In today’s episode, I’m speaking with two other Aussie’s (Tom and Ricky) who were with me at the premiere of the FIRE documentary ‘Playing with FIRE’ which follows 35 year old Scott Rickens, his wife Taylor, and their toddler Jovi as they embark on a year-long odyssey to understand the rules of this sub-culture and test their willingness to reject the standard narrative of adult life.

I want to congratulate Travis and the whole team who was involved in the creation of Playing with FIRE. The film is fantastic and I would recommend it to anyone as it’s a super interesting documentary starring so many of our favourite FIRE bloggers and was surprisingly very funny as well.

Some of the topics we cover today include:

The events that lead up to the Premiere

Our initial thoughts after watching the film

Things we liked and things we wanted to see more of in the documentary

Talked about how hard it must have been to fit an entire concept like FIRE within 90 minutes

The Q&A session after the film

And pretty much everything else we ended up talking about!

Today I’m speaking to one of the most popular FIRE bloggers in the UK, Barney from The Escape Artist.

Barney is a super interesting guy who is married with three kids, worked in Finance and managed to reach FI at the tender age of just 43. He could have done it much sooner too if he had discovered FIRE earlier in the piece which we get into in the pod.

Since I’m now living in the UK, I was particularly interested in what the FIRE community is like here and if there are any major differences in approach. We also have chat about the film that could be a game changer for the entire FIRE community worldwide, that is, of course, the documentary ‘Playing with Fire’ which is premiering in London on the 12th of June! And yes I will be attending the premiere and would love to see some Aussie help me rep the FIRE community if you’re in the area.

Some of the topics we cover today include:

Barney’s journey towards financial independence in the UK

*Human error can result in losses. Make sure you fully understand how matched betting works before trying this strategy out

Summary

My guest today is Nico who managed to create an online income stream through a technique called matched betting.

But don’t let the name fool you! Matched betting is not gambling but it takes advantage of the big signup bonuses amongst other things that the betting agencies used to lure people in.

The closest thing I can compare it to is signing up for credit card point to use on flights but matched betting is a lot more lucrative and easier IMO.

Nico runs Bonus Bank which is a website that helps Aussies with matched betting by finding the best opportunities out there. Make sure you stick around for the second half of the pod as Nico’s story about what life matched betting has enabled him to live is pretty cool and well worth a listen.

Some of the topics we cover today include:

What is matched betting and how it works

How Nico can make $300 tax-free dollars in 30 minutes

Geoarbitrage with matched betting

What is Bonus Bank and how they can help

Infamous Betfair signup bonus story about winning a couple of grand in one night

How Nico managed to replace the majority of his income through matched betting

If you do decide to sign up for a paid membership, the guys at Bonus Bank sorted out an exclusive deal only for Aussie Firebug Members where you will get 50% off your first premium monthly subscription if you use the coupon codeFIREBUG* this code has changed to a 3-day free trial instead (as mentioned in the podcast) The FIREBUG code has changed (from the start of Febuary 2020) and will now get you 25% off the first month of a Premium Monthly subscription

*Full disclosure. If you use this code, I will receive a commission through an affiliate program. Thank you in advance for helping me run and maintain this site 🙂

Update: The laws are apparently changing at the end of May 2019 and the Consumer Framework for Online Gambling has made a recommendation to remove of signup bonuses along with various steps to try and deal with problem gambling in Australia. We don’t know what this means exactly as I personally received the bonus even though I was registered in Victoria which was already a state that wasn’t meant to have them. From what I’m reading, if you signup and email them asking for the bonus, more often then not they are allowed to give it to you because it’s technically not a signup bonus but an incentive for an already established member. We will see how this plays out in the coming weeks.

This article is not going to go into whether the changes are good or bad, or even a technical breakdown of the franking system and how it works. In fact, the target audience for today’s article are people who understand the franking system and what the changes propose to do.

What I’m going to cover is the strange phenomenon I’m seeing more and more of as we inch closer and closer to the election.

