excel spreadsheets neglect to model for. Super is a fantastic vehicle to save for financial freedom. However, if your priorities change halfway through your journey, that money is locked away until your preservation age. Looking back, I’m really pleased that we decided paying extra in taxes was worth the added flexibility.

Heavily inspired by the book ‘Die with Zero’ by Bill Perkins, we knew that in our late twenties, we had a brief window of health, financial stability, and free time to explore parts of the world we had always wanted to visit.

And that’s exactly what we did.

We have travelled to over 30 countries and visited every continent on earth (except for Antarctica).

I’ve found that many people in the FIRE community tend to be a bit cynical about the whole ‘Travel the world while you’re young’ cliché.

“Sure, it’s cool and all. But you know what’s really cool? Never having to work ever again!”

I held a similar belief for quite a while and often wondered whether those who splurged on travel were trying to convince themselves it was all worth it because they spent a fortune.

But living overseas and visiting so many different cultures changed my point of view.

I’m not saying it will be as transformational for everyone as it was for me, but travelling dramatically broadened my horizons, particularly regarding my relationship with meaningful work.

Spending god knows how much we spent during those two years abroad was, in some ways, more of an investment than saving our money and buying shares.

There’s a good quote that sums it up for me.

“Travel is the only thing you can buy that makes you richer.” – Anonymous

Retire From The Rat Race, Not From Work

When I reflect on my journey towards FIRE, it’s crystal clear that my desire to escape the rat race was largely motivated by a job that left me unfulfilled. I wanted to create a passive stream of income so I could pursue other interests without worrying about paying the bills. Financial freedom was my ticket out of the monotonous 9-5 grind and onto eternal Happyland.

I think many people are attracted to the idea of FIRE because they either hate their job or are left unfulfilled after spending most of their time there (that was me).

My professional work life has had two distinct phases. Pre-London and post-London.

I worked for various levels of government in regional Victoria for eight years before my wife, and I jetted off to the other side of the world for a two-year adventure.

Pre-London, Matt enjoyed the people he worked with and found parts of his job fun and interesting. But it was extremely rare for him to get ‘excited’ about work. Work at that stage was 95% about making money so he could live his life outside of it. Public sector culture tends to be sluggish, bureaucratic, lacking energy, and occasionally downright wasteful.

I never had a problem with any of that because as long as I was cashing my paycheck, it’s all good.

However, an unstimulating work environment can gradually destroy your creative spirit.

Subconsciously, I was checking out. Towards the end of my first job, I just didn’t care what was going on. I had no passion for the work I was doing. No pride or excitement. Just rocking up to collect money, talk with some of my mates and bounce.

If you put up with this long enough, you may lose sight of, or simply stop searching for, the enjoyable aspect that meaningful work can provide which is a terrible outcome.

Or as Dr Robert Doback so eloquently says at the end of Step Brothers, “Don’t lose your dinosaur”.

Fast forward eight years, and I started my first consultant gig in one of the busiest cities in the world.

London is like a vibrant melting pot filled with diverse ideas, talented people, and innovations. It’s filled with folks who are passionate about changing the world. I was working alongside some seriously talented people with incredible energy and an ambitious spirit that rubbed off on everyone they worked with.

It took me until I was 29 years old before I got my first taste of kick-ass, motivational, and inspiring work culture with world-class leaders.

I had a really interesting conversation with Carl Jensen (AKA Mr. 1500) in July, and we spoke about sliding door moments and how fulfilling, purposeful work has the power to inspire you to leap out of bed each morning.

He asked me a thought-provoking question that went along these lines.

“Would Aussie Firebug be a thing if you moved overseas straight after uni and were genuinely inspired by your job?”

I’ve been thinking about that for a while now, and the honest answer would be no.

Why would I need to reach financial freedom and escape the rat race if I was in a job I really liked? If I had been truly satisfied with my job, I wouldn’t have been driven to explore other paths.

That being said, even if someone enjoys their job, there are still legitimate reasons to aim for financial freedom. However, in some cases, the burning desire to make necessary lifestyle changes may not be there, and it’s really hard to change your lifestyle if you don’t have a strong ‘Why of FI’.

So What Now?

In some strange way, I feel like I’ve skipped the ‘Financial Independence’ part and gone right ahead to the ‘Retire Early’ portion. My version of RE has always been ‘Retire Early’ from the rat race. It’s never been about not working.

And financial freedom isn’t binary, either. There are levels.

From an Excel spreadsheet point of view, we have not reached financial freedom. But from a real-life point of view, I’m as free as a bird. I know that our portfolio will continue to compound over the years and eventually hit our FIRE number.

But that part is kind of irrelevant to us now. I already feel like we have conquered our first mountain (FI), and now it’s time to shift our attention to the next phase of our lives (RE).

Another sidebar: Some people never get off their first mountain. They make all sorts of excuses to keep working another year and saving and investing and saving and investing. They drop their safe withdrawal rates from 4% to 3.5% and then 3% just to make sure. A lot of people in the FIRE community have drifted away from the movement’s initial objectives and principles. Live a happier and more satisfied life by buying back your freedom through intentional lifestyle choices and common sense investing. But if you never dare to take that initial leap from that first mountain, you’ll remain stuck in the daily grind, even if you accumulate immense wealth.

I’m not kidding when I say that I feel thankful for how my life has turned out almost every single day.

The life I’m living right now was something Matt could only dream of in 2015 (when I first started blogging). And I’m not just talking about all the travel either. I’m mainly talking about having complete control over my time during the week. Some days are spent travelling back and forth to Bunnings doing home renovations with my dad. Some days, I’ll walk with my sister and little nephew for a few hours. Some days, I’ll catch up with Mum, and she’ll tell me all about her and Dad’s next trip over a cuppa.

