by Aussie Firebug | Sep 30, 2016 | Real Estate

If/when you get to a point in your life where you own multiple properties, you will no doubt come across the term ‘cross collateralisation’. It’s a very important loan structure issue that you must fully understand if you ever do decide that it’s the best option for you. Many mortgage brokers (my first included) don’t actually understand the full implications themselves and are more than happy to sign you up for it because it’s usually an easier process. Cross collateralisation can very rarely be a good option, the majority of the time it simply increases the investors risk and strengthens the banks position of power.

Cross Collateralisation Explained

Cross collateralisation is when you use house A as security for purchasing house B.

Lets look at how you buy a house in the first place. THE most important thing when buying is….THE DEPOSIT! Banks love that shit. If the deposit is big enough you can pretty much guarantee that the bank will approve your loan.

No Job? No Education? No prospects?

Got a huge deposit, no worries. (I’m talking like >70% here guys)

It’s important to understand what the actual deposit means to the banks. It’s their way of lowering their exposure to risk.

Think about this. If you buy a $400K house with a 20% deposit that means the banks lent you $320K. Worst case scenario for the banks is you default on your loan and they are forced to sell to recoup their investment (the loan). They are not worried in the slightest about making money from this property, they just want their money back asap.

Ever wonder why you always hear of these stories of foreclosure bargains? It’s because the banks could not give two shits about an extra $10K, $20K or $40K. That’s pocket change to them. They just want to get back what’s theirs.

So now they have this house which the owner paid $400K for. Unless there has been a big downward swing in the market you would surely think that the banks could at the very least sell it for somewhere near the $320K mark. If they do then relatively no harm done, they loaned out $320K and got back their investment. No money made but minimal lost…except if you’re the poor sod that applied for the loan. You’re probably down the shitter now but like the banks care right?

So as you can see, the deposit is king to the banks and without a decent sized one (at least 20%) you are likely to pay exuberant fees to get the loan approved.

So why have I explained the above? Well as I have already mention, deposit is king. But what if I told you there was a way to get a loan approved without having to fork out one dollar? With the flick of a pen you can have access to hundreds of thousands of dollars.

Sounds too good to be true.

Enter Cross Collateralisation.

No Such Thing As A Free Lunch

Cross Collateralisation uses equity as the ‘down payment’ instead of cold hard cash. To simplify things, lets assume we have $200K of untapped equity on our family home (House A). We want to buy House B for $400K but don’t have a deposit.

To secure the loan we can use the equity from House A as collateral. This essentially does the same job of lowering the banks risks, just utilizing a different method.

House A Loan: $300K

House A Value: $500K

House B Loan: $420K (loan includes 5% buying costs)

House B Value: $400K

Security: $500K + $400K (the value of both properties)

LVR : $300K + $400K = $700K

. $500K + $400K = $900K

= 77% LVR (loan value ratio)

There will be a section in the loan contract that details that this loan is secure using another property over which the lender holds it’s mortgage.

‘Wow that’s pretty cool isn’t it? Didn’t even have to save any money to buy another property and the banks made the loan contract a breeze. I’m going to buy all my properties from now on using this method’

You must consider the ramifications first.

1. Selling Headaches

Every wonder what happens when you want to sell the property that you used to secured the others?

To put it simply…Whatever the bank decides is going to happen.

They have complete control over the proceeds of the sale. I hope you didn’t have anything planned for the money you were going to get when you sell House A. Because the bank has just decided that House B is at a higher risk than when you first bought it and now requires your loan to be at 70% LVR. So that $200K you just received is going straight to the loan on House B…Nothing you can do about it.

And if you think that’s bad. Imagine a situation where you have secured multiple houses with multiple other houses…shit show.

2. Equity Withdrawals

At the moment, if I want to withdraw equity from one of my properties it’s super simple. I apply for the withdrawal and as long as I’m keeping it under 80% LVR there are minimal hoops I have to jump through. I’ve done this three times now (once for each of my IPs) and it’s been very straight forward.

There has been times though where one of my properties have gone up in value and the others have gone down. Because my properties are not cross collateralised I am able to access the equity from the IP that went up because they are seen by the banks as separate .

If you have all your properties cross collateralised however the bank views all of them as the same. You might have had one IP go up by $50K but the others go down by $30K each. This would mean you can’t access the equity on the one that went up which may impact your opportunities moving forward.

3. Want To Swap Lenders?

‘Hey look at that! CBA has been ripping me off with their high interest rate. I’m going to move all my loans to the lower rate at Ubank’

People do this all the time. The problem with Cross Collateralisation is that you can’t just move one or two loans across. You have to either move everything or nothing. Depending on who you’re going to they may not want that level of risk exposure. They might charge extra fees for having to value all the properties to determine the position.

