by Aussie Firebug | Nov 11, 2015 | Investing, Mindset

Over the past couple of years I have discovered a growing trend that a number of people seem to be doing. It goes something like this, “We only want to invest AFTER we have finished paying off our house.” Fair enough. I can see that some people want the security that comes with owning your own home outright without a loan.

What I don’t understand is what some people do next. “OMG Brad isn’t it so fantastic that we have saved every penny for the last 10 years so we can now say we own our $500K house outright without a loan?” “Certainly is Jenny, such a relief that we don’t have a loan, I think it’s time we looked into investing outside our Super to build a nest egg to retire on.”

They start to talk to friends about investing and of course because they live in Australia the topic of investing quickly turns to real estate and how everyone knows someone who bought a house that doubled in 7 years blah blah blah.

Intrigued, they do a bit of research and ask family or friends how they can get started. They eventually book an appointment in with a broker to assess their borrowing capacity and what’s involved with getting a loan for an investment property. The broker educates them that they would have to save X amount of money to put down as a deposit OR they could use equity in their home and could get a loan straight away. “Wow, you mean we wouldn’t have to wait and save a deposit?”

“Yes, that’s right, just pull out some equity in your house and use it as collateral for your investment property.” Brad and Jen are amazed that they don’t need to save anything and can get started right away. The spur of the moment excitement causes them to go through with the process and they are now the proud owners of an investment property after pulling out $80K of equity from their home. A few years pass and they get the property revalued. To their amazement, their investment property has risen in value by over $70K. They are so excited that they could make so much money just by owning the house that they want to have another. They have plenty of equity their broker explains so this shouldn’t be an issue. After 3 or 4 properties they start to run out of equity as they approached 80% LVR for their own home.

[pullquote align=”full” cite=”” link=”” color=”#ffa500″ class=”” size=””]My problem is that if you are intending to use the equity in your house you might as well not pay it off to begin with[/pullquote]

When I hear people utilise this strategy I cringe. I mean what’s the point of paying off your own home just to withdraw the equity to invest with? You’re just wasting time doing this. As I’ve mentioned in a previous post, the earlier you start investing, the better. I have no problem with people using equity from another investment as I do it myself. And I have no issues with people wanting to pay off their home.

My problem is that if you are intending to use the equity in your house you might as well not pay it off to begin with. All you’re doing is delaying the process. The 10 years that your dollars have been locked away in your house have essentially been wasted because there’s only two ways to make money in real estate, rental income and capital appreciation and you’re doing neither when you buy a home (unless you sell).

A home should be bought and paid off for security and peace of mind. When you withdraw equity from it you are no longer debt free and your home could be repossessed (worst case scenario).

Either invest before you start paying off a home, or, if you already have paid off your home please think back to why you wanted to pay it off in the first place and realise that when you withdraw equity from it, you no longer own it debt free. As tough as it sounds you need to start building your portfolio from scratch BUT it should be a lot easier to save for those who have paid off their home compared to most people since you have don’t have any house repayments to make.

Try to work out at the start what you want to do. Do you want to own your home outright, or do you want to start investing early. Pick one and then go after it! Do you know anyone that has paid off their home only to withdraw equity from it to invest with?

*For those who have discovered investing later in life please don’t take the heading personally. This article is more aimed at the people who actually plan to pay off their home only to withdraw from it. If you discover investing after you have paid off your home and then decide to invest your equity, that is completely different and I would say go for it!

by Aussie Firebug | Oct 28, 2015 | Classics, Investing, Mindset

Until I discovered the concept of FIRE at around the age of 24, my life was on track to becoming pretty ‘normal’. What is normal anyway? I guess it’s what the majority of the people around you are doing?

The ‘normal’ where I live goes something like this:

> Go to school and study hard

> Go to either Uni or get a trade

> Get a job after you have finished your degree/trade

> Find a partner

> Get married

> Buy a home

> Have kids

> Raise kids for the next 20-30 years

> Start to seriously plan for retirement

> Spend the next 10 or so years adding to whatever nest-egg you have in hopes that you can retire soon

> If you’re one of the lucky ones you retire around 60 with enough investments to see you live comfortably for the rest of your life

This model of ‘normal’ usually involved around 40+ years of 9-5 full-time work.

