Our third and last investment property (IP) has officially been sold 🎉👏

It was actually the second investment property that we bought and I’ve always referred to it at IP2 in this blog but we sold IP1 back in 2018 and IP3 a few months ago which is why it’s technically the third to hit the road.

Following the theme from the IP1 and IP3 sale articles, I’ll get straight to the point.

We turned $56,326into $119,094 over 8 years which works out to be an annualized after-tax return of 11.29%.

If you’re interested in all the finer details of how we arrived at that figure please read on.

The Numbers

IP2 was bought in SE Queensland for $169K in 2014.

Buying expenses

$2,000

Initial deposit

$380

Building and Pest inspection

$25,700

More of the deposit

$6,487

Rest of Deposit

$6,625

Outlays including stamp duty and Legal Fees

$200.00

Settlement Fee

$488

Land Titles Office

$9,900

Buyer’s agent fee

$200

Guarantee Fee

$200

Fee for attending settlement

I paid a 20% deposit to avoid LMI

I used a buyer’s agent because back in 2014 I was very time-poor. I didn’t have the time or desire to go up to Queensland to scope out the place and really do my due diligence so I outsourced it.

Actual money spent so far: $52,181

Cash Flow/Holding Costs

Cash flow

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Rent – Expenses

-$1,121

-$2,116

$1,148

-$1,202

$1,672

$64

-$3,144

-$2,041

Depreciation

$5,940

$4,556

$3,496

$2,799

$2,339

$2,036

$1,835

$1,702

Tax Refund

$2,613

$2,469

$869

$1,480

$247

$730

$1,842

$1,385

Total

$1,492

$353

$2,017

$278

$1,919

$794

-$1,302

-$656

Total cash flow over the 8 years = $4,894

Notes:

I had a lot of repairs that needed to be taken care of before I sold the property in years 7 and 8.

I’ve included depreciation and a tax refund even though this property was held in a trust and not in my name. This means that the taxable income of the trust was lowered but my personal income was not affected. It’s hard to measure the full effect of the depreciation so I just used a refund amount based on the 37c tax bracket as I did for IP1 and IP3.

I used the diminishing value method for depreciation.

Actual money spent so far: $47,287

Selling Costs

$635 – Conveyancing

$8,405 – Went through a traditional agent for the sale because the property was located in Queensland and I wasn’t in a position to go up there and host open days. The commission was a lot more than IP3 because apparently gold coast property has a premium attached 🙄

Total Selling Costs: $9,040

Total money committed to this investment over 8 years: $56,327

The IP was sold in November for $250,000

I invested $56,327 of my own money and received $119,094($250,000 – $135,800 + $4,894) 8 years later giving me an annualised return of 11.29%.

Return on Investment (ROI) and Tax

I used this website to calculate my return on investment for IP3. The formula was the following:

Annualized Return = ((Ending value of investment / Beginning value of investment) ^ (1 / Number years held)) – 1

And just like I explained in my IP1 Sold article, I’m only calculating how much of my money was spent, and how much cash I got back after I sold. Because that’s all that really matters IMO, it’s all about the cash on cash returns.

The tax bill for this investment will be washed through the trust and all of the gains will most likely go to my self-funded retiree parents or potentially my sister who has just had a baby and isn’t working. They will hopefully be kind enough to gift the profit back to the trust. So no tax be will be paid for this investment.

One last thing to note is that even though we had this property over 8 financial years, we technically only owned it for 7. So I used 7 in the calculations FYI

Why Did We Sell?

In a nutshell, selling our investment properties is part of our current investment strategy. We want to pump more $$$ into our index style share portfolio to create a passive income stream that will free us from the 9 to 5 grind.

Conclusion

Not much else to say really. I’ve been talking about going 100% passive for years and it feels awesome to finally be in this position.

The only thing left for us to do is deploy the $200K+ of cash we have sitting in the bank atm. We plan to debt recycling part of our PPoR loan with this money before we dump it into the markets but the details of that are in another article that I’ll hopefully publish before the end of the year (not long now).

Real Estate has been an incredible wealth-building tool for Mrs FB and I but there’s something super satisfying knowing the days of tenant issues are over… at least for now. We have no intention of jumping back into real estate in the future but ya just never know!

Our second investment property (IP) has officially been sold 🎉👏

I say second because we first sold IP1 back in 2018, but this IP was actually the third property we bought and I’ve always referred to it as IP3 on this site so it can be a bit confusing.

We still have one IP left (IP2) which hopefully will be sold at the end of 2021.

What Was The Return?

Following the theme from the IP1 sale article, I’ll get straight to the point.

We turned $65,313 into $126,298 over 6 years which works out to be an annualized after-tax return of 11.62%.

If you’re interested in all the finer details of how we arrived at that figure please read on.

The Numbers

IP3 was bought in SE Queensland for $250K in 2015.

