Preface: When I talk about shares in this article, I really mean ETFs. I don’t buy individual shares or day trade.

Collingwood vs Carlton

Sydney vs Melbourne

Magic vs Bird

Just some of the biggest rivalries the world’s ever seen.

But in the investing world, there is not a more hotly debated topic among avid investors. Property vs shares is a topic that everyone seems to have an opinion on, no matter how ill-informed they are.

Owning 3 investment properties and nearly $90K worth of ETFs (shares), I feel I have tasted the best of both worlds (and the worst) and can give you perspective to what I’ve learned over the last 5+ years of investing in these two asset classes. Both are great when used right, with pros and cons for various financial situations/types of investors.

But which one is right for you?…

Contestant 1: Property

The hometown favorite. This guy has been around longer than the stock market has existed!

You can touch and feel him, and your mum most likely loves the idea of you being with him. He has a strong track record in Australia and there is a firm belief that his value never goes down.

Now for realz:

Property is a great investment class but you need to be the right type of investor and have the financial stability for it to be used correctly. It’s an active investment. You’re going to have to do some sort of work to keep this investment running. You can minimize the work needed by hiring people but there are still headaches trust me.

However! Property has BY FAR the most potential to accelerate your wealth compared to shares for three reasons.

Cheap leverage

Ability to physically add value to your asset

Skill and experience actually mean something (more on this below)

Cheap leverage is often misunderstood. Too often an article is published with statistics on how shares have outperformed property by comparing the % of capital growth and rental/dividend returns.

This is a dumb way to compare the two because I don’t know any property investors that buy real estate outright. It’s almost always bought with a loan. Which means the asset is leverage.

But what does this have to do with returns you might ask?

Here’s an example (for simplicity we are ignoring buying and selling costs and tax):

Property 1 is brought in 2016 for $500K with a 20% deposit of $100K. That same investor also buys $100K of shares in 2016 too.

Fast forward 1 year and the house is now worth $600K and the shares worth $150K

Let’s make it simple and say that the shares have no dividends and that the house had $0 net gain/loss factoring in everything.

The shares made a whopping 50% return in one year. The property on the other hand only made a 20% return.

Which investment did better?

Going percent wise the shares beat the pants of the house. More than doubled its return. But hold on.

If we actually compare how much money each investment made, it tells a different story.

It cost the investor both $100K to buy each asset. Property made a total of $100K in a year whereas the shares only made $50K.

This is because of the power of leverage. You technically can leverage with shares but not for the same cheap rate and you get nasty margin calls which you don’t get with property.

The ability to physically add value to your asset is where I would say active investors have a clear choice with which investment they choose.

Sweat equity is a proven wealth building technique that’s been around for centuries. You would have to be extremely unlucky to physically add value to your property and not have it go up in value.

Experience and skill is a very interesting point to look at when comparing shares and real state.

The entire premise of index-style investing goes something along the lines of:

“It’s impossible to beat the market over a long period of time unless your names Warren Buffett. Even if you do manage to do so, it’s almost always luck. People spend all day every day studying stocks and graphs and still get it wrong. So what hope do you have as an ordinary Joe Blow? Don’t even try to become a master of the stock market because there is only such a very very small percent of humans alive that seems to be able to get it right the majority of the time”

Now, here’s the difference. Skill and experience actually matter in real estate.

A skilled and experienced property investor has a very good chance of repeating his/her success over and over again. In fact, they most likely get better at it as times goes on. The same cannot be said for the stock market (except for those very rare people like Buffett). A skilled and experienced property investor will beat the pants off a skilled and experienced stock trader over a 7-10 year period 9 times out 10.

You can’t really be skillful in picking stocks. You definitely can’t be skillful in picking ETFs either. Sure, you can be smart about your allocations to reduce risk. But it’s not like an ETF investor of 30 years is going to blow out a brand new ETF investor in terms of returns. In fact, they should get relatively the same return. And that’s not a bad thing either.

Contestant 2: Shares

3 things.

Diversification

Low buy in and selling costs

Easy peasy with hardly any management required

Have you ever heard the phrase ‘don’t keep all your eggs in one basket’?

The stock market gives you the ability to buy things called ETFs which is a slice of a lot (>200) of companies bundled up into one very convenient share. So instead of buying 200 individual shares. You can just buy things like ETFs and you get that vast diversification in one transaction. Couldn’t be any easier.