Some weeks, I’ll spend 40 hours working on my business if I’m in the zone. Some weeks are dedicated to getting AFB content out there.

Having absolute control over your time is a blessing, yet it can also present challenges.

It’s kinda like going to a restaurant offering over 100 different meals. It’s overwhelming at first. You feel the need to look at every option in case you get meal envy after you order. Sometimes it’s really nice when they only offer 3-5 dishes.

Having a job to go to gives people structure. And I’ve rarely appreciated that structure until I stepped out of the 9-5.

It took me about two years to actually figure out what I wanted to do work-wise. I don’t care who you are, everyone has a vice. We all need to engage in some form of meaningful work, even if it doesn’t necessarily result in earning money.

In this net worth update, I wrote about my aspirations of bringing some of that vibrant work culture from the UK back to my hometown in Victoria and my dream of a co-working space.

Helping foster a local community of like-minded people is really important to me. It’s part of what I’ve been missing since returning home from London. I haven’t found my ‘work people’ yet, but I know they’re out there. I just need to bring them together 🙂

Feel free to follow our Co-Working Facebook page to follow along.

I guess the main point is that I march to the beat of my own drum these days.

I’ll always be a finance nerd, but I have completely lost the obsession I once had with investing, budgeting and tax minimisation strategies. I’ve even put a pause on consuming FIRE-related content, except for those I’ve been following for a while and have a deeper connection with as individuals, rather than simply using it as motivation for my own journey.

I’ll continue posting our net worth updates until our passive income exceeds our expenses (based on the 4% rule). Once that happens, I don’t see a need to continue to publish those articles.

As far as our strategy is concerned. We are still aiming to build our passive income mainly through shares, cash and a little bit of Bitcoin for some speculative fun.

Our core mix of A200, VAS and VTS remains the same. Our current target weightings for each market are 20% US, 20% world and 60% Australia.

I know plenty of people will say that’s weighted too much towards Australia. However, I want to stress the significant psychological power of using dividends to cover your expenses rather than selling shares.

We still haven’t cracked open VTS or VEU even though that was the original strategy. And I’ve come across countless members of the FIRE community who have suffered the same fate. Many find it much simpler to use dividends that land in their bank account, as opposed to selling down their portfolio.

We must be pragmatic about these sorts of things. Efficiency is important, but there are times when it’s wiser to choose the strategy you’re most likely to execute.

I’m a Dad Now!

The biggest change of all has been a recent one.

Mrs FB and I welcomed the newest member of the family in September, marking a moment that forever changed our lives.

I won’t get into all the details of how our little bundle of joy has transformed our world because it’s an emotion that only other parents can understand.

But what I will say is that from a FIRE point of view, having a child hammers home how important controlling your time really is.

And to be fair, this is something I’ve been speaking about since I started this blog. I knew all the way back in 2011, when I first started working, that having a kid really chews up your time. One of my biggest motivators for reaching FIRE was to be able to do everything I loved doing while also being a committed father.

I just couldn’t see how that was possible working 40 hours a week since I had so many extracurricular activities I enjoyed.

I had seen this story play out a bunch of times before. People have kids, and suddenly, they can’t find the time to look after themselves, or they start forgoing activities that make them happy.

They might be unable to focus on their health and fitness as much and become unwell. They begin to see friends and family less frequently than they used to. They start skipping social outings because they’re exhausted from the week etc. etc.

From what I witnessed growing up, it appeared that new parents often set aside their passions and self-care to invest more time and energy in raising their children. A noble goal, but I selfishly wanted to put myself into a position where I could do everything that made me happy and be a kick-ass dad.

FIRE was going to give me my time back when I needed it the most.

And it’s pretty much worked out that way now.

Friends and family have been asking me when my paternity leave finishes, and I’m like:

“I work for myself. I can have as long off as I want”.

I feel incredibly fortunate to have the best of both worlds. I’ve kicked off some projects that fulfil my desire for meaningful work, yet I also have the freedom to relax and spend entire days with my lovely daughter if I feel like it.

This is what FIRE is all about IMO.

Conclusion

Our FIRE goal from the very start was always to ‘Retire Early’ from the rat race. It was never about not working altogether or amassing the biggest fortune.

From my experience, once we had around 50-70% of our expenses covered in passive income, that was enough to give me the confidence to quit the stable 9-5 and have a crack a something else without worrying about the money.

For me, that’s starting a co-working space in my hometown, helping build a community of like-minded people, and addressing my love of all things data through a business idea I’ve been cooking up.

When you have autonomy over your time and start to work on projects that ignite your passion, you look forward to working almost every day.

There is also a really important concept that I hope you’ll consider too. Similar to the unwritten rule of not starting another book before finishing the current one, it might feel like you’re cheating if to jump ahead in the journey and begin enjoying the benefits of RE before reaching FI. However, not only is it perfectly okay to do so, but I also believe it’s the better path.

I consider myself extremely fortunate that my partner and I found ourselves in a situation where I had to resign from my job to fulfil a bucket list item (living abroad). That incident became the catalyst for stepping one foot off the FI mountain and starting to climb the RE one.

But I’d like to be crystal clear, Mrs. FB and I are still on the journey towards FIRE, but we’ve decided to start enjoying the fruits of our labour sooner rather than later.

We’re now drawing down part of our portfolio after devoting so much time and effort in our 20s to building it.

Life’s short, and I want to be as present as possible to watch our beautiful daughter grow up.

That’s what it’s all about. Buying back your time to enjoy special moments (like leisurely sleep-ins) with the people you love.

As always,

Spark that 🔥