Let me repeat that. 40 years of work…

When I first started working full time I was blown away by how much life you actually lose each week. I knew the hours and that you work Monday to Friday, but it wasn’t until I actually started work that I felt like so much of my life was being wasted. I didn’t even hate my job either, in fact, I quite liked it. But there were SO many other things I’d rather be doing than my job. I knew there had to be a better way. I just couldn’t accept that a human being living in one of the richest counties on earth is required to work the majority of the day for 5 days a weeks for 40+ years in order to finally retire. Which is when I started to learn more about investing and the concept of FIRE.

If you know anything about investing then you most likely have come across the term ‘compounding interest’. Albert Einstein is quoted to have said

“Compound interest is the eighth wonder of the world. He who understands it earns it … he who doesn’t … pays it.”

If Einstein is saying it’s the 8th wonder of the world than you know it’s some pretty epic shit.

Compounding interest is when your interest earns interest. It’s basically like a big snowball that gathers more and more snow as it rolls down the hill. To get this snowball started you need to supply your own snow. But once you have ‘something’ started then the snowball will roll down the hill gathering little bits of snow along the way (your gains).

After a year of your snowball rolling down the hill slowly collecting other bits of snow, you discover that it’s grown by 5%. Because your snowball is now a bit bigger, the following year it gains even more snow since as it can cover more ground now. This has a flow on effect and after years of rolling down the hill, the snowball has grown to such a size that the amount of snow it can now collect after just a single year of rolling is enormous.

There are two critical components to compounding interest, the initial amount you start with and the time in which you start.

Let’s consider two different examples:

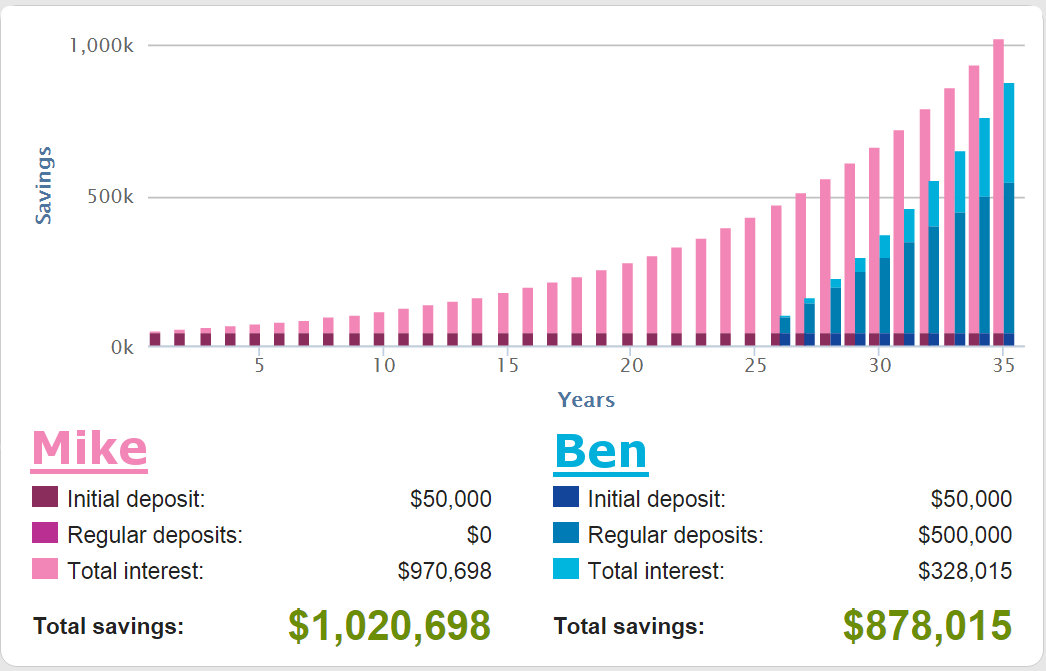

Mike is 25 and he decides to place his life savings of $50K into a savings account that returns 9% per year compounding annually (meaning that the additional interest is paid every year). He makes a promise to himself that this money will be used for his retirement and he must never touch a single dollar of it until he reaches 60.

Ben is also 25, but retirement to him is so many years away that it’s not remotely on his mind. He knows that one day he will probably need to save for retirement as he doesn’t trust that the government will be able to look after him once he can’t work anymore. Ben puts retirement on the back burner and YOLO’s through his 20’s, settles down in his 30’s and has kids.

The years fly by and suddenly Ben is 50. Ben and his wife start discussing retirement seriously and decide to start putting away a decent chunk of their income each year into a similar savings account that Mike used, this account also returns 9% per year compounding annually. Since Ben and his wife started their retirement account later in life they now have to sacrifice their lifestyle and scrap together all the spare change they can get. They miraculously are able to save a whopping $50K each year to add to their retirement fund.