Buying expenses

$1,000.00

Initial deposit

$400.00

Building and Pest inspection

$11,500.00

More of the deposit

$37,900.25

Rest of Deposit

$2,078.83

Legal and conveyancing fees

$200.00

Settlement Fee

$728.40

Land Titles Office

$9,900.00

Buyer’s agent fee

Stamp duty was added to the loan for this IP instead of paying it upfront.

I paid a 20% deposit to avoid LMI

I used a buyer’s agent because back in 2015 I was very time poor. I didn’t have the time or desire to go up to Queensland to scope out the place and really do my due diligence so I out sourced it.

Actual money spent so far: $63,707

Cash Flow/Holding Costs

Cash flow

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Rent – Expenses

$1,679

-$118

-$1,976

$711

-$1,285

-$1,989

Depreciation

$6,911

$4,117

$3,375

$2,872

$2,529

$2,293

Tax Refund

$1,935

$1,567

$1,979

$799

$1,411

$1,584

Total

$3,615

$1,448

$3

$1,510

$126

-$404

Total cash flow over the 6 years = $6,298

Notes:

I had a lot of repairs that needed to be taken care of before I sold the property in year 6 which was the most expensive year. Year 3 and 5 also had some pretty hefty R&M jobs too.

I’ve included depreciation and a tax refund even though this property was held in a trust and not in my name. This means that the taxable income of the trust was lowered but my personal income was not affected. It’s hard to measure the full effect of the depreciation so I just used a refund amount based on the 37c tax bracket as I did for IP1.

I used the diminishing value method for depreciation.

Actual money spent so far: $57,409

Selling Costs

$599 – Conveyancing

$7,305 – Went through a traditional agent for the sale because the property was located in Queensland and I wasn’t in a position to go up there and host open days

Total Selling Costs: $7,904

Total money committed to this investment over 6 years: $65,313

The IP was sold in June for $320,000

I invested $65,313 of my own money and received $126,2986 years later giving me an annualised return of 11.62%.

Return on Investment (ROI) and Tax

I used this website to calculate my return on investment for IP3. The formula was the following:

Annualized Return = ((Ending value of investment / Beginning value of investment) ^ (1 / Number years held)) – 1

And just like I explained in my IP1 Sold article, I’m only calculating how much of my money was spent, and how much cash I got back after I sold. Because that’s all that really matters IMO, it’s all about the cash on cash returns.

I know people like to crunch the numbers based on purchase and sold prices without factoring in leverage, but I just can’t see how this gives an accurate depiction of the investment when 99.99% of property investors use leverage when investing. It’s the only way real estate makes sense IMO.

The tax bill for this investment was washed through the trust and most of the gains actually went to my self-funded retiree parents. So just like IP1, we didn’t actually have to pay any tax for IP3.

I need to write another trust article that highlights our strategy when it comes to trust distributions because the trust is actually shaping up to be an enormous tax minimisation vehicle especially combined with debt recycling which will also be doing once our new home settles this month.

Why Did I Sell?

In a nutshell, selling our investment properties is part of our current investment strategy. We want to pump more $$$ into our index style share portfolio to create a passive income stream that will free us from the 9 to 5 grind.

Conclusion

IP3 wasn’t that much of a headache tbh. But it was still way more work than our share portfolio. I know hindsight is 20/20, but the share market would have actually made us more money in the same period of time with 0 work involved… 😑

But this is easy to say now in 2021 after a huge bull market. I’m still happy with the returns but it further illustrates to me that you really need to add value or solve a problem with real estate to make bank.

This may surprise some of you but I bought, managed and sold IP3 without ever actually seeing it in person 😅.

I paid someone a very high amount to do all the due diligence work for me so I was confident that the property was legit (I was still nervous until I received my first rent check lol). I also never improved the value of the property which is one of the biggest advantages I’ve always said property has over shares… the ability to physically add value. I seriously just bought it, dealt with a few tenant issues here and there and sold it 6 years later.

IP1 was very different because I put in the work (sweat equity) and physically improved the value of the home which was reflected in the sale price.

And now we only have IP2 left which we will be putting on the market later this year 🙂

I’m so glad I can finally crunch all the numbers for you accurately now it’s been sold because you never quite know how much your true return will be until you actually sell your investment property.

Without a doubt the most interesting question on most peoples minds would be:

‘So how much did you make?’

To cut a long story short, we had an annualized after-tax return of 36.48%.

If you’re interested in all the finer details of how we arrived at that figure please read on.

The Numbers

This IP was built in south-east Melbourne for $340K in 2013. I lived in it originally to receive the FHOG.

Buying expenses

$30,000 – Deposit ($9,000 from me plus $21,000 FHOG)

I borrowed 91.33% of the property plus LMI. I would not recommend this but that’s what I had and the banks were allowing it back then. I wouldn’t have got that loan in today’s market.

$4,634 – LMI even though my parents could have gone guarantor (no hands out for me)

I built this house so there were no expenses for conveyancing or stamp duty. All the loaned money went to the builder who was selling land and house packages.