Let me introduce you to ‘The Curious Case of Franking Credits and The FIRE Community’

What’s Being Said

Assuming that you’re up to speed with the debate at hand, I’m going to go over the most common arguments I’m seeing online and give my take.

“Franking was introduced to stop double taxation not to give refunds. Howard–Costello changed it in 2000. It was never meant to have refunds”

The reason that the franking system came about in the first place was from an independent review into the Financial System in the 1979 commission by the Fraser Government. This resulted in the ‘The Campbell Report’.

The fundamental principle behind dividend imputation is to ensure that income is taxed once by those obliged to pay it.

If someone does not receive the franking credit when their tax obligation is zero, they have paid additional tax when they should not have. This means that they have paid more tax than others who earn the same amount but through other means of incomes such as rental, PAYG, sole trader business, bonds etc.

For example:

Person A works part-time and grosses $16,000 a year. They are under the tax-free threshold and don’t pay any tax.

Person B operates a small sole trader business that nets $16,000 a year. They have no tax obligation.

Person C is retired and owns part of an Australian company through shares that bring in $16,000 a year. Person C receives a fully franked dividend of $11,200. Person C at this point has effectively paid $4,800 in tax on their $16,000 income. Under the current law, the ATO refund the $4,800 to keep things at an even playing field and treat all income fairly no matter how it was earnt.

If you remove the refund, Person C has to pay $4,800 in taxes when they are only receiving an income of $16,000.

Now back to the point.

The Campell Report did, in fact, have refunds included in it!

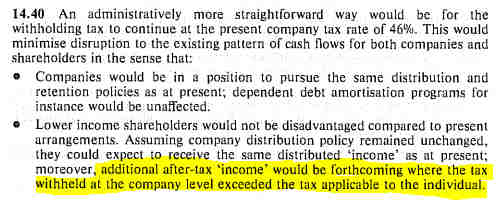

Cambell Review – 14.40

“Lower income shareholders would not be disadvantaged compared to present arrangements. Assuming company distribution policy remained unchanged, they could expect to receive the same distributed ‘income’ as at present; moreover, additional after-tax ‘income’ would be forthcoming where the tax withheld at the company level exceeded the tax applicable to the individual.”

AKA a refund!

What actually happened was the Hawke-Keating Government in 1987 implemented the ‘interim’ recommendation of the Campbell Review. This was not the original recommendation and ended in 1999 following the Ralph Review which introduced the refund of excess franking credits under the Howard Government.

The current system we have (which includes franking credit refunds) was designed by an independent body and was implemented with the support of both houses!

“A company and an individual are separate legal entities. A profitable company should always have to pay some tax. The franking credit refund is a loophole where the share payers can potentially pay no tax”

This is very clearly addressed in the Campbell Review.

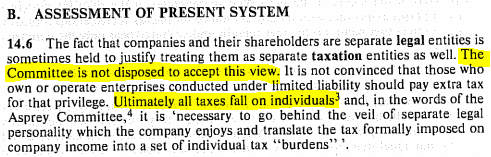

Cambell Review – 14.6

“The fact that companies and their shareholders are separate legal entities is sometimes held to justify treating them as separate taxation entities as well. The Committee is not disposed to accept this view. It is not convinced that those who own or operate enterprises conducted under limited liability should pay extra tax for that privilege. Ultimately all taxes fall on individuals and, in the words of the Asprey Committee, it is ‘necessary to go behind the veil of separate legal personality which the company enjoys and translate the tax formally imposed on company income into a set of individual tax ‘burdens'”

Pretty straight forward. They might be separate legal entities but all tax eventually falls on individuals!

The company is simply prepaying tax for the shareholders.

If you accept that franking credits can offset an individuals income to $0, you must accept the refund as the shareholder has prepaid more tax than they should have.

If you want to still argue this point. I’m assuming that you’re in favour of completely eliminating imputation credits altogether right…? Tax will be paid twice, once for the company and once for the individual. They are separate after all, right???