Lets recap for a second. Mike invested a once-off lump sum of $50K at 25 while Ben and his wife invested a total of $500K ($50K X 10 years) between 50 – 60 years of age. Let’s compare how much money they have when they both turn 60.

Mike is represented by the pink columns and Ben and his wife by the blue ones. Mike ends up with over a million dollars in his account with Ben trailing by over $100K on $878K. Keep in mind that Mike made a once-off departure with $50K at 25. T

hat’s it.

He also YOLO’d his way through the rest of his life, he didn’t have to save a cent past 25, he didn’t have to sacrifice his lifestyle for 10 years saving $500K and yet he STILL came out over $100K ahead of Ben when they reached 60.

Mike had the power of compounding interest working for him for 35 years. During that time, his $50K nest-egg grew from $50K to over $1,000,000 dollars without him ever having to add or do anything to it.

Historically the S&P 500 Index has returned 9.04% with dividends reinvested so you might not be able to find a savings account that’s going to give you 9% (you won’t) but it is entirely possible that you could have invested $50K and have it return something close to 9% over 35 years. What I’m trying to say is that Mike’s story is entirely achievable. Yes, I left out a lot of things (market swings, inflation, income growth etc.) but fundamentally, if you start young and let father time do the hard lifting for you, It’s 100% possible to build a small fortune with little to no effort thanks to the power of compounding interest.

A Final Thought

I hope that you now fully appreciate the awesome power of compounding interest and how it can work in your favor. I think that the majority of people are doing it wrong when they hold off saving for their retirement. You should start young and be consistent with small amounts rather than trying to play catch up later in life. Get the snowball rolling now not later!

PS* The above graph was made from the smartmoney.gov.au site which can be found here. It’s a really great calculator that lets you compare two different strategies. Have a play with it and you will be astonished at some returns you can end up with if you invest early and consistently.

Photo credit: 401(K) 2013 / Foter / CC BY-SA

by Aussie Firebug | Oct 21, 2015 | Classics, Investing, Real Estate

With my most recent purchase of property number 3 I thought it would be a good chance to clear up any misconceptions about how much it really costs to buy a property and what are the hidden fees, extras and everything else involved right from step 1 to getting the keys.

Purchase Price

The most important part of the transaction. The purchase price is where you can really set yourself apart from an investor that knows what they’re doing as opposed to the investing n00b that rolls into a Metricon display home and picks a house off the shelf (this was actually me on my first IP LOL). It’s probably the most important part of property investing, sure you make a woad of cash over the years as compounding interest does its thang. But to really steamroll ahead in the investing game, getting a bargain on each property you buy is vital. It not only gives you a buffer in place in case you had to sell, but more importantly you will see growth WAY sooner than if you bought like 80% of people do, at market value or over.

Yes, I know what some are going to say “Whatever you buy at IS the market price”. True to an extent, but what really matters is how much the bank values the property at. And they usually undervalue the property a tad to mitigate their risk. So if the banks valuation comes back higher than what you paid for it, well done!

Deposit

The big one. All that hard work and years of savings form your deposit. How much deposit do you need though? Everyone has a different opinion on this one but here’s my take.

If you’re buying a home to LIVE in and not to invest then how big a deposit you put down doesn’t really matter. You probably want to avoid lenders mortgage insurance which is an insurance you have to pay for the bank when your deposit is less than 20%. Isn’t that funny? The banks see less than 20% deposits as high risk so they rightfully take out insurance to cover themselves in case you default on your loan. If that was to happen, the banks would get paid out by their insurer and the insurer would then come after YOU! The funny thing here is that you have to pay for the banks insurance. Imagine if every landlord started charging each tenant-landlord and home insurance because they see them as high risk. It just wouldn’t happen. But the banks have the mula $$$ and they make the rules. So us mere peasants just have to cop it on the chin…OR place down a 20% or bigger deposit.

If you are investing in property however my view on this is a bit different. You can put down less than 20% and pay the extra in fees (thousands of dollars extra depending on the size of the loan and your deposit %) if you are desperate to get into the market because you think it’s rising faster than you can save. For example, lets say that you want to buy an IP for $400K which would require a deposit of $80K (20%) but you only have $60K right now. A year passes by and now you have the extra $20K but now you discover that houses are selling for $500K instead, that means you would now need an extra $20K for your deposit. If you had bought the property at the start with a lower deposit, you would have had to pay the LMI but you would have seen a $100K increase in equity after one year which easily offsets the pain of paying the LMI.

