All three strategies have their merits but they all require rebalancing with the exception of an all Australian ETF. The issue with that strategy is, of course, you don’t have much diversification as Australia is only roughly 2 percent of the world economy. And with how much private debt Australians have right now… if Australia went through a recession the all Australian portfolio would not fare well.

The point is that each one of these strategies is missing something and require manual intervention whether it be rebalancing, extra admin work or more diversification.

Wouldn’t it be good if there was an ETF that took care of all this for you?

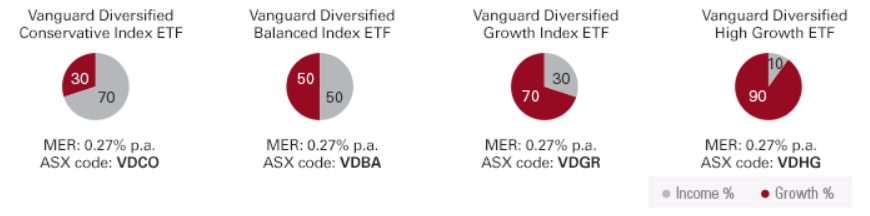

Vanguard Diversified ETFs

So what are they exactly and what’s the difference between buying this ETF vs one of the three options mentions above?

To put it simply, any of the four diversified index ETFs above offer a complete one stop shop solution for anyone looking to invest.

They solve a few problems that our three options above had

Diversification – Exposure to over 10,000 securities—in just one ETF.

Auto Rebalancing

DRP option

Hedged against the Australian dollar*

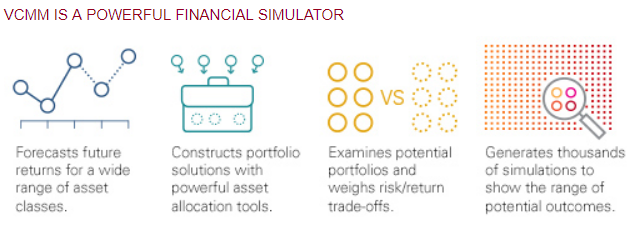

It wasn’t listed above as a con, but all four diversified index ETFs are actively managed using Vanguard Capital Markets Model (VCMM)

The two big ones that stand out are of course the auto-rebalancing but also maybe surprisingly the active management component.

Rebalancing is not hard to do, but it’s something that if left unattended can most certainly affect the performance of your portfolio over the long term. As for the active management component. You may be wondering why there is any management at all? I thought Vanguard is all about minimal management to keep fees low and it’s really hard to beat the index anyway??? I’m not sure about this part beating the market either but I guess we will have to wait and see how it performs. It uses a modelling system called VCMM to simulate potential outcomes and pick the correct balance for your desired portfolio out of the four options above.

*As pointed out by Chris in the comments. The diversified ETFs are not 100% hedged. Please check the PDS for each ETF to find the amount of hedging

Who Is This Suited For?

To be honest, it’s a bloody good product for 99% of people. What they are offering here is as close to the perfect ETF as I’ve ever seen given the management fees and what it offers.

The best thing about this ETF is how idiot-proof it is. A complete n00b could buy one of the four diversified ETFs (depending on their investor profile) for the rest of their life and get respectable returns with minimal effort.

People avoid things that appear confusing and hard. That’s why Robo investment companies like Acorns and Stockspot are in business. They essentially are providing what this ETF is providing at additional costs because they make investing super easy and friendly. With the other three options listed above, it can be daunting to explain to a complete n00b how to rebalance. As soon as they don’t understand something, the majority of the time they can get spooked and give up altogether.

That’s why this ETF is so special. You can confidently recommend this product to anyone and be sure that they can’t stuff it up or get confused.

Set up a broker account

Buy this ETF when you have the money to do so

Turn on DRP if you want

Do tax when it comes around

Repeat forever

So if this ETF is suited for 99% of people, who is the 1%?

Why I Won’t Be Switching To These ETFs

This is something I have been wanting to bring up for a while now.

Has the Australian FIRE community forgotten just how important management fees are?

I have been seeing a lot of people recommend VDHG, which as I have mentioned above is a fantastic product. No doubt about it.

The only issue I have is that at a MER of 0.27%, it’s more than double that of what my MER currently is (0.101% or option 2 above). They are both very low fees, but I plan to have a portfolio of a million+ within the next 5 years and hope to live for another 50 years at least! Now even though the management fees are very low, over a long period of time it does add up!