I had a loan of $319,815 (the LMI got attached to the loan plus some other expenses).

Actual money spent so far: $9,000

Sweat Equity

$3,840 – Landscaping. A new garden for the front, back and sides. Plants, pots, mulch, stones etc.

$12,000 – Built a deck. Materials, building permit, labour help costs

$1,400 – Concreating

$4,410 – Other costs. Materials, Skip bins, money spent on food and other things while renovating etc.

I spent countless weekends with my old man and mum going up to the house to add value to it. This not only saved us money, but I also learnt a bunch of new skills. Win-win.

Total: $22,061

Actual money spent so far: $31,061

Cash Flow/Holding Costs

Cash Flow

Year 1

Year 2

Year 3

Year 4

Year 5

Rent – All Expenses

-$7,590

-$3,929

-$2,744

-$3,047

-$5,841

Depreciation

-$8,228

-$8,283

-$7,445

-$6,858

-$6,641

Tax Refund

$2,654

$4,519

$3,770

$3,664

$4,618

Total

-$4,935

$589

$1,025

$617

-$1,223

Total cash flow over the 5 years = -$3,927

Notes:

The first year I had to live in the house for 6 months receive the FHOG. This meant that I couldn’t claim all of the expenses for that year. Only for the 6 months I had it as an investment

I ended the lease with the tenants and cleaned the house up a bit which is why year 5 is so expensive. I had to cover interest repayments for a few months before the house was sold.

Depreciation is not including in the cash flow because it’s not an actual loss of cash flow whereas the tax refund is money coming into my account

I used the diminishing value method for depreciation. Don’t ask me why it somehow depreciates more in year 2 than year 1 🤷, that was what was on the report.

Tax refunds are based on the 37c tax bracket

Actual money spent so far: $34,986

Selling Costs

$700 – Conveyancing (had a friend do it cheap)

$2,210 – Used an online agent to sell the property. No way I’m paying 2.5% plus marketing just to list it on RealEstate.com and host a few open days

$3,850 – Staging. Maybe unnecessary but I like to think it worked

Total Selling Costs: $6,760

Total money committed to this investment over 5 years: $41,746

The IP was sold last month for $512,500

I invested $41,746 of my own money and received $197,697in return over a 5 year period.

ROI vs ROI On Money Invested

Way too often when anti-property commentators are trying to convince investors that another market has had superior returns over the last X amount of years they usually leave out the most important part of the equation.

Property investors use leverage to buy their investments.

Without factoring in leverage, I don’t understand how anyone can make blanket statements about the true returns of real estate. It’s not comparing apples with apples.

With that said, I want to provide you with both returns numbers so I can further illustrate the point that the only real return number you should be measuring is how much money you put in and how much you get out.

ROI

Capital Gain = (gain from investment – cost of investment) / cost of investment

I’m not 100% sure I can simply plus the two return figures together since one is annualized and the other is just an average rent of $360 per week (maths wizards please correct me). But the overall point still stands that the investment doesn’t look great without leverage.

The above calculations are assuming that we buy the property outright. This would mean no interest repayments or LMI costs.

12.98% may sound like a decent return, but what’s not factored in is the 100s of hours of labour and travel spent on this property to achieve this result. Considering you could have got better returns from shares over the same time period with no work required, you’d be mad to buy an investment property outright.

I have not factored in the replacement costs as the house depreciates. This hidden bill will rear its head eventually. Something shares don’t suffer from.

ROI On Money Invested

This one is a lot easier to work out and the true measure of the investment, not an assumption.

ROI = (gain from investment – cost of investment) / cost of investment

= ($197,697 – $41,746) / $41,746 = 373.57%

Annualized Total Return = 36.48%

Tax?

In an extremely fortunate turn of events, IP1 became my PPOR after I first moved in to receive the FHOG.

Investment property 1 taught me more life lessons than any investment in the future ever will.

It was the first house I ever bought, renovated, sacrificed countless weekend adding value to it with my old man helping me out and a whole raft of issues that I had to figure out along the way. From dealing with tenants, discovering how many hoops you have to jump through with banks, lodging insurance claims, rushing to finish the concreting in 38-degree heat (would not recommend), hosting open days and so much more.

Some say property investing can be passive. IP1 was definitely not passive!

It was hard work which did eventually pay off in the long run. Now, how much of its success can I take credit for? That’s a very good question.

Looking back in hindsight I can point out a few key things that happened that I had nothing to do with and was 100% luck

FHOG being available boosted my deposit meaning I only had to put down $9K (crazy)

The banks lending criteria was completely different back then. No way I get a loan in today’s market only having $9K to put down

For the majority of my loan, interest rates were being cut. Every couple of months I had to pay less and less in interest which at the time seemed cool but it’s only with hindsight I can truly understand how fortunate of a time it was to be in real estate. It has only been the last 18 months I have seen my I/O loans rise in rates

Melbourne experienced a property boom basically the whole time I had the property. It was only the last 3 months that the prices started to drop and the loans market really tightened their belt. The property was actually under contract before I sold, but it fell through because the buyer couldn’t get finance. I experience this two more time (not officially under contract though) before I had a buyer who was cashed up. Based on what similar properties were selling for, I estimated that IP1 dropped by around $30K since the start of 2018.