In short it’s a pain in the ass for a process that is so much easier for stand alone loans.

4. Complicates Things

The extra paper work you have to complete only increases the more you cross collateralise.

Want to sell? Complete evaluation of your entire portfolio (assuming you have cross collateralised your entire portfolio).

Want to withdraw equity? Complete review of your financial position on all properties.

Want to move banks?…. You get the picture.

What To Do?

If you discover cross collateralisation exists in your portfolio without you even knowing it (happens all the time) there are a few things to consider.

Cross collateralisation isn’t a problem… until is it.

What I mean by that is that it’s perfectly fine to cross collateralise if nothing goes wrong. But the odds of something undesirable happening increase when you cross collateralise and it usually only benefits the bank.

If you want to uncross your loans go see a mortgage broker who can assist you and work out a plan of attack.

Stand Alone Loans

You really want all your loans stand alone. The only advantage I really see for cross collateralisation is the convenience of setting them up. The banks really like to strengthen their position so they make it super easy to cross collateralise.

The thing is, if you have equity. You can withdraw the equity as cash and use that cash as a down payment for a new loan. I have utilized this method in the past and have had great success with it.

You have to check with your lender on the conditions for equity withdrawal but if you can do it, it’s a much smarter way to buy your next investment as opposed to using cross collateralisation.

Wrapping Up

Cross collateralisation may be convenient and appealing for investors looking to buy a new property without using their own money. However, cross collateralisation rarely is a good thing and the majority of the time it does nothing but cause headaches later down the track. The banks prefer cross collateralisation because it strengthens their position of power and they have all the control.

If you have equity available, look to withdraw this equity as cash to use as the down payment for the new loan. You might have some short term pain with a bit more paperwork and a few more hoops to jump through but your future self will thank you for laying the foundations of a strong portfolio now rather than later.

by Aussie Firebug | Apr 30, 2016 | Real Estate, Saving

It’s a decision most homeowners know all too well. Fixed or variable Rate? Do I fix my interest rate? Or do I go variable? Will the rate go up and I’ll feel like a champ if I fixed? Or will it continue to drop and I’ll just not tell anyone how much more I’m paying every month?

To Fix, Or Not To Fix?

There are some pros and cons for both. The main arguments made for fixing often include:

– Stability with repayments

– Laughing at others when rates rise

While the downsides usually are:

– Can’t make extra repayments

– Have to pay fees to set it up

– No offset

– No redraw

– Big, expensive, want to make you burn down the bank break fees if you ever decide you need out

– Crying internally if rates drop

Variable is basically the opposite of above where you have a lot more freedom and flexibility with your loan. You do pay for this extra freedom however by exposing yourself to more risk.

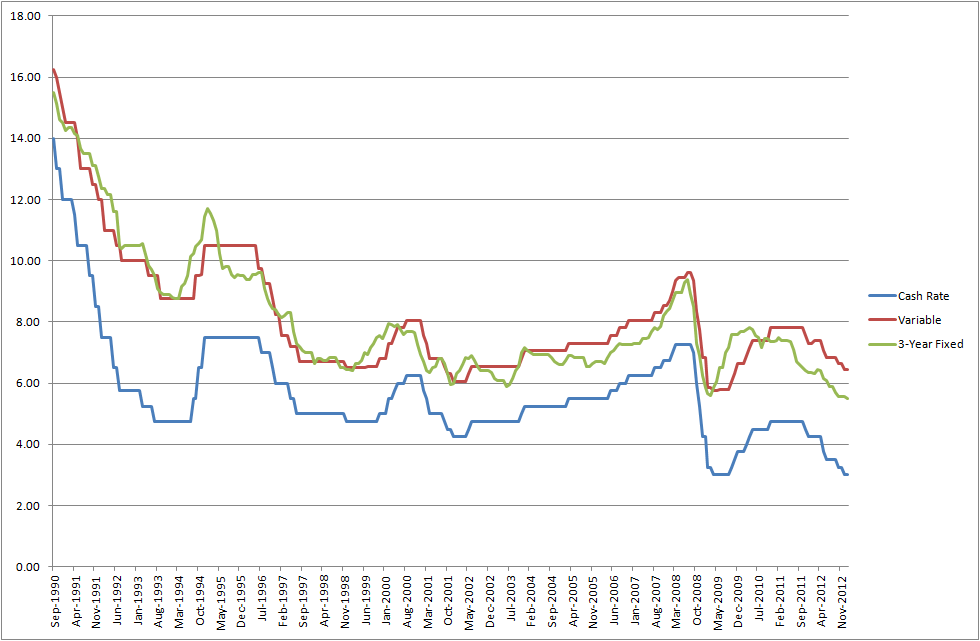

What’s interesting is that at the moment of writing this article you can find plenty of fixed rates that are lower than variable. I had a quick look at some historic fixed or variable rate data and it seems that this is not so uncommon.