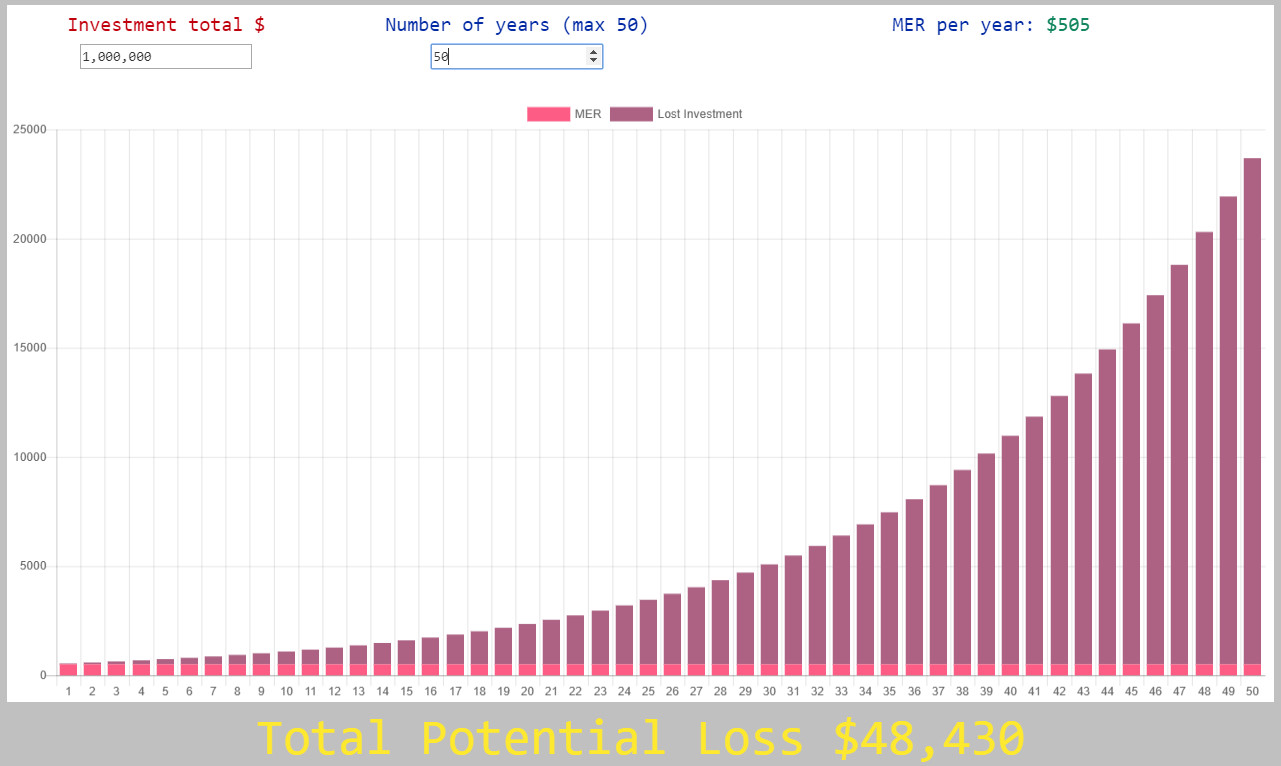

I have actually been working on a web app recently (so close to being published) that works out lost investment potential from management fees which gives you a visual of what I’m talking about.

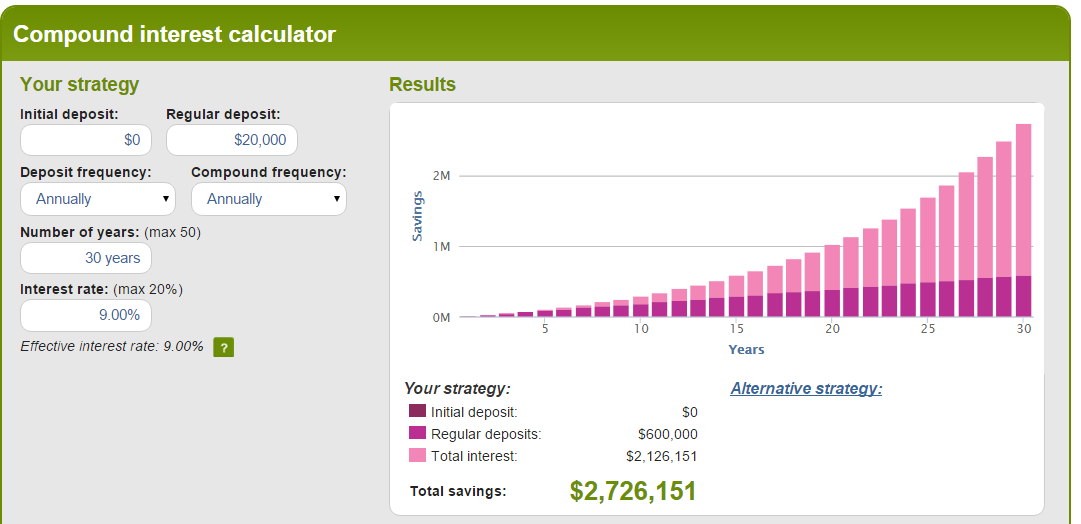

Management fees are unavoidable, but how much you pay is your choice to an extent. I have calculated my current investment potential loss from management fees to be $48K over 50 years at $1M invested.

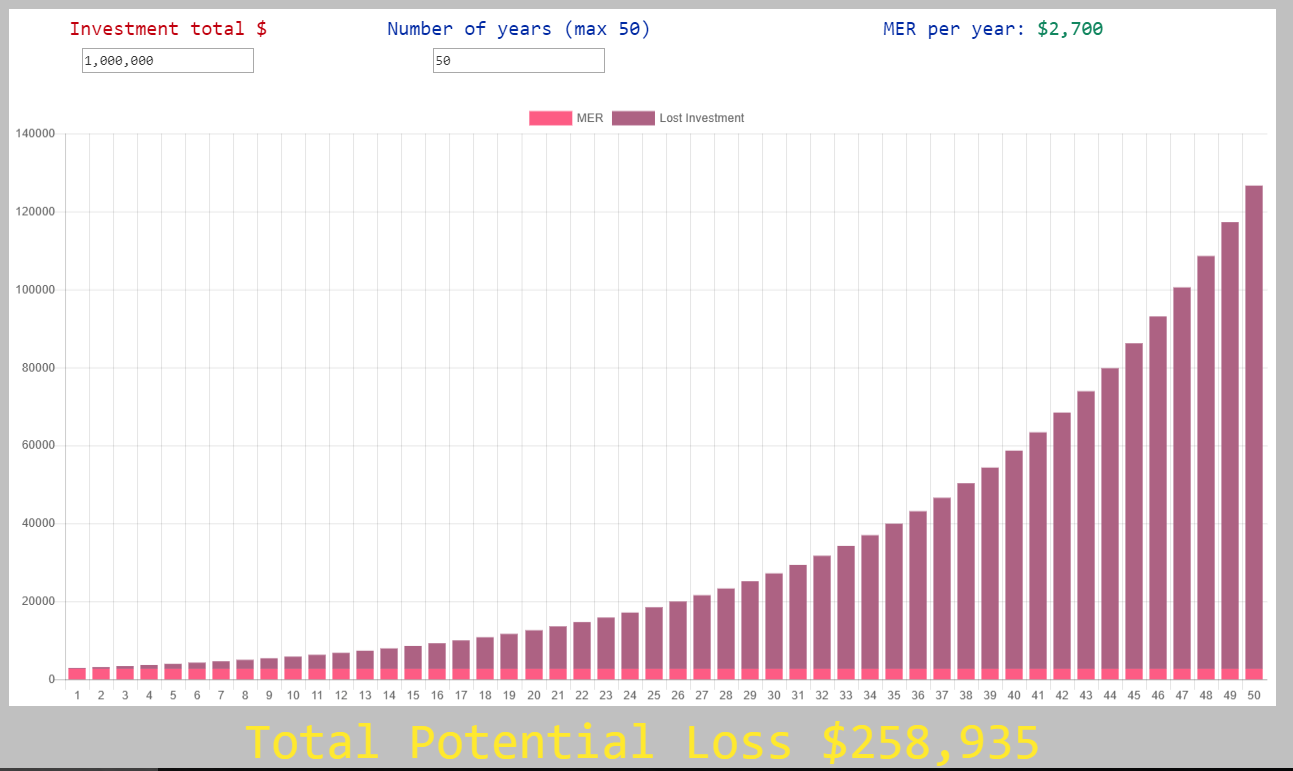

If I change the management fees to be 0.27% we get the following

Holy shit!

We went from paying under $50K over 50 years in investment potential loss from management fees to over 5 times that amount at over $250K!

Ok, I need to clear a few things up about the above graphs because it’s a big deal.