I fully admit that all of the above was unforeseen, I was just hoping for the property to keep up with inflation and use leverage to amplify the gains.

One of my favourite quotes of all time comes from the Roman philosopher Seneca.

I’m a big believer that you can create your own luck. Whilst I still think that the majority of the return from IP1 came from an uncontrollable event (market boomed), there were things that definitely helped bolster the profits that were in my control.

I actually identified the FHOG as an opportunity not to be missed. I signed my contract on the 29th of June which was one day before they scraped the FHOG all together back in 2012. This opportunity was available to all my friends, but most of them did not take it

I realised that it was unlikely for me to make a lot of money if I paid for everyone else to do the work for me. I looked to physically add value where I could and since I was full of enthusiasm and energy back then. Countless weekends were spent working on the house. Sacrifices were happily made if that meant I could reach my goal of FIRE quicker

I sought advice from experienced property investors who knew what to look for when investing…my parents of course! I understand this luxury isn’t available to every but it’s worth seeking one out if you can. There were small things that helped the investment like buying near public transport, schools, amenities, easy access to the M1, in an area with strong employment options and projects scheduled for the future etc.

Getting out of my comfort zone to learn new things such as selling IP1 online saving over $15K in commission fees. The experience I gained from negotiating the deals was invaluable. Some might argue that a skilled and experienced agent could have secured a better sale price. That may be true but we’ll never know. What I do know is that I saved over $15K doing it myself and I’m choosing to save $15K over potentially getting a higher profit every day of the week!

Why Did I Sell?

The strategy moving forward is to sell all the investment properties and transition to a more cash flow portfolio of ETFs/LICs. IP1 was the first cab off the rank for the following reasons

The market had gone bananas and I was very keen to lock in that profit and not risk something happening, which sorta happened with the market pullback in the last few months. But I’m very happy with the return we got so no complaints here 🙂

I would have reached 6 years next year which would have affected the main residence status for tax purposes. This means that I would have had to pay taxes on part of the sale

There was some upkeep work that I was fed up with. IP2 and IP3 are part of a body corp which takes care of a lot of the maintenance.

Whilst IP1 had gone up considerably in value, the cash flow was still shithouse! Technically positive cash flow after the tax refund during the last few years (apart from the selling year due to the extra costs). It still was nowhere near as good as what shares could offer for half the investment.

Conclusion

Overall IP1 has been a very successful investment in terms of both return and life skills obtained. I was very fortunate to be in the market during the time I was and I’m pretty confident in saying that I’m most likely never going to make as much money in any other investment ever again.

This may sound like a bummer but the truth is that IP1 was a hell of a lot of work! I can’t be effed doing all that again and I doubt I will have as lucky timings with the market twice. It’s a risk I don’t have to take and Strategy 3 suits our current lifestyle better being so passive.

What’s really hard to measure and has not been factored into the above return is all the physical work required. It was essentially a side hustle I did on weekends (not every weekend but a lot). If I deducted the hours worked * an hourly rate, the return would be less.

I’m still a fan of property investing for the right investor, but I am no longer the right investor and will continue with our strategy of selling off the other two IPs when the times right. It’s my opinion that there are more problems to solve with real estate and more opportunities for those who seek the challenge vs shares.

How has your experience been with real estate? I would love to hear from others positive or negative in the comment section below 👇

Preface: When I talk about shares in this article, I really mean ETFs. I don’t buy individual shares or day trade.

Collingwood vs Carlton

Sydney vs Melbourne

Magic vs Bird

Just some of the biggest rivalries the world’s ever seen.

But in the investing world, there is not a more hotly debated topic among avid investors. Property vs shares is a topic that everyone seems to have an opinion on, no matter how ill-informed they are.

Owning 3 investment properties and nearly $90K worth of ETFs (shares), I feel I have tasted the best of both worlds (and the worst) and can give you perspective to what I’ve learned over the last 5+ years of investing in these two asset classes. Both are great when used right, with pros and cons for various financial situations/types of investors.

But which one is right for you?…

Contestant 1: Property

The hometown favorite. This guy has been around longer than the stock market has existed!

You can touch and feel him, and your mum most likely loves the idea of you being with him. He has a strong track record in Australia and there is a firm belief that his value never goes down.

Now for realz:

Property is a great investment class but you need to be the right type of investor and have the financial stability for it to be used correctly. It’s an active investment. You’re going to have to do some sort of work to keep this investment running. You can minimize the work needed by hiring people but there are still headaches trust me.

However! Property has BY FAR the most potential to accelerate your wealth compared to shares for three reasons.