Source:RBA

I was under the impression that fixing your rate usually meant that you pay a higher rate but upon further research, this wasn’t the case.

So if a fixed rate is lower than your variable AND provides the security of a fixed rate, there’s no reason I shouldn’t fix right?

Yes and no.

Make no mistake about it. The banks are ALWAYS aiming to make the MOST profit at ALL times. If you think you will pay less by fixing your loan for 1, 3 or 5 years after you have factored in all the extra fees and potential rate movements then, by all means, go for it. But just remember that the banks have an army of analysts that are betting against you. Just look at the above graph and try to find a couple of years where fixing your loan will come out ahead.

And remember that you have to factor in the fees associated with setting up the fixed loan and keeping it.

Here are the CBA’s fees for fixed loans. Scroll all the way to the bottom to see the fees. They include:

- $600 upfront establishment fee

- $8 monthly loan service fee

- $750 Rate Lock fee. Applies to each Rate Lock. Only available on 1-5 year periods

That’s $1,446 in fees straight off the bat. How much of an interest rate hike would be needed for you to recover those losses and come out ahead vs variable? It depends on your loan and rate but there needs to be a BIG rate hike. And that’s just for one year. If you decided to fix for 5 years, the fees are spread out that’s true. But again, take a look above and try to pick any date where a 5 year fixed rate would still be lower than variable during its whole lifetime and by how much?

Are you starting to see how hard it is for this to actually pay off? There have been certain periods of time where fixing has been better no doubt about it. But how good and confident are you that you can get the timing right? The banks have an army of people working full time on this stuff and STILL get it wrong.

I truly believe that you’re gambling if you’re trying to fix your rate to save money. And the ones that win 90% of the time are the banks.

If you’re fixing for stability or peace of mind then that’s different. But don’t think for a minute that the odds are in your favor by fixing. If you do actually come out ahead it will almost certainly be because of luck and not your amazing analytic skills that you predicted that the banks didn’t.

Split Loans?

I’m not a fan of split loans because it’s sort of like taking the worst bits from each loan type and combining them into a shit sandwich.

Let me explain

Some of the main benefits from variable are:

– Loan flexibility

– Being able to refinance if needed

– Benefit from rate drops

– Offset and redraw

– Can pay off the loan at any rate you want

You get half of the offset, rate drop and redraw (assuming you split 50/50) which is Ok but none of the other benefits.

You still can’t refinance the entire loan, you still can’t pay off the entire loan.

Your flexibility is about as good as a pair of chalk hamstrings

You’re taking on all the risks associated with variable but not benefiting from all the advantages.

The main benefits of a fixed loan are:

– Stability with loan repayments

– Protection against rate rises

You lose both of those things with a split loan. Yes, you’re only going to have increased repayments from half the loan if rates do rise but then what was the purpose of fixing half the loan if your paying establishment fees for the fixed loan which will probably be more than the interest repayments from the rate rise???

And you’re stability is gone too because you still have the potential to pay more from the other half of the loan if you split.

But you still have to pay the setup fees plus you’re locked into the loan.

You’re getting nowhere near the benefit of either strategy but all the negatives from both. If you want stability and certainty then go with fixed. If you can handle rate rises, go with variable.

Wrapping Up

Maybe I’m wrong with my analysis of ‘fixed or variable rate’ and maybe I’m about to be blasted in the comment section about all the people who have ‘beat the banks’ by fixing their loan at a certain time. I’m a variable man, the flexibility, and freedom of a variable based loan is something that appeals to me. I think that fixed loans were invented by the banks to prey on the Ned Flanders of the world (the over cautious) and take more money from them by giving them peace of mind. That being said, if a rate rise means that you’re going to default on your loan, then you should definitely fix because you’re most likely overextending yourself financially. For the rest of us, riding up and down the variable roller coaster is financially better, for the majority of the time

by Aussie Firebug | Feb 2, 2016 | Financial Independence, Investing, Mindset, Podcast, Real Estate

[soundcloud url=”https://api.soundcloud.com/tracks/281465926″ params=”color=ff5500&auto_play=false&hide_related=false&show_comments=true&show_user=true&show_reposts=false” width=”100%” height=”166″ iframe=”true” /]

Subscribe on Itunes Subscribe on SoundCloud

Subscribe on SoundCloud

In this episode I chat to Ben Everingham who was able to retire from full time work at the age of 29.