And the good thing about the stock market is the low buy in and sell costs. I pay $20 for around $5K of ETFs. Times that by 40 and I would have paid $800 for $200K worth of shares.

Think about how much it would cost you to buy a unit for $200K. Probably around $10K if we use the 5% rule.

And then you would have to sell it for anywhere between 2-3%.

When you want to sell shares there is another brokerage cost of around $20 per sell (depending on how much you sell).

This low buy in and sell costs are very convenient when compared to real estate.

And the last point I want to make is also one of the most important points. How little of your time and effort you have to put in for it to make you money.

And check up on your shares after about 7-10 years and get a pleasant surprise that on average, they have increased by around 9%

They only thing required during these 7-10 years is declaring the income earned through dividends on your tax returns which you can download electronically. No need to keep your own records.

THAT’S IT.

You didn’t have to manage anything and your investments returned a respectable 9% over 7-10 years. This extremely low management style is a phenomenal advantage.

Pros and Cons

Property

Pros

Cons

Leverage on low-interest rate

Ability to physically add value to investment

Skill and experience can be leveraged

High return potential for an active investor

Tax advantages such as neg gearing, depreciation and PPOR capital gains exclusion

Good protection against inflation

Less volatile than other asset classes

Active investment.

Requires a lot of capital to get started

Big buy-in (5%) and exist (2-3%) costs

Not diversified. One asset class in one location

Loan stress

Potential for things to go wrong. Leaking pipes, dog pees on the carpet, house burns down etc.

Not very liquid. May take you 6-12 months to cash out of this investment

Cash flow dependent. Needs a big buffer for incidents

If something goes horribly wrong. It can ruin you financially

Shares (ETFs)

Pros

Cons

Passive investment. Very little time and effort involved (less than one day a year)

Extremely diversified

Low entry and exit fees

Very liquid. Can break up shares and sell only a few units if that’s what you need

Easy peasy to do a tax return. No bookkeeping required

Franked dividends

At worst you can only lose what you have invested

Can’t physically improve investment or add value to asset

No influence on how your investment performs. If the market is down there’s not much you can do

Can’t leverage at the same low-interest rate as property

If you do leverage (which I wouldn’t recommend), you may get margin calls

More volatile

Fewer tax advantages than property

So Which Ones Right For Me?

It all comes down to what type of investor you are. Are you an active or defensive (passive) investor?

‘The defensive investor is unwilling, or unable, to put in the time and effort required to be an enterprising investor. Instead of an active approach, the defensive investor seeks a portfolio that requires minimal effort, research, and monitoring.’

My rough guess is around 95% of people are passive investors.

That’s because the majority of everyday people don’t really care for finance in general and would rather be doing others things they find interesting.

But since you’re on this blog, it means you find finance stuff interesting. What a sad bunch we are ?!

If you’re a passive investor I think the answer is clear.

Shares are clearly suited for the passive investing style while still giving the investor a great return.

Coupled with great diversification, low buy-in and selling costs, no loan stress, liquid asset (can get your money out in 2-3 days), it makes for the ultimate passive style investment!

But if you’re in that very small group of investors that want to take an active approach, you’ve gotta ask yourself.

Are you REALLY an active investor? Do you REALLY want to manage your investments for potentially the next 10-15 years? Will your circumstances change? What happens if you have a few kids? Do you still want to be managing your investments on 4 hours sleep?

Do you have a lot of capital lying around for a deposit?

How’s your cash flow position? Could you afford to pay an extra $1,400 a month when you don’t have a tenant in?

Is your job stable?

Do you have a big cash buffer in case anything goes wrong?

If you answered yes to all the above then maybe you are suited for investing in property.

I have made money using both investment classes. They each have their own merits and downfalls.

Whichever one you choose to invest in, just make sure you educate yourself before taking the plunge.

If you’re on the path to financial independence and follow a few bloggers as they save and invest their way to freedom. You no doubt have come across an investment vehicle that just keeps on popping up everywhere you look.

Exchanged Traded Funds (ETFs)!