Paying LMI in this case is beneficial but if the value of the property doesn’t rise then you will be stuck with a property with a loan to value ratio (LVR) of greater than 80%. The issue with having a property with an LVR of greater than 80% is that if you want to pull out equity, lets say upto 90% LVR you will have to pay LMI again 😐 . This actually happened to me on my first IP and was quite a shock. I’d already paid LMI to purchase the property but then they slugged me AGAIN when I pulled out equity. Lesson learned. I now only withdraw equity when my property is less than 80% LVR. The banks (my bank at least) allows me to pull out equity up to 80% LVR with no charge attached and it’s a pretty straightforward process.

I put down 20% for each IP that I buy these days but I don’t put down any more than that. Why? Because a 20% deposit I feel is the sweet spot for not only dodging such extras as LMI but also providing a big enough buffer in case anything went wrong and you had to get out.

Some people say the bigger the deposit the better. I disagree. One of my favourite ways to evaluate a property (or any investment) is to calculate the cash on cash (COC) return. The formula looks something like this:

COC = (INCOME-EXPENSES) ÷ CASH INVESTED

I like it so much because it can tell you how quickly you are going to get back your initial outlay that you parted with to buy the investment to begin with. Using this formula you can work out that it is not always the best idea to put down a bigger deposit. Lets for example say that you are looking at purchasing a positively geared house in the country that doesn’t have the brightest future for capital growth but has a really strong rental yield. The purchase price is $170K (yes these houses do exist if you look outside of capital cities) and it is currently tenanted at $290 P/W. Rounding the figures off lets just assume that all the expenses including interest, rates, water etc. all add up to be $9K P/Y. That’s roughly $15K a year from rent and expenses of $9K, which is fantastic positive cash flow straight off the bat of $6K P/Y. Lets say you purchased this deal with a 20% deposit. At 20% deposit you are forking out $34K plus 5% overall buying costs which brings you up to $42.5K OVERALL cash invested. If we plug that into the formula

COC = $6K ÷ $42.5K

COC = 14%.

Assuming no capital growth and not adjusting for inflation this means that at the current rate of return with all things being the exact same, I will get back my initial capital that I invested into this asset back after roughly 7 years. Every $ after those 7 years is pure profit. Now lets change the deposit size and see what happens to our COC return. Let say I was to only put a 10% deposit down instead of 20%. I’m now paying an extra $850 (assuming interest rate @ 5%) bucks each year because my loan is bigger and lets say LMI is going to cost me $3K. My cash flow now changes from 6K P/Y to $5.15K but my total cash invested also changed from $42,5K to $28.5K. So if we now plug those figures into the COC formula we then get the following

COC = $5.15K ÷ $28.5K

COC = 18%

The higher the COC percentage the quicker you get back the money that went into any investment. We could do the formula again with 0% deposit (banks don’t currently let you do this now, they did once upon a time) and the COC would be even bigger, sometimes over 100% meaning you’re making real money from the very get-go.

It’s all about how comfortable you are with risk. I’m not saying to put down the smallest deposit possible I’m just saying that purely from a mathematical point of view you are not always better to be putting down 30% to 60% deposits when you’re investing in real estate. If you want a place to live in then it’s different because your primary goal is not to make money. But if you are looking to make money from investing in property then there are better ways to do it then to put down a big 40% deposit on a property that’s going to take 40 years to generate enough income just so you can be back at square one from where you started from.

Buying Costs

This will vary on a number of things but I have used the 5% rule in the past and it has been pretty much spot on for all three of my properties so far. It’s pretty simple really. 5% of the purchase price is usually what it’s going to cost you to buy the property. This covers everything like building and pest inspections, stamp duty and legal fees. It’s a bitter pill to swallow sometimes because if you are buying a property worth $500K, using the 5% rule would mean you are paying $25K just to own this asset. That’s a LOT of money just to buy something which is why a lot of property investors don’t like selling once they have bought. It’s expensive to get into the market and even more so sometimes to exit. I would have to agree with this mantra. You lose enough money as it is through buying fees let alone selling ones. Below is my actual buying costs of the latest property to give you an idea not only of the prices but also the timelines on which I had to pay them. FYI the purchase price was $250K