Ben knew he was not wired the same as everyone else when he started working full time and quickly discovered that the ‘normal’ working life was never going to make him happy. After a Euro trip at 19 and finishing Uni, Ben was able to land a great job in Sydney earning over 6 figures. Most would think that they have it made with a great job straight out of Uni but after working a while Ben knew that this job was never going to satisfy him long term and whilst the money was great, he was miserable.

After reading Rich Dad Poor Dad, Ben’s eyes had been opened up to the possibility of investing and business ownership. Eager to get started, Ben was able to purchase 6 properties within 4 years and started his own business, thus achieving his goal of quitting full time work before the age of thirty…

Transcript:

Aussie Firebug

Welcome to the Aussie Firebug podcast where we talk about finical Independence in Australia

Today’s guest is Ben Everingham who managed to retire froem full time work at the amazing age of 29

Welcome to the podcast Ben

Ben

Thank you so much, excited to be here

Aussie Firebug

I guess we’ll start with, lets just go back to the very beginning

When did you know you wanted to be financially independent?

Or when did you even discover the concept of being financially independent?

Ben

That’s a really interesting question, so there is probably two key stories for me that really stand out from things that have happened over the last ten years that were really meaningful

One was when I was 19, we were sitting around having some beers with about 20 of my mates at the times at the age when you still have the big crew of people that you hang out with at the weekend.

We were sitting around and someone suggested that we book a trip to Europe in a couple of months, so the next day four boys and myself went and booked the trip and two months later we were over there.

It was the exact sort of trip that you would imagine a 19 year old would sort of do and that was sort of the partying and having a fun time.

I got to this point actually it was probably 6 weeks into the 8 week trip and I’m sitting watching the sun set on my own in Paris watching the sun set behind the Eiffel tower and I was sitting there and I know this may sound a little strange but as I was looking at the Eiffel tower and I was looking at the sky and at that time the sky looked extremely chaotic to me and all of a sudden, I looked up again and it was almost like it was…this is really odd especially for me…it was almost like the starts had become straighter and align themselves and it was like my future was opened up to me and I knew at that point I had to do something difference it was a massive transformation experience for me

Aussie Firebug

Wow that’s quite the epiphany

Ben

Haha I don’t even know if I believe in this stuff. but it was one strange moment that, like it was literally like it was my future was mapped out in front of me and I knew not at the time what I needed but I knew that was on my way and so I came back and moved to Queensland from Sydney. I thought that in that time of my life I needed to get away from lot of influences in my life that were, you know a lot of party people and not a lot of people that were really going anywhere and so I started fresh and that was the first major experience

Aussie Firebug

Wow that’s crazy

So let’s just rewind a bit, so you were 19, were you working full time at that stage or at Uni?

Ben

Yeah I dropped out of Uni about 6 months into my course and it was my second gap year. I took two gap years basically. So I had been working full time for about six month saving for the trip

Aussie Firebug

And was that an eye opener? Because I know for me when I first started working full time, it was mind blowing. I always knew the hours and I know people went off and worked 8-5 Monday to Friday but it’s not until you actually start doing it I think…it’s such a full on experience…OMG it’s just so much time I’m at work. And I quite like my job. I don’t know if you went through a same experience. But I remember my first year that I was just like “this is crazy!” and I don’t even work that many hours.

I have mates that do the fly in fly out work and their working 4 weeks straight with one week off. This is mental! It’s wasting so much life?

Did you have a similar experience in them 6 months when you were saving for your trip?

Ben

Absolutely I knew from the first day I started my first job that I wasn’t wired the same way as the people I was working with. My first job was with the major elevator company as a laborer or a laccy one of the electricians and I just realised I was wired differently straight away like I wasn’t interested in taking breaks I was just interested in interested in getting the job done as quickly as possible and getting the hell out of there. I worked in that job for the six months before a left and I used to have this guy who was about sixty years of age who used to ride me every day and the day that I left he said sorry to see you go, you were the best young employee we have had here and I really thought you could have gone a long way. And I was like your half the reason I was bailing on this job because you are such an ass to me for that period of time. Ha ha hah. It’s funny how, how things come around like. It was definitely an eye-opener and it is something I would definitely never want to do it again.