“These refunds are costing taxpayers billions each year. That money could be spent on schools, hospitals and roads. Why should the rich get a refund from the taxpayers?”

This is one of the first arguments from people who don’t understand how franking works. To be fair, most of the FIRE community-related arguments on this matter don’t raise this point. Because we fully know that the refund has absolutely nothing to do with other taxpayers and is simply returning money that is rightfully owed to the shareholders from which the money was earnt in the first place through the company!

I’ve yet to see anything that specifically stipulates that the ALP will use any revenue received by these changes on schools/roads/hospitals etc. What most likely will happen is any extra revenue will be added to the Federal government’s coffers where god knows what it will be allocated to.

Let’s take a little look at the fiscal management of the Government, shall we?

Same-sex marriage plebiscite for $80 Million – Clearly a stalling tactic the government used to postpone the inevitable. All good though, getting into power is much more important than using taxpayers dollars wisely.

$4 Billion Victorian desalination plant that’s hardly been used – To add insult to injury, it’s costing the taxpayers $649 million a year to keep this plant open even if it’s not producing water! I personally had a lot of friends work on this project and let me tell you, taking the piss doesn’t even begin to describe how much money was being thrown about on that job site. I’m all for unions fighting for their worker’s rights but c’mon… some of my apprentice mates were clearing $2,500 a week after tax whilst also getting $800 a week travel allowance and living away from home pay plus god knows what other EBA entitlements. Four or so of my mates were renting out a beach house in Inverloch and getting $800 a week each for travel pay… Inverloch to Wonthaggi (site of desal) takes 13 minutes 😐 I’m all for tradies earning as much as they can but when taxpayers dollars are used we need to look at the fiscal management of these projects… some of what was happening was a complete waste of money. This was one desal project, Sydney also have one that cost $1.8 Billion and is currently costing taxpayers $535 million a year to keep it in a state of hibernation. Other states have them too but you get the idea.

So what are we at now… around $20+ billion of wasted taxpayers money without even really trying (I’m allowing for some actual value of these projects to be returned).

Seriously.

These projects were off the top of my head and I did a bit of Googling to fact find. I’m sure there’s plenty of others out there that cost even more.

I have worked for the government for over 7 years and trust me when I tell you, we are not good at managing money/projects.

The late Kerry Packer summed it up best in 1991:

‘I am not evading tax in any way, shape or form. Now, of course, I am minimising my tax, and, if anybody in this country doesn’t minimise their tax, they want their heads read because, as a Government, I can tell you you’re not spending it that well that we should be donating extra.’

“Australia is the only country in the world that have franking credit refunds”

My response to this one has always been… so what?

I actually think it shows a sign of weakness from that side of the argument. I mean, what has that got to do with anything? There’s plenty of things unique to Australia.

Does that make us wrong?

No!

In fact, I’d wager that Australia must be doing a lot of things right as we are consistently ranked as one of the best countries to live in on the planet and our citizens are some of the richest in the world. There’s plenty of factors to attribute to these claims but it just strikes me as odd when people bring this point up as if it’s a bad thing 😕

The Propaganda Machine In Full Swing

The ALP are clearly trying to win votes from the working class by exploiting on their lack of knowledge around a policy they want to change (franking credits this time around) which is how politics have worked since the beginning of time.

They are spinning this debate into:

‘The rich aren’t paying their fair share’