| Date |

Expenses |

Notes |

| 27-Jul-2015 |

$1,000.00 |

Initial deposit |

| 29-Jul-2015 |

$400.00 |

Building and Pest inspection |

| 11-Aug-2015 |

$11,500.00 |

More of the deposit |

| 2-Sep-2015 |

$7,175.00 |

Stamp Duty |

| 16-Sep-2015 |

$37,900.25 |

Rest of Deposit |

| 16-Sep-2015 |

$2,078.83 |

Legal and conveyancing fees |

| 25-Sep-2015 |

$200.00 |

Settlement Fee |

| 25-Sep-2015 |

$728.40 |

Land Titles Office |

| Total |

$60,982.48 |

|

Conclusion

From my experience, I have found that I can quickly and easily work out how much it’s going to cost me to buy a property using the 5% rule and 20% of the purchase price. For me, it works out to be 25%. The 5% rule can be applied for most purchases but the other major part to the buying cost is the deposit which will differ from person to person. Do you always aim to put 20% deposit down? Maybe more? Maybe less? I’d like to know your reasoning behind it in the comment section below.

by Aussie Firebug | Sep 7, 2015 | Classics, Investing

Unless you have been living under a rock I’m sure you have heard of the term negative gearing. Some swear by it, others say that it is responsible for the outrageous house prices in the Sydney and Melbourne market. At the time of writing this, the current median house price in Sydney is $1,000,616 and Melbourne is $668,030! But what is Negative gearing, why do I think it’s for dummies (most of the time) and why doesn’t Negative Gearing’s cooler brother Positive Gearing get as much attention?

Negative Gearing Explained

The first thing to understand is the term ‘gearing’ which simply means to invest on borrowed money. Why would someone invest on borrowed money? Because investing on borrowed money allows you to get bigger bang for your buck (technical called leveraging), for example:

If I invested $50K straight into an Exchange Traded Fund that returned 10% annually I would make $5K in one year. But if I used that $50K as a down payment for a house worth $250K that increased in value to $275K over the course of one year I have successfully used leverage to my advantage. You see, even though the ETF had a better return on investment (ROI) of 10% compared to the house ($250K to $275K is a 9% ROI), the leveraged investment was able to return $25K compared to $5K from the ETF. This is possible because you are investing the same amount of capital but are acquiring a much larger asset.

Of course I’m leaving out a ton in the above example but that’s just to explain the basics and how gearing is meant to work.

OK so now you understand what leveraging\gearing is and how it’s meant to work. If we continue with the above example and break down the costs associated with holding the asset for one year and the income it produces (rent) it might look something like this

| Expenses |

|

Income |

|

| Management fees |

$1,000 |

Rent p/w |

$235 |

| Water Bills |

$600 |

|

|

| Interest Repayments |

$10,000 |

|

|

| Insurance |

$600 |

|

|

| Rates |

$1,600 |

|

|

| Depreciation |

$7,600 |

|

|

| Total |

$21,400 |

Total |

$12,220 |

Which would mean that the investment is negatively geared because the outgoings are greater that the income produced by the asset. You are basically losing $9,180 dollar a year to hold this asset. Why would anyone buy something that looses them money? Because they think they can make it back through capital gains. Which in the above example is correct since the house gains 25K and only loses around 9K.

While some people like to invest like this, it ain’t for me. The reason I don’t like this way to invest is because every year you loose REAL money out of your account and it affects cash flow position which impacts your lifestyle. You might not be able to go on that holiday every year if you were consistently having to fork out 9K on the investment property. You never see the capital gains money until you sell the house, your gains are only on paper until you actually sell. The house might be worth 25K more after year 1 and then 25K more again after year 2 but then the market slumps and your house is suddenly worth 40K less after year 3. Meanwhile your negatively geared asset has consistently been draining you of 9K yearly. It comes back to the basics of investing and for me my light bulb moment. You buy assets that make you money. Negative gearing is buying assets that loose you money with the hope of making that money back and more when you sell… No thanks

Pay Less Tax

What is unusual about negative gearing in Australia is that the law allows you to offset the tax you pay on your wage with the losses from an investment. Not all country’s allow you to do this. I’m not going into a lot of detail about taxes because it’s just too hard with so many different situations but the gist of it is that you can claim a deduction in your tax return from the loss you made on an investment property.