Aussie Firebug

Right so you knew that you didn’t want work full-time for the rest of your life. And you go on this trip and the stars align and your like something is happening here I need to change my path so then how do you then, from that moment… because a lot of people don’t realise that financial independence is a thing. I remember reading about it, I was like my mind was just blown, I was like you just keep buying these things that make you money assets, and if you buy enough assets they can replace your income. My mind was just blowing when I read that I was like that so simple why hasn’t anyone told me about that before or why haven’t I heard that before. Then I had my doubts, I’m interested to know your experience with that. Was that something that you’ve always been around all is their family members that had reached it would do you discover that on your own?

Ben

No unfortunately I had to discover that my own not a lot of people that I grew up with all their families or my families had a huge amount of surplus money at the end of the week or the months so fast forward from Europe four years I was finishing a university degree in about six months before finishing the degree I picked up this book by Robert Kawasaki called Rich dad poor dad. I’m sure a lot of people listen and have read that book it such a foundational book for a lot of people as well. And I read this book and I just said, holy shit. It completely opened up my eyes to what is possible and from that moment forward I knew that assets and businesses were better than wages and jobs. I focused on buying assets as soon as I finish university with the intention as soon as I have the right skill set to go out to succeed to leave full-time work and start a business.

Aussie Firebug

Yeah I almost had an identical experience. Rich dad poor dad was actually the second financial book but I ever read. I originally read Stephen McKnight’s book 0 to 135 properties in 3.5 years. That’s an awesome book. I remember the same sort of thing, just reading that and your like this is like so up my alley and why isn’t everyone doing this. Rich dad poor at is a really good mindset one I think, gets you to think about things differently. It just makes so much sense, when I was reading that I was like this this is exactly what I wanted to do. You know trading your time for money for 40 or 50 years and relying on the government to help you out with retirement just seemed crazy to me. I always have in the back of my head, that people were actually retiring early and that just blew my mind. And I just had to get there as soon as possible. Yes that book was a big eye-opener for me as well

Ben

I remember something that happened to me post university. I was lucky, I got accepted into one of the big companies in Sydney’s graduate programs, for a lot of people that’s a fast track way to make a career. I realise that once I finished high school, done the degree gone and worked the big corporate job I still was never going to be fulfilled doing that. It was at that point I went on a trip with my girlfriend who is now my wife to Bali after working with IBM for a couple of years. She said your miserable and you’ve got to leave and at that point again we packed up a second time and moved from Sydney to Queensland and from that moment forward I didn’t make a single decision again based on fear or lack or something that wasn’t in alignment to where I truly wanted to be. And I just decided from that point on I would actively gain the skills required to actually be a business owner as opposed to an employee long-term.

Aussie Firebug

Right so you knew that working for someone else and doing the normal 9-to-5 day grind career sort of thing wasn’t for you. So you read Rich dad poor dad, was investing or businesses your first preference. Where did you sort of go from there?

Ben

So investing was definitely my first preference because I came from mindset which is probably like a huge amount people in your audience which is you have to follow a certain path to achieve a certain result and that path is School, University, great job paying a huge amount of money, and maybe investing in a couple of properties and retiring.

For me I listen to this guy a huge amount when I exercised called Jim Ronan who talks about financial independence and achieving financial independence. His first goal for every employee is to replace their full-time wage while their working in their job. And then he goes on to say that he replaced his full-time wage by three times before he left his job. That was always my goal, so I was earning good money over six figures by the time I was 23/24. And I was looking to replace my wage by three times which was a ridiculous goal. I don’t know why I had that goal, it was probably because I was listening to him so much and I thought that was financial independence. Where it ended up being someone further down the track that convinced me to leave my job because I replace my basic living expenses and I was ready to move on and do what I love full time.

Aussie Firebug

Right so you went down that investing road first and you discovered property, why properties what attracted you to property?

Ben

I think the number one attraction to me was that I understood it. I have met people during university that were millionaires through property and I knew that they weren’t smarter than me, I knew that you didn’t have to be a rocket scientist. And I just love it, I love the concept of buying something of average quality with potential and manufacturing potential into the deal. And I also thought the one thing you can do with property was use leverage. I only had a $20,000 deposit within the first year of leaving uni and I knew that 20 grand leveraged in shares might have only been about $40,000 I could buy whereas with property at the time I could buy a 400,000 asset using first home buyers grants and things like that. So for me that was extremely attractive because leveraged and compound interest to me is what it’s all about

Aussie Firebug

So what sort of property investor would you say that you are? Are you buy and hold sort of guy or are you into developments or renovations?

Ben

I’m all about buying and holding now but by buying and holding I develop or renovate. I will never just buy and hold something and hope that the market goes up I will make sure I can manufacture at least $100,000 plus into the deal before I even buy.

Aussie Firebug

You retired from full-time work at 29 do you work at all these days?