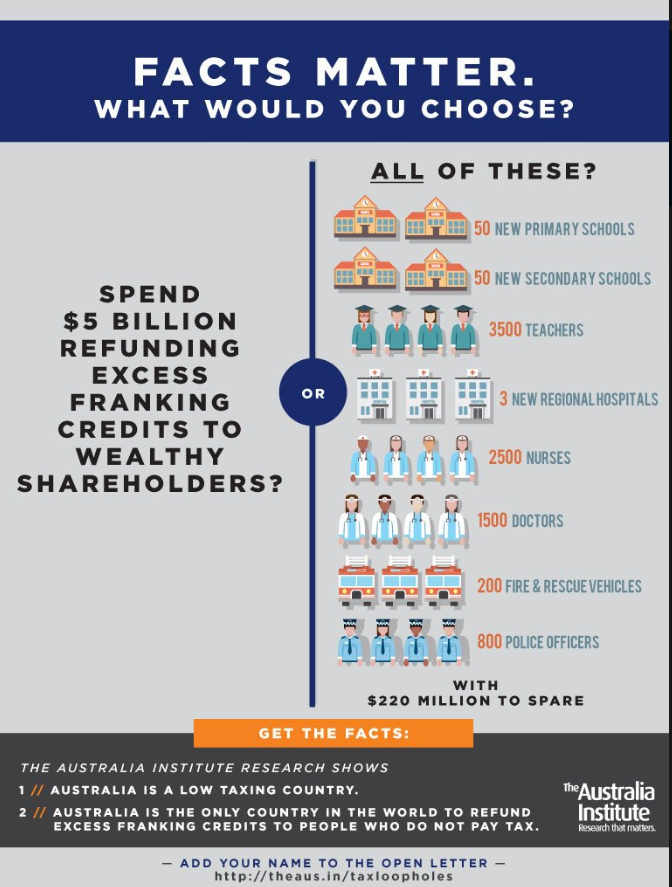

Check out some of their propaganda.

I have no idea who ‘The Australian Institute’ is but they call themselves a ‘think tank’ but are clearly a propaganda machine.

I really enjoy the play on words with the poster insinuating that the taxpayers are somehow ‘spending’ $5B to refund franking credits whereas we know perfectly well that the taxpayers don’t have to pay for anything. The refund is simply returning the tax paid by the shareholder if they paid too much tax that year…like … you know… how it works with every other form of income.

But hey, good job PR team! Nothing is more likely to get votes than if you pretend you’re fighting for the working class and trying to get the rich to pay more tax so you can fund more public services.

So Robin Hood of you. In fact, Robin Hood is almost a perfect analogy because this policy is indeed stealing from the rich but I’m not sure about giving to the poor. As I’ve covered above, the government sorta sucks with money and to quote Mr Packer again, if you think that the money that is retained by this policy (assuming they are able to retain any money, which is highly debatable) will be going to these public services … ‘You’d want your head read‘

There are also other countless articles written by prominent financial figures with large followings that also raises eyebrows about the sincerity or purpose of some of the content that’s published.

The real issue with this whole debate is the tax-free pension with Super. When you start to receive an income from your Super (pension mode) you don’t have to pay a single cent of tax on that income up to $1.6M. This means that because your taxable income is $0 if you receive Aussie dividends with franking credits attached… you guessed it, you will receive a refund!

The unsustainable tax-free pension mode of Super has been debated countless times and I’m not going to go into it.

But make no mistake about it, the ALP are targetting this and the FIRE community is getting caught in the crossfire.

‘But why wouldn’t they just change the law so there’s not a tax-free pension mode’

Because that’s not smart politics!

Does anyone honestly think that this move to axe franking credit refunds wasn’t strategic? Hell, half of the FIRE community doesn’t understand it well, how are we to expect that the general public will get it? The answer is they probably won’t. And I don’t blame them, it’s complicated and confusing. They are sold the dream that the wealthy will have to pay more tax (which will be 100% true) and that money will be used to fund public services (lol).

That’s a great PR campaign if you ask me. And incredibly hard to argue against because it’s so confusing.

Nevertheless.

Everything I’ve covered so far is pretty stock standard on the battlefield of the political juggernaut trying their best to win all of our precious votes.

But there’s something else afoot that I can’t figure out…

Where It’s Getting Weird

To summarise everything I’ve covered so far:

Franking credit refunds make perfect fiscal sense. They were designed by an independent body and implemented with bipartisan support

ALP want more revenue

They won’t directly tax Super pensions because that would be political suicide so instead, they have gone after Franking credit refunds and are exploiting the general publics lack of knowledge about how they work

Here’s my beef.