For example, if you earned 70K a year and you lost 9K with a negatively geared investment property the tax man looks at that and allows you to offset your salary of 70K by 9K thus your real earnings that financial year is 61K and not 70K. And this difference is the reason you can get a big tax return at the end of the financial year. Because you paid tax on the whole 70K throughout the year the tax man refunds you the tax you would had paid on the 9K which equals $2,925* using the income tax rates 2014-2015.

BUT!!!! You have to remember that even though you paid less tax and got a tax return of near 3K, you still lost 9K to do so. When you hear people bragging about ‘My tax return was $12,000 dollars this year how smart am I!’ just remember that they would have had to have lost a heaps of money in order to offset their salary to get that big of a return. The aim in property investing is not to pay no tax at all. It is to make the most money possible in the shortest amount of time with the least aggravation. There are ways to minimise the amount of tax you pay but your goals should never be paying not tax at all. Ideally you want to be paying loads of tax each year, because if you’re paying heaps of tax that means your making bucket loads of money. If you live in this wondering country of Australia you’re going to have to pay tax. Get over it.

When is it OK to Negatively Gear?

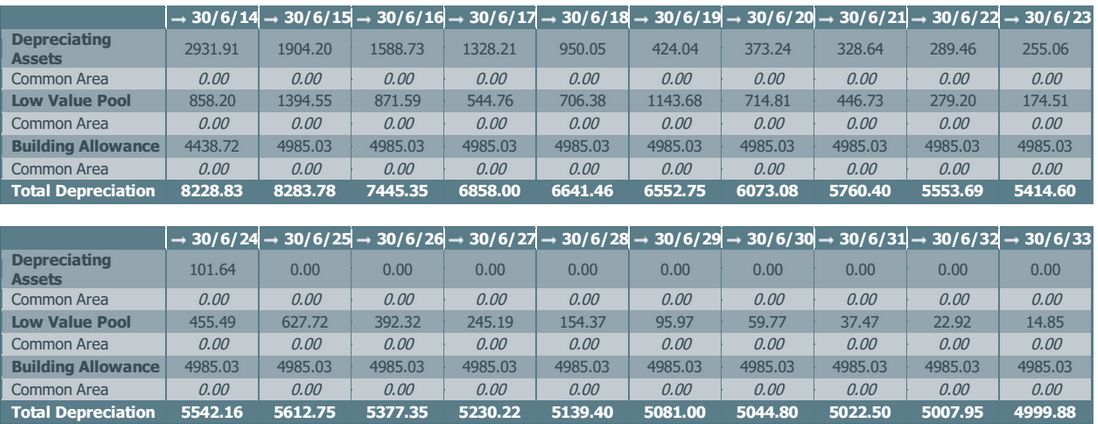

I’m going to sound like a massive hypocrite right now but all my properties are negatively geared BUT have positive cash flow increasing my ability to save cash for the next deposit. Huh? Didn’t I just say that negatively geared properties lose you money each year? Yes I did but there is one key category to the expenses of a property that makes it different from the rest. Depreciation! When you buy/build an investment property you should get a depreciation report made. This is basically paying a professional depreciator to come to your property and work out how much value things are going to depreciate by each year. The carpet might lose $200 value each year for the next 15 years, the deck might deteriorate by $400 a year for the next 20 years and so on. They value everything on the property and give you the value that the property loses throughout the next 20 or so years. Below is from a report of one of my own properties

The total depreciation at the bottom of every financial year is what my accountant is after to use in my tax return. The reason why depreciation is different to every other expense is that it does not affect cash flow. I technically make a lose on paper but I don’t actually have to give 8K to anyone, it’s simply what the property has lost in value during that time. My own cash flow position with my properties is that my rent covers ALL expenses and leaves me with a little left over. But when you factor in the depreciation I’m technically negative gearing even though I have a positive cash flow. For example:

| Expenses |

|

Income |

|

| Management fees |

$1,000 |

Rent p/w |

$350 |

| Water Bills |

$ 600 |

|

|

| Interest Repayments |

$10,000 |

|

|

| Insurance |

$ 600 |

|

|

| Rates |

$1,600 |

|

|

| Depreciation |

$7,600 |

|

|

| Total |

$21,400 |

Total |

$18,200 |

Technically I am losing $3,200 dollars holding this property. BUT the big difference with the above is that if you take out the loss from depreciation I actually have a positive cash flow of $4,400 dollars. Deprecation puts me in the negatives which is OK because that means I can then claim the loss on my tax return and get even more money in my pocket! The entire time I’m holding this asset I am having $$$’s flow into my bank account and not out of it PLUS I’m not even factoring in capital gains which may or may not be occurring. Capital gains is the gravy on top for me though, as long as an asset is cash flowing I continue to buy more of them.