The holy grail of investing, according to most in this space. I’m more open to other types of investment classes such as real estate (I can almost hear the boos and hisses) and believe that each asset class has its strengths and weaknesses. But honestly, ETFs are recommended by so many people (Warren Buffett included) for very good reason:

Extremely low management costs (one of my ETFs charge 0.04%)

Great diversification

Low buy in and exit fees ($20 a pop depending on how much you buy/sell)

Can start investing with little capital (investment properties, on the other hand, require considerable start-up costs)

And there’s more but you get the idea.

So ETFs are awesome right! But how does one actually go about purchasing these little bundles of investment goodness?

Directly through Vanguard vsBuying ETFs

This is the most confusing part of the whole thing. So you decide that you want to buy Vanguard ETFs because you’ve been hearing how awesome they are so you naturally do what any computer literate person would do.

You go to Google.

You punch in Vanguard, head to their site expecting it to be awesome and have them basically walk you through buying their product.

Errrrrr not so fast muchacho’s!

Vanguard’s site is crap. Yes, it has all the information you need on there in the form of white papers. But they have absolutely no funnel for a user to purchase their product. You sorta have to figure it out on your own. And to be honest, Vanguard doesn’t really need to rely on a fancy website or app (they don’t even have an app ffs). Their product is so good they don’t waste time and money on advertising and marketing.

Back to the point. You have two choices when it comes to buying a Vanguard product. You can either buy it directly from them (called managed funds) or you can purchase an ETF through a broker.

In a nutshell:

ETFs

Good if you make large or irregular investments

Requires trading flexibility

Managed Funds

Good if you make ongoing, small contributions

Does not require trading flexibility

The biggest factor is probably cost. Because depending on how often you’re going to make contributions, will dictate which method is right for you. There is a really good article that goes into detail about the costings of investing directly through a mutual fund vs ETFs on the Betterment website.

I have never purchased Vanguard products directly from them because it works out better for me to buy ETFs, so I can’t comment. But I have seen videos and it’s basically a signup, get your details, pick your fund type deal. If you have experience please comment below.

I do have experience buying Vanguard products through a broker though (see the video below to see me literally buying some).

Buying ETFs Walkthrough

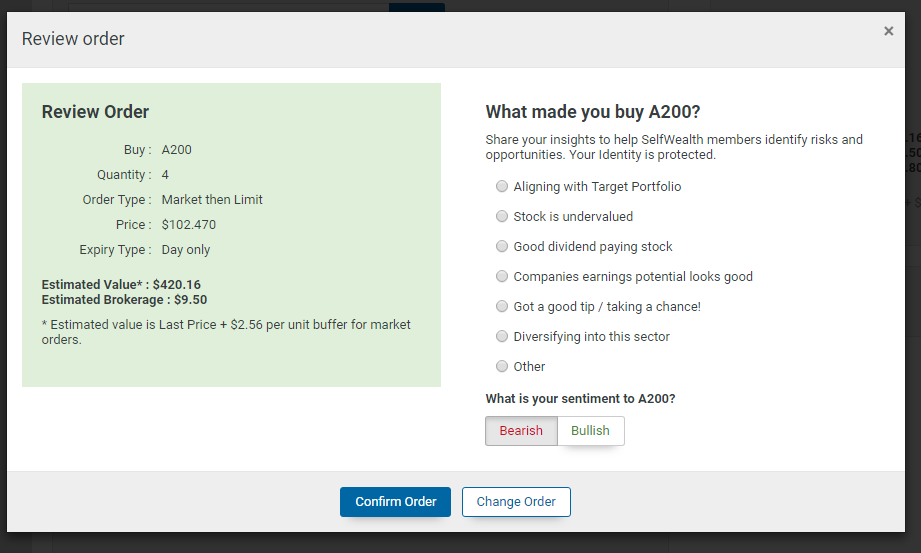

Log into your broker (I use SelfWealth) and head to trading > Place Orders

Select the ASX (Australian Stock Exchange) code that you want to purchase (a list of all Vanguard listed ETFs can be found here) or use the search function

Set order type as ‘Buy’

Enter in how many units you wish to purchase

Select at market value or list a price you’re happy with

Set an expiry for the transaction

Review your order and hit submit

Here’s an example of what mine looks like

It’s that simple. Proceed to the next screen and confirm the order and you’re done. It will take a few days to process and the money will then come out of your nominated account and boom. You have now bought some ETFs.