Cheap leverage

Ability to physically add value to your asset

Skill and experience actually mean something (more on this below)

Cheap leverage is often misunderstood. Too often an article is published with statistics on how shares have outperformed property by comparing the % of capital growth and rental/dividend returns.

This is a dumb way to compare the two because I don’t know any property investors that buy real estate outright. It’s almost always bought with a loan. Which means the asset is leverage.

But what does this have to do with returns you might ask?

Here’s an example (for simplicity we are ignoring buying and selling costs and tax):

Property 1 is brought in 2016 for $500K with a 20% deposit of $100K. That same investor also buys $100K of shares in 2016 too.

Fast forward 1 year and the house is now worth $600K and the shares worth $150K

Let’s make it simple and say that the shares have no dividends and that the house had $0 net gain/loss factoring in everything.

The shares made a whopping 50% return in one year. The property on the other hand only made a 20% return.

Which investment did better?

Going percent wise the shares beat the pants of the house. More than doubled its return. But hold on.

If we actually compare how much money each investment made, it tells a different story.

It cost the investor both $100K to buy each asset. Property made a total of $100K in a year whereas the shares only made $50K.

This is because of the power of leverage. You technically can leverage with shares but not for the same cheap rate and you get nasty margin calls which you don’t get with property.

The ability to physically add value to your asset is where I would say active investors have a clear choice with which investment they choose.

Sweat equity is a proven wealth building technique that’s been around for centuries. You would have to be extremely unlucky to physically add value to your property and not have it go up in value.

Experience and skill is a very interesting point to look at when comparing shares and real state.

The entire premise of index-style investing goes something along the lines of:

“It’s impossible to beat the market over a long period of time unless your names Warren Buffett. Even if you do manage to do so, it’s almost always luck. People spend all day every day studying stocks and graphs and still get it wrong. So what hope do you have as an ordinary Joe Blow? Don’t even try to become a master of the stock market because there is only such a very very small percent of humans alive that seems to be able to get it right the majority of the time”

Now, here’s the difference. Skill and experience actually matter in real estate.

A skilled and experienced property investor has a very good chance of repeating his/her success over and over again. In fact, they most likely get better at it as times goes on. The same cannot be said for the stock market (except for those very rare people like Buffett). A skilled and experienced property investor will beat the pants off a skilled and experienced stock trader over a 7-10 year period 9 times out 10.

You can’t really be skillful in picking stocks. You definitely can’t be skillful in picking ETFs either. Sure, you can be smart about your allocations to reduce risk. But it’s not like an ETF investor of 30 years is going to blow out a brand new ETF investor in terms of returns. In fact, they should get relatively the same return. And that’s not a bad thing either.

Contestant 2: Shares

3 things.

Diversification

Low buy in and selling costs

Easy peasy with hardly any management required

Have you ever heard the phrase ‘don’t keep all your eggs in one basket’?

The stock market gives you the ability to buy things called ETFs which is a slice of a lot (>200) of companies bundled up into one very convenient share. So instead of buying 200 individual shares. You can just buy things like ETFs and you get that vast diversification in one transaction. Couldn’t be any easier.

And the good thing about the stock market is the low buy in and sell costs. I pay $20 for around $5K of ETFs. Times that by 40 and I would have paid $800 for $200K worth of shares.

Think about how much it would cost you to buy a unit for $200K. Probably around $10K if we use the 5% rule.

And then you would have to sell it for anywhere between 2-3%.

When you want to sell shares there is another brokerage cost of around $20 per sell (depending on how much you sell).

This low buy in and sell costs are very convenient when compared to real estate.

And the last point I want to make is also one of the most important points. How little of your time and effort you have to put in for it to make you money.

And check up on your shares after about 7-10 years and get a pleasant surprise that on average, they have increased by around 9%

They only thing required during these 7-10 years is declaring the income earned through dividends on your tax returns which you can download electronically. No need to keep your own records.

THAT’S IT.

You didn’t have to manage anything and your investments returned a respectable 9% over 7-10 years. This extremely low management style is a phenomenal advantage.

Pros and Cons

Property

Pros

Cons

Leverage on low-interest rate

Ability to physically add value to investment

Skill and experience can be leveraged

High return potential for an active investor

Tax advantages such as neg gearing, depreciation and PPOR capital gains exclusion

Good protection against inflation

Less volatile than other asset classes

Active investment.

Requires a lot of capital to get started

Big buy-in (5%) and exist (2-3%) costs

Not diversified. One asset class in one location

Loan stress

Potential for things to go wrong. Leaking pipes, dog pees on the carpet, house burns down etc.

Not very liquid. May take you 6-12 months to cash out of this investment

Cash flow dependent. Needs a big buffer for incidents

If something goes horribly wrong. It can ruin you financially

Shares (ETFs)

Pros

Cons

Passive investment. Very little time and effort involved (less than one day a year)

Extremely diversified

Low entry and exit fees

Very liquid. Can break up shares and sell only a few units if that’s what you need

Easy peasy to do a tax return. No bookkeeping required

Franked dividends

At worst you can only lose what you have invested

Can’t physically improve investment or add value to asset

No influence on how your investment performs. If the market is down there’s not much you can do

Can’t leverage at the same low-interest rate as property

If you do leverage (which I wouldn’t recommend), you may get margin calls

More volatile

Fewer tax advantages than property

So Which Ones Right For Me?