What am I actually talking about when I say investment potential loss? I’m referring to how much management fees are costing the investor when you factor in that the money paid to management could have been invested and compounded at 8% return (that’s what the graph is using as a return rate).

If I had $1M in my portfolio with my current weightings I would be paying Vanguard $505 a year. If I had $1M with any of the diversified index ETFs, I would be paying Vanguard $2,700 a year.

The difference between $505 and $2,700 a year over a lifetime adds up!

Conclusion

If you’re reading this blog, odds are you’re somewhat interested in personal finance and investing. The question you need to ask yourself is whether or not you are willing to learn, educate yourself and do the extra things required for the lower MER ETF options. Or if you think that the higher MER for the diversified index ETFs are justified. I personally choose to keep my MER as low as possible because paying less in management fees is a guaranteed return. You could argue that the diversified index ETFs will outperform my ETF combo but that is unknown without a crystal ball.

If you don’t know what half of the words in this article are even about, then the diversified index ETFs are most likely the best ETF for you. Just pick your investor profile and off you go. And don’t sweat the extra management fees. If the simplicity of the diversified ETF gets you into investing, you’ve more than made up the difference.

Preface: When I talk about shares in this article, I really mean ETFs. I don’t buy individual shares or day trade.

Collingwood vs Carlton

Sydney vs Melbourne

Magic vs Bird

Just some of the biggest rivalries the world’s ever seen.

But in the investing world, there is not a more hotly debated topic among avid investors. Property vs shares is a topic that everyone seems to have an opinion on, no matter how ill-informed they are.

Owning 3 investment properties and nearly $90K worth of ETFs (shares), I feel I have tasted the best of both worlds (and the worst) and can give you perspective to what I’ve learned over the last 5+ years of investing in these two asset classes. Both are great when used right, with pros and cons for various financial situations/types of investors.

But which one is right for you?…

Contestant 1: Property

The hometown favorite. This guy has been around longer than the stock market has existed!

You can touch and feel him, and your mum most likely loves the idea of you being with him. He has a strong track record in Australia and there is a firm belief that his value never goes down.

Now for realz:

Property is a great investment class but you need to be the right type of investor and have the financial stability for it to be used correctly. It’s an active investment. You’re going to have to do some sort of work to keep this investment running. You can minimize the work needed by hiring people but there are still headaches trust me.

However! Property has BY FAR the most potential to accelerate your wealth compared to shares for three reasons.

Cheap leverage

Ability to physically add value to your asset

Skill and experience actually mean something (more on this below)

Cheap leverage is often misunderstood. Too often an article is published with statistics on how shares have outperformed property by comparing the % of capital growth and rental/dividend returns.

This is a dumb way to compare the two because I don’t know any property investors that buy real estate outright. It’s almost always bought with a loan. Which means the asset is leverage.

But what does this have to do with returns you might ask?

Here’s an example (for simplicity we are ignoring buying and selling costs and tax):

Property 1 is brought in 2016 for $500K with a 20% deposit of $100K. That same investor also buys $100K of shares in 2016 too.

Fast forward 1 year and the house is now worth $600K and the shares worth $150K

Let’s make it simple and say that the shares have no dividends and that the house had $0 net gain/loss factoring in everything.

The shares made a whopping 50% return in one year. The property on the other hand only made a 20% return.

Which investment did better?

Going percent wise the shares beat the pants of the house. More than doubled its return. But hold on.

If we actually compare how much money each investment made, it tells a different story.

It cost the investor both $100K to buy each asset. Property made a total of $100K in a year whereas the shares only made $50K.

This is because of the power of leverage. You technically can leverage with shares but not for the same cheap rate and you get nasty margin calls which you don’t get with property.

The ability to physically add value to your asset is where I would say active investors have a clear choice with which investment they choose.

Sweat equity is a proven wealth building technique that’s been around for centuries. You would have to be extremely unlucky to physically add value to your property and not have it go up in value.

Experience and skill is a very interesting point to look at when comparing shares and real state.

The entire premise of index-style investing goes something along the lines of:

“It’s impossible to beat the market over a long period of time unless your names Warren Buffett. Even if you do manage to do so, it’s almost always luck. People spend all day every day studying stocks and graphs and still get it wrong. So what hope do you have as an ordinary Joe Blow? Don’t even try to become a master of the stock market because there is only such a very very small percent of humans alive that seems to be able to get it right the majority of the time”

Now, here’s the difference. Skill and experience actually matter in real estate.

A skilled and experienced property investor has a very good chance of repeating his/her success over and over again. In fact, they most likely get better at it as times goes on. The same cannot be said for the stock market (except for those very rare people like Buffett). A skilled and experienced property investor will beat the pants off a skilled and experienced stock trader over a 7-10 year period 9 times out 10.

You can’t really be skillful in picking stocks. You definitely can’t be skillful in picking ETFs either. Sure, you can be smart about your allocations to reduce risk. But it’s not like an ETF investor of 30 years is going to blow out a brand new ETF investor in terms of returns. In fact, they should get relatively the same return. And that’s not a bad thing either.

Contestant 2: Shares

3 things.

Diversification

Low buy in and selling costs

Easy peasy with hardly any management required

Have you ever heard the phrase ‘don’t keep all your eggs in one basket’?

The stock market gives you the ability to buy things called ETFs which is a slice of a lot (>200) of companies bundled up into one very convenient share. So instead of buying 200 individual shares. You can just buy things like ETFs and you get that vast diversification in one transaction. Couldn’t be any easier.

And the good thing about the stock market is the low buy in and sell costs. I pay $20 for around $5K of ETFs. Times that by 40 and I would have paid $800 for $200K worth of shares.

Think about how much it would cost you to buy a unit for $200K. Probably around $10K if we use the 5% rule.

And then you would have to sell it for anywhere between 2-3%.

When you want to sell shares there is another brokerage cost of around $20 per sell (depending on how much you sell).

This low buy in and sell costs are very convenient when compared to real estate.

And the last point I want to make is also one of the most important points. How little of your time and effort you have to put in for it to make you money.

And check up on your shares after about 7-10 years and get a pleasant surprise that on average, they have increased by around 9%

They only thing required during these 7-10 years is declaring the income earned through dividends on your tax returns which you can download electronically. No need to keep your own records.

THAT’S IT.

You didn’t have to manage anything and your investments returned a respectable 9% over 7-10 years. This extremely low management style is a phenomenal advantage.

Pros and Cons

Property

Pros

Cons

Leverage on low-interest rate

Ability to physically add value to investment

Skill and experience can be leveraged

High return potential for an active investor

Tax advantages such as neg gearing, depreciation and PPOR capital gains exclusion

Good protection against inflation

Less volatile than other asset classes

Active investment.