If you have any specific questions please let me know and I’ll answer them to the best of my abilities.

Now go forth and fear not the simple process of purchasing ETFs!

P2P lending is a topic I have been wanting to do for a long time but I never had the experience or expertise to write about it. I’m the kinda guy that actually likes to do something before I claim any knowledge on the subject. There are people out there believe it or not, that actually give seminars and speeches about how to become master in topic X without ever actually have been a expert in the first place.

Anyway, peer to peer (P2P) lending has been an interest topic of mine for about 2 years now. And when a reader emailed me with their experience with P2P lending I thought it would be a good opportunity for a guest post.

Chris has been investing in P2P lending platforms for over 2 years and he was kind enough to share his experience with us.

So without further adieu, here is the post. Enjoy 🙂

P2P Lending Guest Post

Several years into my FIRE journey I was seeking more diversification, more yield, and more interesting ways I could take control of my investments. Already I had delved into the share market, given managed funds a second chance (a story for another day). Then, one dark & stormy night, while searching across the digital internet on my electric computing device, I came across something called Peer-to-peer (P2P) lending.

Reddit and Whirlpool, where all the cool kids hang out, wasn’t much help in terms of details – just a few mentions here and there about UK company, RateSetter, entering the Australian market.

Magnets, How Do They Work?

I was able to discern that P2P lending, broadly, involves lenders/investors, being able to choose where their money is invested using online platforms. This is in contrast to a Real Estate Investment Trust, or index fund, where the investor’s money is managed by someone else. ASIC has a nice little write-up here (https://www.moneysmart.gov.au/investing/managed-funds/peer-to-peer-lending).

Each P2P provider does things in their own way, but it seems common across all platforms that these investments are very risky, often uninsured, unsecured, and can have a very delicious return.

At the time (December of 2015) the major players were RateSetter and SocietyOne.

SocietyOne is only open for the “sophisticated” investor – with a hefty minimum investment of $500,000, while RateSetter had a minimum

investment of $10… So, ugh, RateSetter it is!

My Experience With RateSetter

RateSetter operates both personal loans and business loans. Lenders elect what rate of return they want, what amount of money to lend at that rate, and for how long (1 month, 1 year, 3 years, 5 years). Then, they are matched to a borrower, who is seeking the lowest rate they can get. This makes the market a bit competitive as lenders undercut each other in order to get their money matched to a borrower.