The entire reason this article exists is that I’m noticing a trend amongst the FIRE community where an uncomfortable number of members are not only in support of this change but are actively campaigning for it to go through.

This change directly affects the FIRE community!

If you are planning on retiring from Aussie dividends, you could be set back years until you reach freedom if this goes through.

Yeah yeah yeah I know you can tweak your investments to get around it and people did just fine without franking and all that but that’s not the point I’m making here.

My point is that a lot of the community is not taking an IDGAF approach. They are trying to argue for the changes that will directly disadvantage them and it’s doing my head in.

Here is what I’m talking about and I want to preface this by acknowledging that every single one of the screenshots below is from a FIRE or financial independence community group (Facebook, Reddit, forums etc). I have not included the whole quote or comment in some of the screenshots FYI.

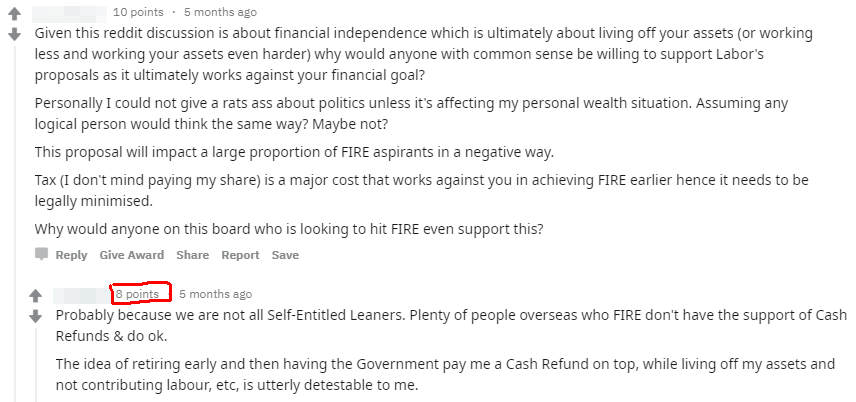

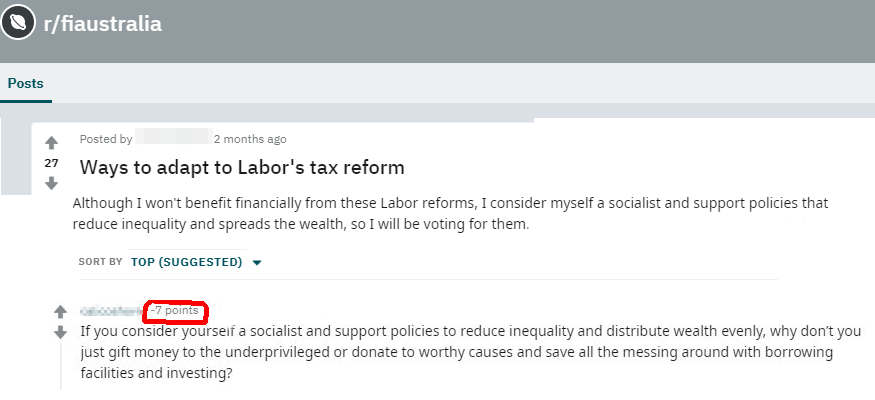

From /r/fiaustralia

The first comment pretty much sums up view spot on. I’m glad to see it sitting on 10 points (basically an agreement for those who don’t use Reddit). But the response has nearly the same number of upvotes which would indicate that a significant amount of the sub (which was small when this was posted) would disagree.

*(this edited screenshot is not the whole post, just the part I’m highlighting)

Same sub as above. 27 upvotes for a post that clearly states that they won’t benefit financially from these changes but will be voting for them anyway. This was posted on a financial independent specific forum. When another member replies with what I would consider a pretty reasonable response, they get downvoted and are currently sitting on -7 points.

Another forum member glad that these changes will go through. But the community is really getting behind this comment with 22 points.