Requires a lot of capital to get started

Big buy-in (5%) and exist (2-3%) costs

Not diversified. One asset class in one location

Loan stress

Potential for things to go wrong. Leaking pipes, dog pees on the carpet, house burns down etc.

Not very liquid. May take you 6-12 months to cash out of this investment

Cash flow dependent. Needs a big buffer for incidents

If something goes horribly wrong. It can ruin you financially

Shares (ETFs)

Pros

Cons

Passive investment. Very little time and effort involved (less than one day a year)

Extremely diversified

Low entry and exit fees

Very liquid. Can break up shares and sell only a few units if that’s what you need

Easy peasy to do a tax return. No bookkeeping required

Franked dividends

At worst you can only lose what you have invested

Can’t physically improve investment or add value to asset

No influence on how your investment performs. If the market is down there’s not much you can do

Can’t leverage at the same low-interest rate as property

If you do leverage (which I wouldn’t recommend), you may get margin calls

More volatile

Fewer tax advantages than property

So Which Ones Right For Me?

It all comes down to what type of investor you are. Are you an active or defensive (passive) investor?

‘The defensive investor is unwilling, or unable, to put in the time and effort required to be an enterprising investor. Instead of an active approach, the defensive investor seeks a portfolio that requires minimal effort, research, and monitoring.’

My rough guess is around 95% of people are passive investors.

That’s because the majority of everyday people don’t really care for finance in general and would rather be doing others things they find interesting.

But since you’re on this blog, it means you find finance stuff interesting. What a sad bunch we are ?!

If you’re a passive investor I think the answer is clear.

Shares are clearly suited for the passive investing style while still giving the investor a great return.

Coupled with great diversification, low buy-in and selling costs, no loan stress, liquid asset (can get your money out in 2-3 days), it makes for the ultimate passive style investment!

But if you’re in that very small group of investors that want to take an active approach, you’ve gotta ask yourself.

Are you REALLY an active investor? Do you REALLY want to manage your investments for potentially the next 10-15 years? Will your circumstances change? What happens if you have a few kids? Do you still want to be managing your investments on 4 hours sleep?

Do you have a lot of capital lying around for a deposit?

How’s your cash flow position? Could you afford to pay an extra $1,400 a month when you don’t have a tenant in?

Is your job stable?

Do you have a big cash buffer in case anything goes wrong?

If you answered yes to all the above then maybe you are suited for investing in property.

I have made money using both investment classes. They each have their own merits and downfalls.

Whichever one you choose to invest in, just make sure you educate yourself before taking the plunge.

If you’re on the path to financial independence and follow a few bloggers as they save and invest their way to freedom. You no doubt have come across an investment vehicle that just keeps on popping up everywhere you look.

Exchanged Traded Funds (ETFs)!

The holy grail of investing, according to most in this space. I’m more open to other types of investment classes such as real estate (I can almost hear the boos and hisses) and believe that each asset class has its strengths and weaknesses. But honestly, ETFs are recommended by so many people (Warren Buffett included) for very good reason:

Extremely low management costs (one of my ETFs charge 0.04%)

Great diversification

Low buy in and exit fees ($20 a pop depending on how much you buy/sell)

Can start investing with little capital (investment properties, on the other hand, require considerable start-up costs)

And there’s more but you get the idea.

So ETFs are awesome right! But how does one actually go about purchasing these little bundles of investment goodness?

Directly through Vanguard vsBuying ETFs

This is the most confusing part of the whole thing. So you decide that you want to buy Vanguard ETFs because you’ve been hearing how awesome they are so you naturally do what any computer literate person would do.

You go to Google.

You punch in Vanguard, head to their site expecting it to be awesome and have them basically walk you through buying their product.

Errrrrr not so fast muchacho’s!

Vanguard’s site is crap. Yes, it has all the information you need on there in the form of white papers. But they have absolutely no funnel for a user to purchase their product. You sorta have to figure it out on your own. And to be honest, Vanguard doesn’t really need to rely on a fancy website or app (they don’t even have an app ffs). Their product is so good they don’t waste time and money on advertising and marketing.

Back to the point. You have two choices when it comes to buying a Vanguard product. You can either buy it directly from them (called managed funds) or you can purchase an ETF through a broker.

In a nutshell:

ETFs

Good if you make large or irregular investments

Requires trading flexibility

Managed Funds

Good if you make ongoing, small contributions

Does not require trading flexibility

The biggest factor is probably cost. Because depending on how often you’re going to make contributions, will dictate which method is right for you. There is a really good article that goes into detail about the costings of investing directly through a mutual fund vs ETFs on the Betterment website.

I have never purchased Vanguard products directly from them because it works out better for me to buy ETFs, so I can’t comment. But I have seen videos and it’s basically a signup, get your details, pick your fund type deal. If you have experience please comment below.

I do have experience buying Vanguard products through a broker though (see the video below to see me literally buying some).

Buying ETFs Walkthrough

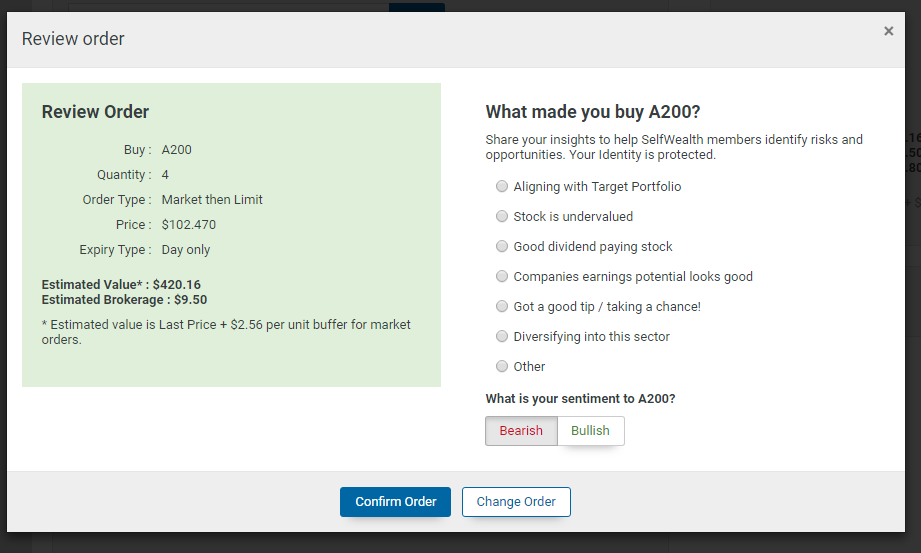

Log into your broker (I use SelfWealth) and head to trading > Place Orders

Select the ASX (Australian Stock Exchange) code that you want to purchase (a list of all Vanguard listed ETFs can be found here) or use the search function

Set order type as ‘Buy’

Enter in how many units you wish to purchase

Select at market value or list a price you’re happy with

Set an expiry for the transaction

Review your order and hit submit

Here’s an example of what mine looks like

It’s that simple. Proceed to the next screen and confirm the order and you’re done. It will take a few days to process and the money will then come out of your nominated account and boom. You have now bought some ETFs.