It all comes down to what type of investor you are. Are you an active or defensive (passive) investor?

‘The defensive investor is unwilling, or unable, to put in the time and effort required to be an enterprising investor. Instead of an active approach, the defensive investor seeks a portfolio that requires minimal effort, research, and monitoring.’

My rough guess is around 95% of people are passive investors.

That’s because the majority of everyday people don’t really care for finance in general and would rather be doing others things they find interesting.

But since you’re on this blog, it means you find finance stuff interesting. What a sad bunch we are ?!

If you’re a passive investor I think the answer is clear.

Shares are clearly suited for the passive investing style while still giving the investor a great return.

Coupled with great diversification, low buy-in and selling costs, no loan stress, liquid asset (can get your money out in 2-3 days), it makes for the ultimate passive style investment!

But if you’re in that very small group of investors that want to take an active approach, you’ve gotta ask yourself.

Are you REALLY an active investor? Do you REALLY want to manage your investments for potentially the next 10-15 years? Will your circumstances change? What happens if you have a few kids? Do you still want to be managing your investments on 4 hours sleep?

Do you have a lot of capital lying around for a deposit?

How’s your cash flow position? Could you afford to pay an extra $1,400 a month when you don’t have a tenant in?

Is your job stable?

Do you have a big cash buffer in case anything goes wrong?

If you answered yes to all the above then maybe you are suited for investing in property.

I have made money using both investment classes. They each have their own merits and downfalls.

Whichever one you choose to invest in, just make sure you educate yourself before taking the plunge.

If/when you get to a point in your life where you own multiple properties, you will no doubt come across the term ‘cross collateralisation’. It’s a very important loan structure issue that you must fully understand if you ever do decide that it’s the best option for you. Many mortgage brokers (my first included) don’t actually understand the full implications themselves and are more than happy to sign you up for it because it’s usually an easier process. Cross collateralisation can very rarely be a good option, the majority of the time it simply increases the investors risk and strengthens the banks position of power.

Cross Collateralisation Explained

Cross collateralisation is when you use house A as security for purchasing house B.

Lets look at how you buy a house in the first place. THE most important thing when buying is….THE DEPOSIT! Banks love that shit. If the deposit is big enough you can pretty much guarantee that the bank will approve your loan.

No Job? No Education? No prospects?

Got a huge deposit, no worries. (I’m talking like >70% here guys)

It’s important to understand what the actual deposit means to the banks. It’s their way of lowering their exposure to risk.

Think about this. If you buy a $400K house with a 20% deposit that means the banks lent you $320K. Worst case scenario for the banks is you default on your loan and they are forced to sell to recoup their investment (the loan). They are not worried in the slightest about making money from this property, they just want their money back asap.

Ever wonder why you always hear of these stories of foreclosure bargains? It’s because the banks could not give two shits about an extra $10K, $20K or $40K. That’s pocket change to them. They just want to get back what’s theirs.

So now they have this house which the owner paid $400K for. Unless there has been a big downward swing in the market you would surely think that the banks could at the very least sell it for somewhere near the $320K mark. If they do then relatively no harm done, they loaned out $320K and got back their investment. No money made but minimal lost…except if you’re the poor sod that applied for the loan. You’re probably down the shitter now but like the banks care right?

So as you can see, the deposit is king to the banks and without a decent sized one (at least 20%) you are likely to pay exuberant fees to get the loan approved.

So why have I explained the above? Well as I have already mention, deposit is king. But what if I told you there was a way to get a loan approved without having to fork out one dollar? With the flick of a pen you can have access to hundreds of thousands of dollars.

Sounds too good to be true.

Enter Cross Collateralisation.

No Such Thing As A Free Lunch

Cross Collateralisation uses equity as the ‘down payment’ instead of cold hard cash. To simplify things, lets assume we have $200K of untapped equity on our family home (House A). We want to buy House B for $400K but don’t have a deposit.

To secure the loan we can use the equity from House A as collateral. This essentially does the same job of lowering the banks risks, just utilizing a different method.

House A Loan: $300K

House A Value: $500K

House B Loan: $420K (loan includes 5% buying costs)

House B Value: $400K

Security: $500K + $400K (the value of both properties)

There will be a section in the loan contract that details that this loan is secure using another property over which the lender holds it’s mortgage.

‘Wow that’s pretty cool isn’t it? Didn’t even have to save any money to buy another property and the banks made the loan contract a breeze. I’m going to buy all my properties from now on using this method’

You must consider the ramifications first.

1. Selling Headaches

Every wonder what happens when you want to sell the property that you used to secured the others?

To put it simply…Whatever the bank decides is going to happen.