FFS Maureen

Some ALP propaganda posted on the ‘Mustachians Australia’ group.

19 Likes and 3 Loves.

The first comment is even a clapping hands emoji.

PEOPLE ARE CLAPPING ABOUT THESE CHANGES IN A FIRE GROUP.

Australian Facebook group specifically geared towards reaching financial independence has the ALP propaganda we seen posted above… And wouldn’t believe it… It has 10 Likes and 2 Love reactions. People who are trying to reach FI are loving the fact that they will have to pay more tax… 🤔

Excuse me…

But what the actual fuck is going on?

I fully expect to see these sort of posts and more importantly, responses from any other group in Australia. I think it’s unrealistic for the general public or anyone who these potential changes won’t affect to give two shits. But a good percentage of the FIRE community actively promoting and wanting these changes to go through is… confusing me.

Why Is This Happening?

I don’t really know but I have four theories.

The most likely theory I have is that there is still a decent amount of people in the FIRE community that still don’t quite know how franking works. The refund can be confusing to understand. Combine this with a slightly naive attitude towards how tax dollars are spent and what you have is a genuinely good-hearted person who just wants to spread the wealth around. All I would say to anyone who falls in this category is please consider direct donations to good charitable organisations. I have worked for the government for over 7 years. Trust me when I say that you are 100% better off directly helping out the less fortunate than you are by paying more taxes in hopes that it will be put to good use.

The FIRE community was once a smallish niche group that all had aspirations of escaping a lifetime of working a job they didn’t particularly enjoy. And then the word got out, and what started off as a relatively small group has grown exponentially. I suspect that there are a lot of people out there that are apart of FIRE groups, forums and pages that have no intention of doing what’s necessary in order to FIRE. Maybe the influx of FIRE phonies are delighted with this speed bump in our road to FIRE. This can best be described as Tall poppy syndrome.

Some out there have been drinking the ALP ‘Kool-Aid’ and actually think that franking credit refunds don’t make for a good fiscal policy.

And now it’s time to put your tin foil hats on…Although highly unlikely, is it possible that members of the ALP have infiltrated the FIRE community? I honestly don’t think we’re big enough for any political party to really care about, but maybe there are a few interns out there pushing their parties’ agenda… Stranger things have happened!

Conclusion

Guys, I get it.

You should never base your strategy around tax laws. The most important rule for investing should always be to invest in great assets (whether that’s locally or internationally). Tax strategies should come later down the track and we shouldn’t get too upset when they change or are abolished. This is to be expected at some point after all.

I’m not saying we need to band together to fight this (I’ve got better things to do), but for the love of God, we don’t need to be actively campaigning to disadvantage ourselves.

Maybe I’m missing something here, but I can’t work out why so many of us are happy to pay more tax to a government who has consistently shown its incompetency to spend money wisely.

I’m really interested to know what the community thinks.

Are you picking up what I’m putting down? Or maybe I’m just out of touch and need more faith in the government?

Please let me know what you think down below 👇.

Spark that 🔥

*Credit to these two Cuffelinks articles for most of my research around the history of franking. Article 1, article 2.

Late last year I woke up to a message from someone who lived in the same town as me saying they knew I was the Aussie Firebug and that my secret was safe with them…

I immediately jumped to the worse conclusion thinking maybe my boss had figured it all out 😱.

But it ended up being my mate from high school who as it turned out, was just as crazy about all things personal finance and investing as I am! It was my mate, Jimmy!

We’ve had countless chats at the pub multiple times about a whole bunch of stuff since that faithful message.

Today’s episode is two mates who went to high school together having a good old yarn about financial independence, investing, ETFs/LICs and much more.

Some of the topics we cover today include:

How Jimmy discovered my alter ego ‘Aussie Firebug’

Jimmy’s story about financial independence

Real estate investing

How Peter Thornhill ‘cleared the fog’ for investing in shares

Jimmy’s strategy that looks at the number of units of a fund as opposed to what the fund is worth when setting the target