If you have any specific questions please let me know and I’ll answer them to the best of my abilities.

Now go forth and fear not the simple process of purchasing ETFs!

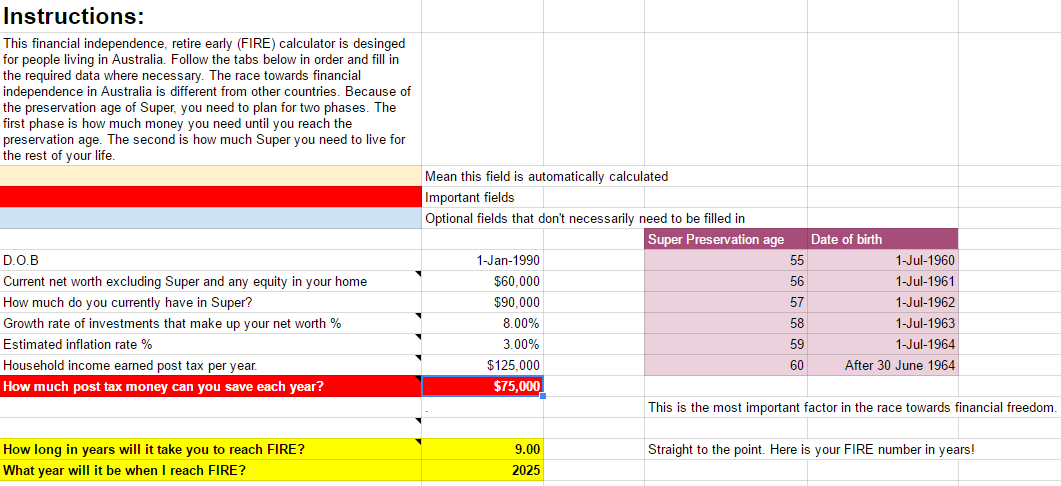

There are countless sites/articles/forums about financial independence (FI) on the world wide web. I’ve often come across really clever, well developed calculators that offer a really good visualisation on how long you have to go before you reach FI. But the longer I searched for the best calculator the longer I realised that they were all geared towards other countries.

One of the main reasons I created this site was to offer my fellow countrymen quality information that was tailored for an Australian audience.

The biggest issue I had with every single one of these FIRE calculators out there was they didn’t factor in our Super system. The US system, which is the main system upon which I found almost all of the calculators accounted for, has a fundamentally different way their citizens can withdraw from their retirement accounts.

To put it simply, in the US you only need one portfolio to be at a certain amount before you are considered FI. But because you can’t access your Super before your preservation age (99% of the time) you end up with two. Your Super portfolio and a portfolio outside of it.

So what’s one to do? Do I just keep plugging away at my personal portfolio until I reach my FI number? That seems like a waste since Super has such a big tax advantage. You’re not likely to beat the 15% tax breaks on your Super.

But I don’t want to put money into Super because I want to retire young! And I won’t be able to touch the money until my preservation age (60 for me).

Decisions decisions decisions!

Introducing The Australian Financial Independence Calculator

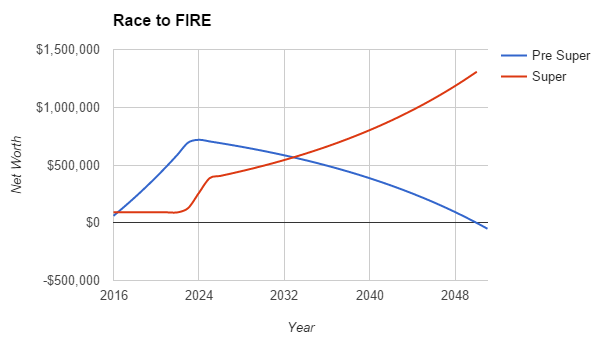

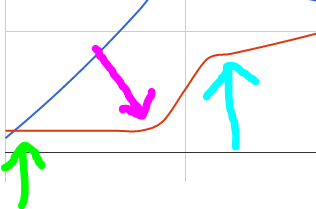

The above are two screen shots from the calculator showing the basic settings and the graph that it generates.

You will notice there are two lines in the graph. The Pre Super number is what you will be living off until you can access your Super. The Super number is obviously what’s in your Super.

In a nutshell, the most optimal way to reach FIRE here in Australia is to:

Step 1. Have enough money to survive until your preservation age (when you can access Super). No matter how much you have in your Super, you won’t be able to retire early and pursue your other goals in life if you don’t have money coming in to live off. Step 1 is not meant to last you forever though. It’s only meant to last you until when you hit your preservation age and can then access your Super. You will notice in the above graph that your Pre Super number goes up and up and up…and then slowly tapers off past $0. This is by design. You want your Pre Super number to be at $0 when you access your Super.

Step 2. Have enough in Super to cover all your living expenses forever! You will notice that the red line (Super) has a number of dips.

The green part of the line indicates how much Super you currently have at the start. This will move slowly up (depending on how much Super you have) over the years as your super grows from compounding interest until you hit the pink arrow.

The pink arrow indicates the time you have reached your Pre Super number. When you have reached your Pre Super number you theoretically should be able to live entirely off that number until preservation age (assuming all conditions stay the same). This means that 100% of your after tax income will be going into your Super account until you reach your Super Number.

Your Super number is not actually your FI number. Your FI number will be reach in your Super account at the very start of your preservation year. But no sooner than that, because that is the most efficient and fastest way to reach FIRE. The calculator works out how many years it’s going to take you to reach your Pre Super number and then does some cool math and works out that you need a certain amount in your Super for it to grow into your FI number the year you can access it.

Pretty cool huh!

Video Of The Calculator In Action

Work In Progress

The calculator has some flaws. It’s a work in progress. If you find a flaw please let me know and I’ll try to fix it.

Download Now

Enter your email address and not only will I send you the calculator. I will send you updated revisions of it ever time I fix a bug or the laws in Australia change.

What a horrible mash-up of words. Rentvesting? Rent-Investing? Rentvestor?

Yuck!

While the term itself doesn’t sit well with me, the underlying principles definitely do and I think a ton of millennials could benefit from it, so listen up muchacho’s!

What The Hell Is Rentvesting?