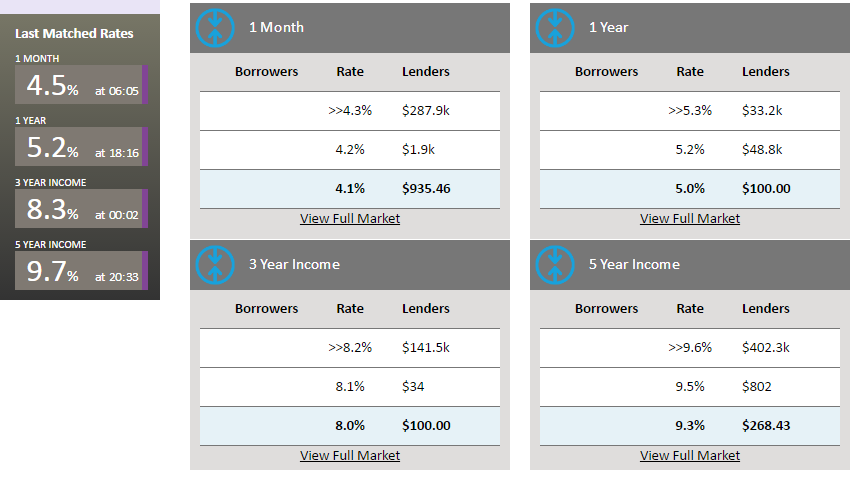

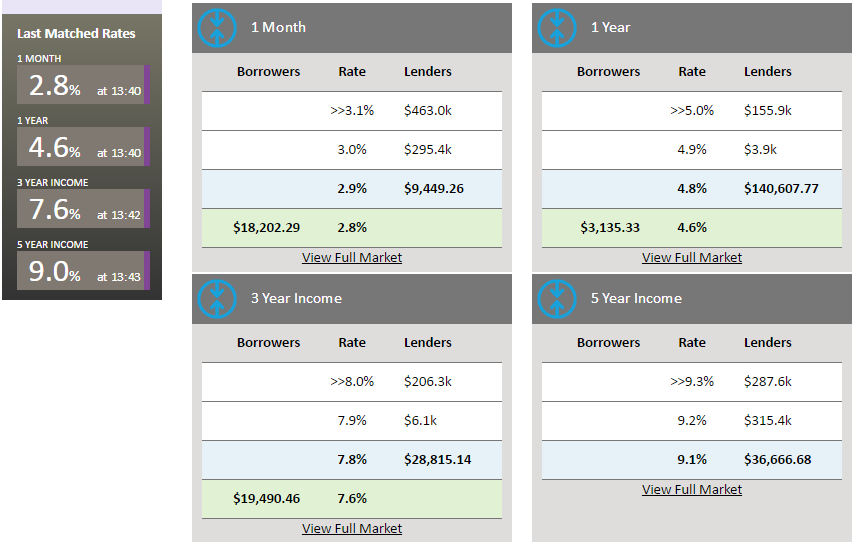

In this competitive market borrowers can snag rates better than what a bank would offer them, if the bank would lend to them at all. I’m going to paste in two screenshots now. The first is from December 16th 2016, and the second is from January 12th 2017. You can see how competition and demand can affect the rates over the course of just one month.

1 – December 16th 2016.

2 – January 12th 2017.

After assessing the PDS and reading about the risks involved, I decided that $5k was appropriate for me to start lending. I watched the 1-year market, selected a 5.9% rate (which was slightly above the last match) and I got matched in a few days.

This turned out to be a good rate, as competition pushed the rates down a full 1% a few months later.

Given the Peer-to-peer nature of the platform, I was expecting a little more involvement on my behalf in the matching process, and later I’ll discuss MarketLend which has exactly the level of control I was expecting. Then again, I can see how some people might prefer the ease of RateSetter’s automatic matching.

The 1-month and 1-year markets in RateSetter are structured very straight forward. Your returns are paid once per month at the rate you were matched and at the end you get your principal back.

In the 3-year and 5-year markets, however, both the interest and part of your principal are returned each month.

None of RateSetter’s loans are secured but there is a “provisional fund” from which they can compensate lenders for losses at their own discretion. Information on how often this happens is hard to come by (my Google-fu failed me).

Over the course of the investment, here are my interest payments:

Jan/2016

26.73

Feb/2016

23.49

Mar/2016

23.49

Apr/2016

26.73

May/2016

22.68

Jun/2016

25.11

Jul/2016

25.92

Aug/2016

23.49

Sep/2016

25.11

Oct/2016

25.11

Nov/2016

24.30

Dec/2016

23.49

So… what to do now that’s finished?

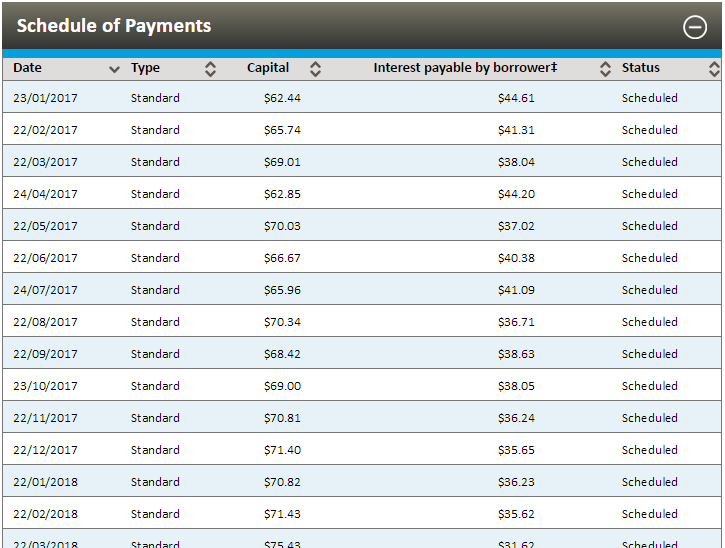

Well, I delved straight back in again and got matched in the 5-year market at 9.5% 🙂

And RateSetter provide a nice little schedule of payments for the life of the investment.