They have complete control over the proceeds of the sale. I hope you didn’t have anything planned for the money you were going to get when you sell House A. Because the bank has just decided that House B is at a higher risk than when you first bought it and now requires your loan to be at 70% LVR. So that $200K you just received is going straight to the loan on House B…Nothing you can do about it.

And if you think that’s bad. Imagine a situation where you have secured multiple houses with multiple other houses…shit show.

2. Equity Withdrawals

At the moment, if I want to withdraw equity from one of my properties it’s super simple. I apply for the withdrawal and as long as I’m keeping it under 80% LVR there are minimal hoops I have to jump through. I’ve done this three times now (once for each of my IPs) and it’s been very straight forward.

There has been times though where one of my properties have gone up in value and the others have gone down. Because my properties are not cross collateralised I am able to access the equity from the IP that went up because they are seen by the banks as separate .

If you have all your properties cross collateralised however the bank views all of them as the same. You might have had one IP go up by $50K but the others go down by $30K each. This would mean you can’t access the equity on the one that went up which may impact your opportunities moving forward.

3. Want To Swap Lenders?

‘Hey look at that! CBA has been ripping me off with their high interest rate. I’m going to move all my loans to the lower rate at Ubank’

People do this all the time. The problem with Cross Collateralisation is that you can’t just move one or two loans across. You have to either move everything or nothing. Depending on who you’re going to they may not want that level of risk exposure. They might charge extra fees for having to value all the properties to determine the position.

In short it’s a pain in the ass for a process that is so much easier for stand alone loans.

4. Complicates Things

The extra paper work you have to complete only increases the more you cross collateralise.

Want to sell? Complete evaluation of your entire portfolio (assuming you have cross collateralised your entire portfolio).

Want to withdraw equity? Complete review of your financial position on all properties.

Want to move banks?…. You get the picture.

What To Do?

If you discover cross collateralisation exists in your portfolio without you even knowing it (happens all the time) there are a few things to consider.

Cross collateralisation isn’t a problem… until is it.

What I mean by that is that it’s perfectly fine to cross collateralise if nothing goes wrong. But the odds of something undesirable happening increase when you cross collateralise and it usually only benefits the bank.

If you want to uncross your loans go see a mortgage broker who can assist you and work out a plan of attack.

Stand Alone Loans

You really want all your loans stand alone. The only advantage I really see for cross collateralisation is the convenience of setting them up. The banks really like to strengthen their position so they make it super easy to cross collateralise.

The thing is, if you have equity. You can withdraw the equity as cash and use that cash as a down payment for a new loan. I have utilized this method in the past and have had great success with it.

You have to check with your lender on the conditions for equity withdrawal but if you can do it, it’s a much smarter way to buy your next investment as opposed to using cross collateralisation.

Wrapping Up

Cross collateralisation may be convenient and appealing for investors looking to buy a new property without using their own money. However, cross collateralisation rarely is a good thing and the majority of the time it does nothing but cause headaches later down the track. The banks prefer cross collateralisation because it strengthens their position of power and they have all the control.

If you have equity available, look to withdraw this equity as cash to use as the down payment for the new loan. You might have some short term pain with a bit more paperwork and a few more hoops to jump through but your future self will thank you for laying the foundations of a strong portfolio now rather than later.

It’s a decision most homeowners know all too well. Fixed or variable Rate? Do I fix my interest rate? Or do I go variable? Will the rate go up and I’ll feel like a champ if I fixed? Or will it continue to drop and I’ll just not tell anyone how much more I’m paying every month?

To Fix, Or Not To Fix?

There are some pros and cons for both. The main arguments made for fixing often include:

– Stability with repayments

– Laughing at others when rates rise

While the downsides usually are:

– Can’t make extra repayments

– Have to pay fees to set it up

– No offset

– No redraw

– Big, expensive, want to make you burn down the bank break feesif you ever decide you need out

– Crying internally if rates drop

Variable is basically the opposite of above where you have a lot more freedom and flexibility with your loan. You do pay for this extra freedom however by exposing yourself to more risk.