Put simply ‘rent where you want to live, while you invest where it makes sense’

Enter death blissfully knowing your financial situation will not follow you to the afterlife

I kid I kid.

But the point I’m trying to make is that the old school conventional way of buying a house in our two biggest cities doesn’t work anymore for the majority of people without financial help from their parents or inheritance.

This is because the game has changed! It ain’t what it used to be when ma and pop were hunting for a house.

Can Rentvesting Help?

Absolutely!

As I have already explained with my Rent vs Buy article, renting is cheaper 90% of the time.

And if you live in either inner Melbourne or Sydney, this becomes 110% of the time.

So instead of taking on a mortgage in either of these two cities, why don’t you rent for a few years and invest where it makes sense to do so.

Rentvesting can get you into the housing market without the financial stress when buying in inner Melbourne and Sydney.

How Does It Work?

One rentvesting example might be ‘Harry Hipster’ from inner city Melbourne complaining that the housing market is rising faster than he can save for a deposit.

Harry desperately wants to enter the property market but cannot save enough for the deposit and is unsure if he will be able to make mortgage repayments without at least a 20% deposit. Caution Harry is also extremely hesitant about the Melbourne market being in a bubble and is worried that prices could come crashing down just after he has bought.

He has been very cautious of a potential crash for more than a decade now and year after year he has seen friends and family around him buy real estate and increase their wealth. He’s sick of being on the sidelines but can’t afford to buy in inner Melbourne.

Harry discovers rentvesting and decides to take his savings and invest interstate where the property market is more affordable. The collected rent would cover the majority of costs associated with the investment with plenty of upside for capital growth.

Rentvesting has allowed Harry to get into the property market without the mortgage stress he would have had if he had bought in inner Melbourne. Furthermore, if Harry’s financial situation changes he can adapt quickly.

If Harry gets a raise, he can move into someplace more luxurious. Maybe he loses his job? No worries, he can move somewhere more affordable until he finds his feet again. None of these luxuries can be had once you lock yourself into a mortgage that you’re paying for. The investment property is an asset, not a liability. The mortgage on the IP is not paid for by Harry, he has tenants that are paying that loan off for him.

After a few years, Harry may decide to sell the IP getting back his savings plus whatever capital growth occurred during the years and use this money as a down payment for an inner Melbourne house. The entire time, Harry was in the property market and benefiting from whatever gains occurred instead of missing out on the sidelines. Harry was also not under financial stress and had the flexibility to live wherever he wanted to based on the circumstances he was in that year.

PROS

CONS

No mortgage stress

You won’t be paying off your home to live in. There is a psychological connection to be paying off something that’s yours. Renting can feel like dead money

Ability to save and invest more

No security in renting. Can get kicked out anytime

Exposure to the property market sooner

Rentvesting is for the disciplined! A mortgage can act as a forced savings mechanism. Rentvesting relies on you having the discipline to stick to a budget and not blow the extra cash.

Flexibility to change your biggest expense (living costs) when it suits you.

Start building your wealth now not later

Invest on your terms. 9/10 the place you want to live in is not the best investment. Rentvesting allows you to live where you want and invest where it makes sense.

Frees up cash flow for more smashed avocado on toast ??

Conclusion

With the two biggest cities in Australia being more expensive than ever, more and more Australians are struggling to get their foot into the property market. Rentvesting can be used to get into the market without having the stress of paying a mortgage yourself.

Rent where you want to live, invest where it makes sense.

My partner and I are rentvestors and have no plans to buy a house to live in anytime soon. This gives us the flexibility and freedom that we want this time in our lives. When circumstances change, we have the flexibility to adapt.

Are you currently rentvesting? Why? Why not?

Thoughts and feelings in the comment section below.

“Are you still renting? Why don’t you buy yourself a house already. Rent money is DEAD MONEY!”

If you rent, I’m sure you have come across one of these people at least once in your life. And it’s most likely coming from a loved one who genuinely cares about you. It’s easy to understand how they come to this conclusion too. At the end of every month you have to fork over hundreds (sometimes thousands) of your hard earned dollars for nothing more than the privilege of having a roof over your head. If you were to buy a house however, at least your payments are going towards something you can call your own. That’s the common theory amongst 99% of Australians (especially parents) at least. If you have the deposit ready, is it always better to buy than to rent?

Why You Should Buy

*Let me just make one thing clear before we delve into this debate. I’m going to be looking at this purely from a financial point of view. There are many intangibles that come from buying a home that you can’t measure in dollars. Your home is your castle that you raise your family in. There is an emotional attachment when buying a home which varies greatly from person A to person B.

I personally only really see one major benefit from buying a house to live in.

Security

It’s a pretty major benefit too. When you rent you are always at the mercy of the landlord. Rent could be raised at the end of your lease. Leaky pipes may never be fixed. You’re not allowed to buy a cat because it’s against the rules. And what happens if the landlord decides to sell to home owners who want to move in and kick you out? You have to find another place to live, and anyone who has ever moved or helped move someone can attest to how they would rather take a bullet than do that shit again. Ok it’s not quite that bad but it sucks trust me (have been involved in 10+ moves).

Forced Savings

Some people just can’t save money.

If it’s in their account and disposable, they just can’t help themselves and must spend it. I don’t have this problem personally but I understand that for many people it’s an issue. So how can you save money when you spend every spare dollar you earn?

Forced savings.

Unless you’re on an interest only loan, you will be paying some principal in your repayments each month. It’s the principal that actually pays off the home, the interest is just how the banks make their money.

The principal payment therefore are sort of like a forced savings mechanism. I say ‘sort of like’ because it’s a bit more complicated than thinking about it purely as savings. Theoretically if you bought your house for $X amount of money and sold it 30 years later for the same price after paying it off, then yes you would be essentially receiving a lump sum of all your principal repayments you have made during those 30 years (not factoring in buying/selling costs and inflation).

But! What happens if you never sell? What happens if the house goes down in value? What happens if no ones wants to buy your home?

It’s is extremely unlikely that you’re are going to have your house go down in value over 30 years but it could happen (see Japan). And it’s for this reason that savings via equity is not as straight forward as you think.

Regardless of these situations though, for people who struggle to save when they have disposable income, a forced savings plan might be a good thing for them. And the banks do a mighty fine job of making sure you ‘save’ every month. They are even kind enough to visit you if you miss too many ‘saving’ payments.

Why You Shouldn’t Buy

LOCKED IN!

Since already establishing what I consider the single and biggest pro when buying to be security, if find yourself in the dilemma of choosing between renting or buying you must ask yourself, why do I need security?

There is merit for people who need the stability that buying comes with. If you have pets, children, elderly parents who you take care of or something else that would be greatly disrupted if you ever had to move. Then I could 100% see the importance of security.