As you can see, this time, in the 5-year market, a portion of my principal (“Capital” column) will be returned each month, and my interest earned is reduced accordingly.

When these payments start rolling in, I will give the “auto-bid” feature a crack. With the auto-bid, payments made to your holding account can automatically be reinvested in the market and rate you specify – either a set rate, or the current market rate. Very handy!

My Experience With MarketLend

My good experience with Ratesetter made me a little braver when I decided to try out MarketLend. I threw $10k at it in August 2016 and payments started in September.

This is a platform which focuses on business loans.

Some loans are insured, some are uninsured. Some loans are for supply chain financing – where MarketLend will own the supplies – and some are simply a line of credit. One of the more interesting loans I’ve seen was for a short-term money lender. I was an investor, lending money to a business to lend money to a business to lend money to people… Hold on while I go watch “Inception” again….

MarketLend advertises these loans to investors in the form of units, each valued at $100. I.e. if i want to lend $1000, I would bid on 10 units at the rate I want. At any time another investor can undercut my bids, introducing a competitive element here as well.

Those high percentages might look amazing but hold on… because I should tell you about utilised versus unutilised parts of the loans – which will affect your return.

In these loans, the borrower might not access all of the capital which is on loan. The money which HAS been accessed, is the “utilised” amount. The rest is “unutilised”. This is important because your return (of say 18%) only applies to the utilised amount. So, even though you might be lending out your money at an amazing 18%, your gross return will be much less. Then MarketLend takes out their fee and your pre-tax return might be %8 (this is my actual average return so far across all my units).

Borrowers could also back the loan early. In which case you get your principal back early, the loan ends, and you are free to carry on your merry way – maybe withdraw the money, maybe invest in more units.

What I really like about MarketLend, is that credit checks and financial statements from the borrowers are available, so you can get very acquainted with them before deciding to bid.

This is the level of control and information I was looking for in a Peer-to-peer lending platform.

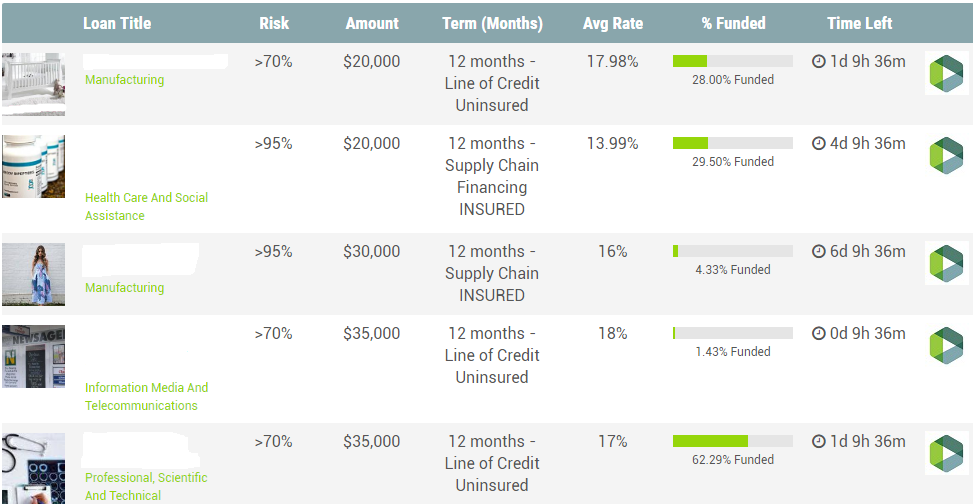

In the interest of diversification, I spread my $10k around many different borrowers at many different rates and levels of risk. Here’s a sample:

And here’s my returns so far:

Month

Amt

Real Return

Sep/2016

34.60

4.15%

Oct/2016

74.87

8.98%

Nov/2016

81.55

9.69%

Dec/2016

76.56

9.10%

Jan/2017

83.53

9.83%

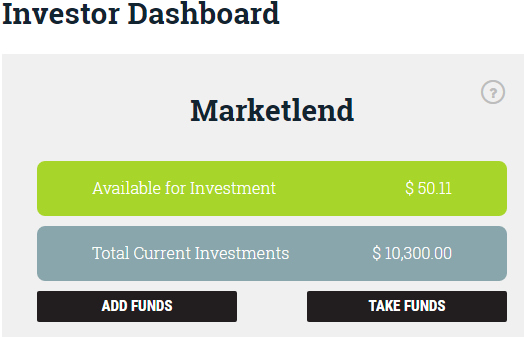

I have used my returns to buy additional units, so I currently have $10,300 invested.