Positive Gearing

And now finally onto the my favorite way to invest, Positive Gearing. You may have figured it out by now but just in case you haven’t. Positive gearing is when the rent you collect covers all costs including depreciation and leaves you with a surplus. You have to pay tax on this surplus but that’s OK because it’s extra money in your pocket and for me it’s better to be earning $1 dollar more and paying 37c tax than it is to be losing $1 and saving 37c tax.

So if positive gearing is so bloody fantastic, why is everyone doing it? Because it’s not easy to find positively geared properties straight off the bat. You can find them in places like mining towns and in the country but mining towns are usually extremely reliant on one industry and if the mine shuts you’re screwed. Country towns are OK but often lack that capital growth seen in the capital cities.

There are only two way to make money from Real Estate. Having positive cash flow from the rent (positive gearing) or having the price of the asset increase from when you bought it (capital growth). Nirvana is purchasing a positively geared property that will have big capital gains in the future. The thing about capital gains though is that you can’t really control it from the market perspective. Sure you can do a reno to increase the value of the house or something, but if outside factors come into play such as China slowing down, Australia going into recession or Europe going down the drain and the buyers market gets spooked and stops buying. Economics 101 ‘supply and demand’ tell us no matter how much you’ve improved the property it may be worth significantly less than what you’ve paid for it. In a rough time like this your cash flow will either help see you through so you can hold the asset until the market rebounds or it will cause you significant grief as you continue to fork out $$$ each week for an asset that is continually losing money. Cash flow is more manageable and easy to predict. You can see roughly what the properties similar to yours is renting for, work out the costs for repayments, rates, water etc. and get a rough idea if the property will be negative, neutral (doesn’t lose or make money) or positive. Outside influences that affect cash flow are usually less volatile too (interest rate, rent prices etc.).

Negatively geared properties should eventually turn into positive over time as rent rises. Realistically, neutrally geared properties in a highly sought area with good potential for growth are the ones I’m interested in. They don’t drain your pockets as the property looks after itself and with every rent increase you are slowly turning the property into the positive area while also having a property with great upside for growth. I would love to get a positively geared property with big upside for growth but the bottom line is they are extremely hard to find in a capital city without lucking out somehow. It is very possible to get neutrally geared properties in up and coming areas which will turn positive over time.

Wrapping Up

Negative gearing saves you paying tax but you lose more than you get from you tax return. If you are negatively gearing you must be 100% confident that the property is going to go up in value whilst your holding it. This is the only way you can make money through negative gearing. Next time you meet someone who is paying little to no tax using negative gearing just be aware that they are actually losing money until they sell and most likely don’t realise this. I only advocate negative gearing if you still have positive cash flow which is the method I’m currently using.

Positive gearing is where it’s at and all investors should be striving to get to this state because there is no good reason not to. The asset produces more income than expenses. Simply investing really, buy things that make you money. Positive gearing does this. Yes you pay tax but if you’re planning to become rich through Real Estate guess what? You’re ganna have to pay tax!

Thoughts, feelings, questions and emotions in the comment section below.

*Assuming that this person falls in the $37,001 – $80,000 tax bracket and is paying 32.5c for every dollar they earn

by Aussie Firebug | Aug 19, 2015 | Financial Independence, Investing, Retire Early, Saving

It doesn’t matter if you’re 16 or 60. You are never too young or old to start planning for retirement, and if you’re crazy like me then you would have wished you had started planning from your early teen years. But how do you know when you can transition to retirement? To answer the common question of ” How much do I need to retire ” there are basically two things that you need to measure before we can use the retirement calculator.

How much do you spend?

And I don’t want to hear rough estimates here. In order to accurately measure and plan for retirement you gotta know exactly how much money you spend each year in order to live at your current life style. This does two things. Firstly it will give you a quantifiable number (needed for the retirement calculator). You can now accurately say that I need $X.00 amount of dollars to live my life as it is right now during this time in history. Notice I mention this time in history because inflation matters, for example someone living in 1970 might have been able to live off $5,000 that year. But they might struggle to buy just coffee for a year with that sort of cash now days.