BUT! With security there also comes restrictions!

When you buy a home, suddenly you can’t just pick up your things and leave. You could rent out your house but that’s a pain in the arse. You could sell your house. That is also annoying and it costs money to do so.

Really, really expensive

Buying a home usually means taking out a mortgage. Having debt on something that does not produce any cash flow is a liability. Some people say your home is an asset, I disagree.

But lets push aside some negatives for the time being and imagine that you are someone who needs stability and believes that they are not going to want to live anywhere else for the next few years. Now you actually need to buy the house and pay it off over the next 30 years. Lets crunch the numbers.

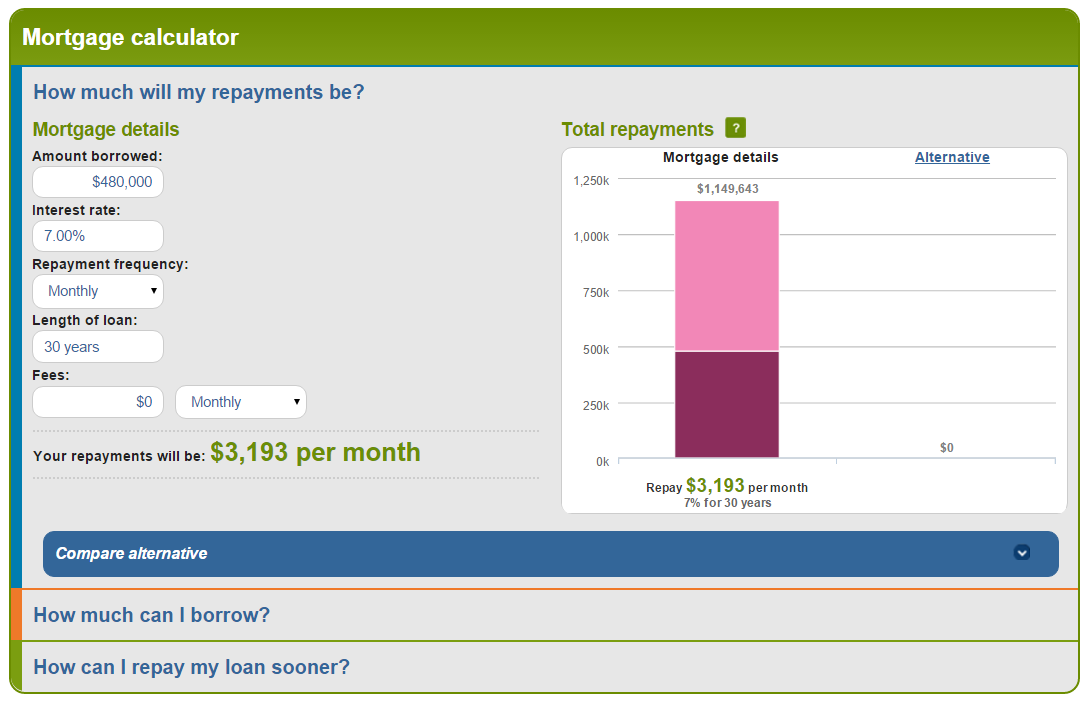

Everyone is different but lets just go with the standard formula of 25% of the purchase price (20% deposit and 5% buying costs). On a $600K house this works out to be $120K for the deposit and $30K for buying costs. The loan amount is $480K and even though interest rates are at historical lows now, they will eventually go up so lets just go with 7% fixed interest rate for the entire 30 years of the loan.

Firstly you may notice that the total cost of servicing this loan amount for 30 years equals $1,149,643.

Wowzers.

Secondly, the dark pink area represents the principal amount of the loan ($480K) and the light pink is the interest. You end up paying more in interest than you do for the actual loan amount… Just think about that for a second. Some say rent money is dead money, well the same can be said for interest too. YOU JUST SPENT $670K ON ‘DEAD’ MONEY!

It’s hard to even think about. If we break up that interest over the 30 years it works out to be $429 a week or $1,861 a month. You could rent a really nice place for that kind of money.

But because you have chosen to buy you have to pay the interest repayments PLUS the principal, which comes to $3,193 per month. That’s a shit load of money leaving your account each month. I don’t know about you, but that would severely impact my lifestyle if I had to make those repayments each month for the next 30 years.

So far we have $120K for the deposit, $30K buying costs and $1.15M for servicing the loan over 30 years. That comes to around $1.3M!

So far we have covered how much it’s going to cost you to buy the house, but we haven’t covered how much extra it’s going to cost you to keep it running.

Here are just some extra items that come with the privilege of buying:

– Rates

– Home Insurance

– Water Fees

– Body Corp Fees

– If anything breaks in the house (plumbing, electrical wires, air con etc.) YOU have to pay to fix it

In a publication from the RBA, they estimated that on average the running costs for a house is 1.5% of its value.

That’s $270K over 30 years to keep a $600K house up and running.

Combining the buying costs with the running costs comes out at a whopping $1.53 MILLION DOLLARS to buy and maintain a $600K house for 30 years.

Forget about Equity!

The other big benefit that a lot of people seem to bring up in this debate is that buying a home will make you money somehow? Last time I checked, buying a home TO LIVE IN does no such thing. You can’t collect rent when you live in your home (unless you have kids). And even if the house goes up in value, it is irrelevant because you can’t live in your house and sell it too. If you withdraw equity then I am of the opinion that you’re selling yourself short of the major benefit of buying a home in the first place (security). You could sell and buy another home BUT this was not the original purpose of buying. If you INTENTIONALLY bought a home only to sell it later in life for a higher price then you are actually investing and the ATO investigates these occurrences where couples may buy and sell every couple of years and take advantage of the CGT exception.

When you buy a house to live in, your goal should not be to sell it later for a higher price. Factoring this into account, I stand by my statement that you will not make money when you buy a house to live in. This removes any investment type gains home owners might be privy to when trying to compare to renters. We want to compare apples to apples as closely as possible. When you start talking about how much the house went up in value it should not be factored into the equation because if someone is happy living somewhere and never sells, then the equity gain is void.

Why You Should Rent

Flexibility

Other than your lease period, renters are free to jump from one place to another.

Don’t like the cost of rent? Move.

Don’t like the location anymore? Move.

Landlord not fixing things around the property? Move

I know that moving is a pain in the arse but do you know what’s more of a pain in the arse? Trying to sell your home AND moving.

It seems to be a growing trend among young people to spend their 20’s travelling around the world, studying and trying new experiences. And that’s awesome! I think that your youth, particularly between the ages of 23-29 is an extremely precocious and unique time in your life when you’re not tied down and most likely have finished your trade/degree and working full time.