Finally, MarketLend features a secondary market where lenders can sell off their units to other lenders. This is useful if you no longer wish to carry the investment, or just need some liquidity.

I’ve picked up a few discounted units here – it’s definitely worth a look if you decide to go down this path.

Conclusions

P2P lending is cool. It’s high yield. And comes with high risk (so read those PDSs).

I like how MarketLend lets me choose who to lend to and the ability to make an informed decision – but RateSetter is also nice so I will continue to use both.

Ratesetter

MarketLend

Pros’s

Website looks and feels more professional.

Predictable returns.

Provisional fund may reduce risk of loss.

More information and more control and over lending.

Easier to diversify investments.

Secondary market allows selling/buying units.

Australian owned & operated.

Con’s

Little control over matching process.

Did not notify me when my investment ended.

The queue-like structure delays matching.

Utilised/unutilised was confusing at first.

No Bpay facility.

Did not notify me when one of my investments was repaid early.

What’s Next?

Another P2P platform caught my eye recently; Brickx. These guys break down a house mortgage into 10,000 units, which investors can bid on, buy, and trade with each other.

Returns come from cash-positive rental income, or capital gains in a sale. I have a bit of saving to do, and a couple of impending financial commitments to get past, before I’m ready, though.

For now, my P2P returns will continue to be reinvested. Due to the nature of the investment, I should expect some losses over time, as borrowers default or make late payments, but that’s why we manage our risk.

-Chris

Wow, what a quality insight into the world of P2P lending. I would like to thank Chris again for putting that amazing post together. If you have any questions about it please feel free to comment on this article. Chris has agreed to answer your questions in the comment section below.

As 2016 comes to an end I’d like to reflect back on what was achieved and set new goals for the coming year.

I’m a big believer in setting goals and making deadlines for them.

One of my favourite quotes:

I really like it because everyone has dreams, but very few actually put in the work required to realise those dreams. Too many people (myself included) think of doing something great but it just never happens because you don’t put any pressure on yourself and rely purely on motivation.

Motivation only lasts so long and when it runs out you should be relying on habit/routine to get the job done. “I’m just not motivated today” is the wrong attitude. Everyone starts the project with motivation, but it’s the habits formed that will see the project completed.

It’s so important to actually map out a plan of attack for your dream no matter how small it is and say to yourself:

“I’m going to have X done by this time next week/month/year”

And then break the task up into smaller sub tasks if it’s a big project. But make sure you set a time and date that you want it completed by or else it will get pushed to the side every time.

I have a rule with this blog that I MUST write a minimum of two posts per month no matter what! No excuses!

This has led to me publishing a new post at 11:30PM once with work on the next day. That’s the price I pay for not being more organised.

What Did I Achieve In 2016?

2016 was a huge year for me personally and financially.

I

Moved into a share house

Watched as the RBA cut the cash rate twice to 1.5%

Watched Malcolm Turnbull and the Liberal party get elected

Had 2 properties gain and one lose value over the course of the year

Joined financial forces with my partner

Bought around $50K worth of ETFs

Moved in with my partner

Broke into the $200K net worth club (so close to the $250K damit!)

I originally wanted to buy another investment property and dip my toes into ETFs for 2016. But the more I thought about it, the more I was leaning towards ETFS.

2017 Financial Goals

My big financial goals that I want to achieve by the end of the year are

Obtain a savings rate of 65% or better

Reach $100K in ETFs

They are both very measurable goals and are something I can review monthly to track how I’m going.

My big goals for the blog are:

Try to release a podcast every month. It’s the number one thing I get requests for. I love doing them too I just find it hard to find guests

Revamp the home page

Write more about Super

What Are Your Goals?

What do you hope to achieve financially on your way towards FIRE in 2017?

Australian FIRE Calculator

Get FREE Aussie Firebug updates, tips and tricks, and exclusive content!

No spam. Unsubscribe anytime.

Stay Connected!

Join others who get FREE Aussie Firebug updates, tips and tricks, and exclusive content!