Secondly you will become aware of where every dollar that you earn goes. And this is going to really open up your eyes trust me on that! Even for someone who has been financially responsible their whole life. When you track your spending religiously you see just how many holes you have in your pocket and that money is constantly flowing in the outwards direction for heaps of shit that doesn’t really improve your life, I’m looking at you alcohol/smokes/designer clothes. Plugging these holes is another post altogether so lets just stick with tracking money for now.

So how does one exactly track their spending accurately? Well there are a few different methods depending on how trust worthy you are. The first is to simply keep an excel spread sheet/journal and fill it out as you go. Export your bank statements to a CSV file and add each transaction on your statements to your spreadsheet with a date, transaction detail, amount in $ and a category column so you can break down what you spent your money on. Something like this will work

| Date |

Transaction Detail |

Amount |

Category |

| 05-Aug-15 |

BP Petrol |

$ 54.36 |

Car |

| 05-Aug-15 |

Safeway |

$ 26.10 |

Groceries |

| 07-Aug-15 |

Revolvers PTY LTD |

$ 281.52 |

Entertainment |

| 08-Aug-15 |

McDonalds |

$ 24.20 |

Food |

| 08-Aug-15 |

Safeway |

$ 35.10 |

Groceries |

|

|

|

|

| Total |

|

$ 421.28 |

|

And with a bit of excel magic you can create a pie graph of your 3 day bender.

The other alternative (my preferred method) is to get browser based software to do this for you for free. There are a number of different Australian options you can choose from: Pocket Book, ANZ Money Manager and for any US readers I’m sure you have already heard of Mint. They all do basically the same thing when it comes to categorizing your transactions. You can log into your online banking and export data between two different dates and then upload it into the software. Once there the software will automatically try to categorize transactions based on common names in the transaction details. For example if the transaction detail has Woolworths in the description than odds are that this transaction should be categorized as groceries. You can always manually go through them to make sure that they are right, and the software is smart enough to remember your changes in case it gets it wrong first time. The only down side to this is that you have to export your data and upload it every time you want up to date info. To make this easier you can add you banking details to the software that enables it to have read only access to your data. This means that the software is always up to date with your transactions without you having to export/import all the time. If you are worries about security you can read up how it works here.

Once you have all your transactions in the software and categorised correctly you can really start to paint a picture on how much you spend and what you spend it on. Pocketbook has a great feature called ‘Analyse’ that creates a pie chart for you between two dates and splices it up based on categories. You can then deselect certain categorie and the pie chart will automatically re-size and show you what your spending would look like without that category for that week/month or whatever the time frame is that you’re measuring. It’s a really easy and quick way to sift through all the junk and find out how much you can actually live off without all the bells and whistles.

Now the last part to this question is all about that cash flow baby! How much does your investments make you? This can be a bit tricky because it depends on what you invest in and how volatile it is. Lets just assume that you are getting a solid return of 9% per annum forever with no fluctuations. Highly unlikely but for the purposes of this example lets just go with it. How much will you have to have invested before your portfolio generates your annual expenditure? Just plug in your figures to the following formula

E / R = FI

E = Yearly expenditure

R = Return rate as a percentage

FI = Financial Independence

Example: I spend $45,730.87 dollars and my rate of return from investments are 9%

$45,730.87 / 0.09 = $508,120.77

So based on the above I would need a portfolio valued at $508.120.77 that returns 9% per year and I would never have to work again!… Not quite. Inflation is the silent killer here. The Reserve Bank of Australia’s (RBA) inflation target is 2-3 percent, lets just use 2.5% for our calculations. We need to minus this percentage from our return rate of 9% and redo the formula.

$45,730.87 / 0.065 = $703,551.84

God dam inflation. Factoring inflation in has just increased our hypothetical FI number by nearly $200K 😐 … This is an evil necessarily though because it will enable your portfolio to grow along with inflation, enabling you to have the same purchasing power in 30 years time as you do today.

I have not covered everything* here but it should give you a basic idea of how to start calculating your FI number. Have a play with the retirement calculator below and see how drastic some simple changes can be such as lowering your living costs by as little as 5K or how much an impact your FI is affected by rate of return.

[CP_CALCULATED_FIELDS id=”6″]

*All calculations have not factored in tax because it’s just too hard to cover all aspects. You should be calculating using after tax money

by Aussie Firebug | Aug 14, 2015 | Investing, Net Worth, Saving

Net worth had a big jump last month (+$21,000) after both my properties got revalued and completing my tax return which showed that I had knocked off about $7,000 off my HECCS debt. July has seen a seen a steady increase of around $4,500 from pure cash savings.