You have full time money coming in, are young and can do what you want. Why would you want to tie yourself down by buying a house? You are in such a unique position to be able to drop everything and move/explore/discover the world.

Renting can provide you with the flexibility needed to live this kind of lifestyle.

I personally don’t intend to buy a home to live in until I’m ready to have kids, but that’s me and everyone’s different.

Usually Cheaper

If you think rent is dead money, then you must certainly see interest repayments on a home loan to also be dead money. You can work out the percentage of interest repayments quite easily because they are set by the bank. But comparing that to rent repayments is a bit trickier at first but is easy once you realise how to compare the two.

To work out if you are better off renting and saving money than you are buying and forcing savings (through principal repayments), you must know the rental yield of the property. To calculate this you have to know two things;

How much the place you want to rent is worth?

How much does rent cost?

For example:

The place you want to rent is currently being advertised for $400 a week and you think it’s worth about $600K because the place next door is nearly identical to it and is for sale for $600K. Rental yield is calculated using the following formula:

Rental Yield = R/PP

Where R = Rent (Per Year)

And PP = Purchase Price

In our above example this would be

Rental Yield = $20,800/ $600,000

Rental Yield = 3.5%

Can you find a bank with a lower interest rate than 3.5%? Right now the answer is no. The average interest rate for a standard variable loan is 5.1% and that’s with today’s historically low cash rates.

Considering today’s rental yields are 3.5% and 4.4% for houses and units respectively in all Australian capitals, you would either have to be paying above market rent or find a killer bargain for it to work out cheaper to buy than to rent.

It’s simple, is the rental yield you’re paying more than the interest rate you would have to pay if you bought? For the vast majority of Australians I would say the rental yield is going to be lower. There are a few places I have seen in the country where the rental yield is quite a bit higher but I have yet to see it in the capital cities, especially Sydney and Melbourne.

And this is not even factoring in all the other crap that comes along with buying (stamp duty, rates, insurance Etc.)

To compare to our example above. If we rented at $400 for 30 years and factoring in inflation at 2.5% we end up paying $913,176 in rent. This is being pessimistic too because I didn’t factor in inflation for the rates, insurance, body corp etc. above so it would have actually been even more to keep the house running over 30 years.

Still, this means that renting over 30 years come out over $600K cheaper than to buy.

However, the person in the above example now owns the assets outright and at worst is sitting on about $1.23M of equity ($600K over 30 years at 2.5% inflation rate) where as the person who rents has no equity.

** 27/03/2018 EDIT ** There seems to be a lot of comments about me using 2.5% in the above calculation. Australian property (all of Australia not just Melbourne and Sydney) has risen by 2.8% (real rate of return) during the last 30 years (SOURCE)! You could even put the return @ 5% and renting would still come out ahead.

I can’t account for all rates of returns. These are the numbers I have used with a source to back them up. Obviously if the return for properties increases in the future the results are going to be different. ** /EDIT **

BUT! The person who rents has a far greater cash flow position than the person who buys. The renter should have just over $600K (total cost to buy over 30 years minus paying rent for 30 years) extra over 30 years if they managed their money and saved the difference. This works out to be an extra $20K per year the renter has up their sleeve.

Lets assume that the renter realises this advantageous position and instead of blowing the extra $20K, they invest it yearly in a diversified portfolio. Suddenly something strange happens.

At $20K per year over 30 years with a rate of return of 9% (historic average) can you believe that the renter can amass a net worth position of $2.7M!!!

Sweet baby Jesus.

I don’t know about you, but I would much rather have $2.7M invested in income producing assets and have no house to my name than having a money draining house paid off with around $1.23M of equity that you might never tap into after 30 years!

Why You Shouldn’t Rent

Landlords, Leases and Leaks

Have you ever had that real asshole of a boss that is always checking up on what you’re doing, invading your privacy and never fixing the things that are broken at work?

This can be what it’s like when you rent. There are good landlords out there but there are also terrible ones.

Since you are sort of borrowing their house to live in for a while (renting), you can’t make changes to it as you please. For some people this is not an issue but for others (my old man included) it can be hard because they like to tinker, fix things and customize their home to their liking. You can’t exactly knock down a wall to expand your living room without receiving some sort of angry letter from your rental agent. Even if you’re helping to fix the property you can get into trouble. This sucks when there are issues with the rental, like broken heaters, leaky taps, out of service hot water systems Etc.

I hope you didn’t have your heart set on this place either. Because the landlord has just decided to sell the property when your lease period ends to the higher bidder. There is a chance that the next owner could want to rent it out too but there is also the chance that it’s a new family who want to move in straight away. Which means you will have to move out!

Luckily the new owner does intend to rent this pace out. You have lived there for 3 years and have a great history looking after the place. The new landlord offers you another lease and at first you are very happy, that is until you read the fine print which says they have just upped the rent per week by $20 bucks!

Ouch.

Might be time to move places, which of course means attending multiple open days, submitting application after application in hopes that you land one that suites. When you finally find one that you have been offered it’s now time to have a weekend from hell carting all your crap around town to the new place.

FINALLY settled you now sit back and relax in your new abode. 10 months pass and you receive another letter saying that the owners wants to sell… FFS!

No forced savings

If you have a hard time sticking to a budget than renting might not be the smartest move. It’s definitely possible to come out ahead when renting if you are discipline and can invest the money saved while you rent. But not all people can do this.

They see spare change in their account like an expiring gift voucher becoming invalid on Sunday afternoon. They MUST SPEND IT on the weekend with no time to spare! And even though it may be better financially to rent and invest the savings, not everyone has the will power to do this.

Final Thoughts

I think too many people (especially younger people) get caught up in what is ‘normal’ and buy homes young when they don’t even know what they want to do in life. If rent money is dead money than so is interest repayments, which are much higher than rental yields for the majority of Australians.

You do not make money when you buy a house to live in. You may get lucky and sell it at a profit later in life, but you never hear about all the people that sell at a loss, only the ones that triple their money in 4 years (bullshit artists). You shouldn’t be thinking about making money when looking at a home to live in anyway. It’s first and foremost your home to make your own and to raise a family in. If you want to make money, look at actually investing into income producing assets (stocks, bonds, rentals).

Don’t get caught up in the stigma and shame on renting, break down the numbers and work out what actually costs more. If it’s cheaper to buy then by all means go ahead and buy, if it’s cheaper to rent, ignore the misinformed who try to make assumptions that you can’t afford to buy or that you must be doing it wrong.

Try to break out of the Matrix and look at what is best for YOU not what others think is best for you.

Please feel free to share this article around if you know someone who may be tossing up between the two, it may help them decide.