Ben

I actually work harder than I have ever before. But I actually work doing what I love every single day which is helping other people buy property. It’s my passion I am absolutely obsessed with this stuff it’s all about contribution now as opposed to making cash though.

Aussie Firebug

It’s funny that you say that work harder than you ever have before because I read a lot about people that have made it to the end goal. They’ve reach financial independence… because some people do it without ever starting their own business. They just work their 9-to-5 today job and they slug it until they have enough investments to cover their living expenses which is totally Ok way to do it. It’s interesting to read about those people into a like that is a lot of say that when they get to the end of the journey, like they only have six months to go and theoretically should be able to retire really soon. Suddenly working this job is a lot better and waking up to go to the job is suddenly not as difficult and not so much doom and gloom as it was before like it was 10 years earlier and couldn’t see the light at the end of the tunnel. Is that psyche sort of in your mind, you could turn around tomorrow and say hey I don’t want to do this I have enough money from my investments to retire and not work whenever I want to. Do you think that plays any part of it in what you doing now and why you work as hard as you do?

Ben

For me I would never be content it’s just not my nature. I come from a competitive sports background type, I can’t help it I love being involved in the game. I don’t want to be a spectator to life. For me I get a lot of my needs for significance and contributions through my day job now. For me those basic needs like survival and basic living needs are met and those things that are a little bit further up the chain to me get met through work. I’ve tried to sort of kickback, saying that. We have taken at least 12 weeks off in the last 12 months to travel and holiday and spent time the family. We will work extremely hard but will work extremely focused as well. It changes the way you work from 9-to-5 to working extremely hard for stints and then playing or relaxing extremely hard to stints as well.

Aussie Firebug

That’s awesome that you have the flexibility to do that and is one of the main things that attracts me to strive for financial independence so it can give you just that, the independence to do whatever you want and go on holidays and spend more time with your family. I know now I’m working full-time and it’s crazy, like I have a partner and I play footy, I swear I hardly have any time as it is now. I commute now each way to work which doesn’t help that but still, I’m thinking down the track and see people having kids now and am thinking how am I going to get the time to do everything I enjoy, seeing I already don’t have enough time as it is now and I know what people do when that happens they have to give up something, they drop the gym they drop the footy they drop something they like doing this just like work kids and there is very little fun time in between for yourself. And I just did not want to be in that position which is why am trying to get to where I’m going. Having children now yourself, you have two kids, that must be an absolute pleasure to you and your wife to know that you have that flexibility.

Ben

absolutely to me a huge part of our motivation now comes from our kids. Kids changed everything. One thing growing up is that my dad worked really really hard he come from absolutely nothing. From the time I was one half to the time I was four and a half we literally lived in a caravan while they saved for their first property. They bought their first property when interest rates were at 18%. My dad couldn’t buy a beer at the end of week that how hard it was. I learn’t from observing them that one, I don’t want to miss those early stages which is why I left work when my daughter was a year and a half, I’ve already felt like I’ve lost more than enough time in her life.

And secondly my dad ended up turning his situation around by turning around buying some great investment properties and starting some really successful businesses that are still running 15-20 years later. Listening to them and seeing the things that they missed out on that if they have made decisions at the age that you and I are their time now would be completely different. I don’t want to trade time for money and I don’t want to miss out the most important things which is being able to say yes to most of to the things that you really care about and to find time for the things that inspire you to do your best work and not to just exist there for a pay cheque.

Aussie Firebug

Sounds like he was a bit of an entrepreneur himself. Sounds like you’re a bit of a chip off the old block. Sounds like your old man had some influence on you.

Ben

Yeah sure he showed me it’s possible and he didn’t have a businesses that failed. I never looked at business is a risk as I could see how it could work.

Aussie Firebug

Absolutely and I think it’s a big thing about it to see people who have actually done it. Before I knew any about anything to do with financial investing and financial freedom and all that. Once you discover it, I went to a heap of property conferences and I’m meeting all these people and it’s like whoa they’re actually out there, these people actually doing it and now I’m interviewing yourself that retired from work at 29 its crazy. It’s awesome, you have that the back your mind that this might be possible, you read about it but when you meet someone who is actually doing it that puts it into perspective and it really validates it that this is the actual thing. You manage to retire from full-time work at 29. Your parents managed to buy a property when interest rates at 18%. Do you think properties in the two capital cities are unattainable and what would you say to people for people looking to buy properties in the two capital cities where the prices are very very high at the moment. What are your thoughts on that and that current situation.