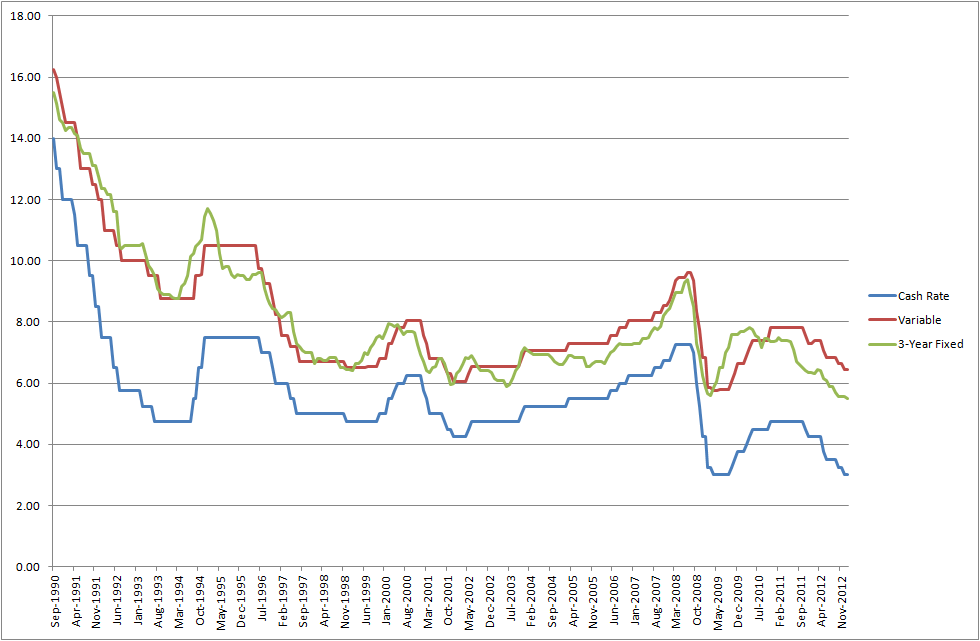

What’s interesting is that at the moment of writing this article you can find plenty of fixed rates that are lower than variable. I had a quick look at some historic fixed or variable rate data and it seems that this is not so uncommon.

Source:RBA

I was under the impression that fixing your rate usually meant that you pay a higher rate but upon further research, this wasn’t the case.

So if a fixed rate is lower than your variable AND provides the security of a fixed rate, there’s no reason I shouldn’t fix right?

Yes and no.

Make no mistake about it. The banks are ALWAYS aiming to make the MOST profit at ALL times. If you think you will pay less by fixing your loan for 1, 3 or 5 years after you have factored in all the extra fees and potential rate movements then, by all means, go for it. But just remember that the banks have an army of analysts that are betting against you. Just look at the above graph and try to find a couple of years where fixing your loan will come out ahead.

And remember that you have to factor in the fees associated with setting up the fixed loan and keeping it.

$750 Rate Lock fee. Applies to each Rate Lock. Only available on 1-5 year periods

That’s $1,446 in fees straight off the bat. How much of an interest rate hike would be needed for you to recover those losses and come out ahead vs variable? It depends on your loan and rate but there needs to be a BIG rate hike. And that’s just for one year. If you decided to fix for 5 years, the fees are spread out that’s true. But again, take a look above and try to pick any date where a 5 year fixed rate would still be lower than variable during its whole lifetime and by how much?

Are you starting to see how hard it is for this to actually pay off? There have been certain periods of time where fixing has been better no doubt about it. But how good and confident are you that you can get the timing right? The banks have an army of people working full time on this stuff and STILL get it wrong.

I truly believe that you’re gambling if you’re trying to fix your rate to save money. And the ones that win 90% of the time are the banks.

If you’re fixing for stability or peace of mind then that’s different. But don’t think for a minute that the odds are in your favor by fixing. If you do actually come out ahead it will almost certainly be because of luck and not your amazing analytic skills that you predicted that the banks didn’t.

Split Loans?

I’m not a fan of split loans because it’s sort of like taking the worst bits from each loan type and combining them into a shit sandwich.

Let me explain

Some of the main benefits from variable are:

– Loan flexibility

– Being able to refinance if needed

– Benefit from rate drops

– Offset and redraw

– Can pay off the loan at any rate you want

You get half of the offset, rate drop and redraw (assuming you split 50/50) which is Ok but none of the other benefits.

You still can’t refinance the entire loan, you still can’t pay off the entire loan.

Your flexibility is about as good as a pair of chalk hamstrings

You’re taking on all the risks associated with variable but not benefiting from all the advantages.

The main benefits of a fixed loan are:

– Stability with loan repayments

– Protection against rate rises

You lose both of those things with a split loan. Yes, you’re only going to have increased repayments from half the loan if rates do rise but then what was the purpose of fixing half the loan if your paying establishment fees for the fixed loan which will probably be more than the interest repayments from the rate rise???

And you’re stability is gone too because you still have the potential to pay more from the other half of the loan if you split.

But you still have to pay the setup fees plus you’re locked into the loan.

You’re getting nowhere near the benefit of either strategy but all the negatives from both. If you want stability and certainty then go with fixed. If you can handle rate rises, go with variable.

Wrapping Up

Maybe I’m wrong with my analysis of ‘fixed or variable rate’ and maybe I’m about to be blasted in the comment section about all the people who have ‘beat the banks’ by fixing their loan at a certain time. I’m a variable man, the flexibility, and freedom of a variable based loan is something that appeals to me. I think that fixed loans were invented by the banks to prey on the Ned Flanders of the world (the over cautious) and take more money from them by giving them peace of mind. That being said, if a rate rise means that you’re going to default on your loan, then you should definitely fix because you’re most likely overextending yourself financially. For the rest of us, riding up and down the variable roller coaster is financially better, for the majority of the time