Ben

I wouldn’t touch Sydney or Melbourne personally with a 10 fioot pole. I mean if you paid me to invest their down there now I wouldn’t even considerate it. And that’s because something that I read by Warren Buffett a long time ago is don’t rush into markets that are at their peak and don’t buy markets where everybody else has just bought. Like the successful people in Sydney and Melbourne are the people that have own properties the 10 years and have cashed out or made equity through this boom. They are not the people who have just bought in the last 12 months. My thoughts is that there are parts of both of those markets that of extremely affordable and extremely attainable now. But you’re probably got to be a little bit more creative in the product that you’re buying. Maybe the dream of buying the four-bedroom two bathroom home on a 600 m² block for a lot of people in our age group is completely unattainable now but there is still plenty of value in the right sort of town houses in the right sort of suburbs. I think that the good buying in areas like that will be in 3 to 4 years times where you have these people that earning 100 grand a year who now own million-dollar properties and interest rates go up to 7 or eight or 9% and all of a sudden these people can’t afford to service the interest let alone the principal repayments on their loan and a huge amount of distress property comes back on the market. That will be a good time to buy if you can financially put yourself in the position to capitalise on that.

Aussie Firebug

Sure

Ben

It’s all about timing. Right now doesn’t represent good timing in the market.

Aussie Firebug

Your talking about an investment point of view, what about someone who just wants to buy a house to live in. So there not looking to invest. What advice would you give to people that are looking to break away from that renters, not trap…but that renting for the rest of your life. Do you have any tips or tricks? If you were a young man in Melbourne right now earning around $80-$90,000 dollars what would you sort of do? Would you move to an outer suburb or look to advance your career? How would you tackle that?

Ben

Through my businesses I to get to speak to a lot of young motivated people. So what I generally suggest is that, put ice on trying to buy the property that you want to live in in Melbourne for the next five years, and over that five-year period focus on the building of a fantastic business is that’s the way you orientated which most people aren’t. If you’re not orientated that way focus on making on making as absolutely as much money as you can over the next five years through better in yourself in your career. The great thing about Sydney or Melbourne is that you can live a 1,000,000 dollar life style for about $700 in rent.

And owning your own home only works if the market is consistently increasing during the time that you own it. There is nothing to guarantee that Melbourne or Sydney because it’s had 8 years of growth in the last three are going to increase in value over the next five years at all. So you would be far better off if you are not making money through your principal place of residence, renting the lifestyle you want a lead now and forgetting about buying and then investing in other areas or other states that can provide you.. say you buy one two 3 properties over the next five years that can make you let’s say make you $300,000 in equity over that five years, redrawing that equity as a larger down payment on the home that you want to own once you’re earning the income that you are able to justify that and when the marketplace is isn’t as ridiculously hot as it is now. That’s my thoughts on that.

Aussie Firebug

It is a really interesting topic. It’s funny those two markets you know, as I have said I know people in Melbourne who are trying to buy and it’s so expensive and Sydney is even worse like you said, renting just seems like such the logical choice now because you break it down into rental yield, if you rent a joint in Sydney it’s so much cheaper for you to do that like if you were to actually buy the same place that you rent your repayments would be double, triple of what you currently renting it for.

And if you just saved the difference if you’re discipline enough to save the difference between how much you pay for rent and how much your leftover savings you can clean up you can totally become a lot wealthier by renting and investing the difference then you can by over stretching yourself with this massive mortgage and having to make these huge repayments each month. I guess it’s sort of ingrained into a lot of people in Australia that your home is your castle and everyone hasn’t made it until they buy their own home. Which is properly not true, but it’s definitely an Australian mantra. I met someone once at a property conference, he was a multi millionaire, financially retired years ago and he rents, he still rents! He still rents his place of residence too, and it is exactly same thing that you said. I live in Sydney I can rent this $1.7 million apartment on the bloody waterfront or wherever it was, why would I buy a place and pay all that money repayments when I could happily rent it and live in a much better placed than if I bought.

Ben

Like I can understand psychology of people wanting to own their own home and the pressure that mum and dad’s and people in the community place on that. I tell you what, if I knew that my million-dollar house that I just bought was going double in value in seven years like it has done historically then I would be owning my own house in Sydney or Melbourne and making it work. But those old days are gone. The best you can… When I look at the numbers my properties the best I can hope for is a growth rate of 4% and if it’s not going to give me at least 4% I won’t invest. I think anything above 4% vote these days is definitely cherry on top of the cake because I don’t think need a 400,000 or place leveraged to increase in value by 10% every year like you did $100,000 how house because you’re still getting the same dollar for dollar return out of it.

Aussie Firebug

It’s funny because you would probably be of similar age, in terms of property life cycles. Have you ever seen a major crash in Australian property because I haven’t since I’ve been alive, my parents may have, but I don’t think there’s been one for a long long time, they have had that massive surge between 2001 to 2004 2005 and then it slowly slowly increase and then Sydney’s gone bananas in the last couple of years it’s almost you know due for a bit of flat line or a bit of a decline some would think?

Ben

Well Sydney market was in correction from 2005 basically through to 2013 and I suppose Brisbane sat flat for five years Gold Coast sat flat for nine years, Melbourne’s consistently sort of ticked along. All the markets have done what people projected they would do, there is no way that the sort of growth that they saw between 2001 to 2003/04/05 will occur again like it’s almost impossible for that to occur again. That’s why I’m so into that manufactured growth and having multiple strategies on properties and options now. Because the old days of just hoping you are going to make 100 grand on a property are over unless you’ve got a huge amount of time which I don’t think any young person really wants to wait 30 or 40 years before they retire these days.

Aussie Firebug

Australia was pretty much largely unaffected by the global financial crisis in 2008. I don’t know you’ve watched the movie, there was a new movie it just came out it’s basically about that financial crisis and a whole bunch of blokes betting against that. I’m trying to think, it’s… The name escapes me.

Ben

Is it the one with Brad Pitt in it?

Aussie Firebug

Yes that’s the one

Ben

Yeah I haven’t watched it

Aussie Firebug

Yet it’s a really good movie. But it’s really scary. Their property market just went completely underwater, like it wasn’t exactly the same as Australia. I invest in property myself and do you, does anything like that scare you or does anything like that come on your radar in Australia that you worry about that?

Ben

Is the movies called the big Short is that the one?

Aussie Firebug

Yes that’s the one! did you just Google That?

Ben

Yes I did ha ha ha. I’m constantly driven by risk and fear from the upbringing I had I still am always preparing for a rainy day I suppose. The way that I prepare is to overcapitalise for example a revenue stream in my business that is recession proof which is a property management business. So you’re going to have your high sales value which is the business I’m into which is buying agency but than you can buffer that with let’s say a million-dollar property management business that regardless of what happens in the world people are still going to need to rent and maybe rent will decrease by 50 bucks a week but you’re still going to get your 7% eveyr single week for the year for those properties.

I’m always concerned with that as well, like if I can’t manufactured growth into my portfolio, if my LVR is ever below 70% and I’m seriously concerned and won’t proceed with that property at that time. I’ve seen a global financial crisis I’ve brought five properties. I bought in Sydney a property which was 20% below which what the same property was worth 12 months before so there was a slight correction in Sydney. You know I read about the stuff that happened in Japan for example they lost over 50% overnight and their economy was as stable as Australia and that sort of stuff scares the shit out of me. It’s all about trying to create an income stream that generates income regardless of the marketplace. So that when things happen, and they will, you’re in a position to capitalise on that you’ve got cash funds and liquid funds that you can go out and buy the distressed assets that other people need to move. I look at something like a GFC now as an amazing opportunity. Where five years ago I would have been seriously concerned about it. I, like every investor, look forward to those opportunities where I can pick up distressed assets.

Aussie Firebug

It’s like what Warren Buffett says, be greedy when people are fearful and fearful when people are greedy. I think that was a famous quote or something along those lines and it’s definitely true. Only a few people know what I’m trying to do you know, I’ve got three properties myself. There are two people and I find I come across, one of them is supportive and want you to succeed and are all for it, but I just find that there’s a lot of people that are just Doomsdayer’s. People who have absolutely no idea about property and who have never invested in a single property in their entire lives and then suddenly they are telling me how just made the biggest mistake of my life. Just naysayer s. Did you ever come across those on your journey and how did you deal with them?

Ben

Yes absolutely and it’s really sad because most of those people were good friends and most of the people in my life still think I’m ridiculous and crazy but now they seem in living on waterfront house without having to work now like maybe if I did stay along for the journey. They have kind of come back around and gone Ok dude what are you actually doing because I’m on the train commuting two hours every day to work and you’re sitting in your house and… I don’t mean to be a dickhead and sound like an arrogant person but the difference is I made choices from about four years ago based on happiness and what was on in-line with my value system when a lot of people in my life make choices based on fear. With a lot of those naysayer’ s, I think about this a lot, I think as you begin to… I don’t know you could call it vibrating on a different frequency or getting yourself in a different mental head-space, like you’re going to attract hundreds of thousands of amazing people to this POD cast over time and your community will become people that are just like you. When I started my journey I had a goal for eight years which was to sit down with five people worth between one and $50 million per week and to sit with them for an hour and interview them and learn and try to find a pattern and it’s very simple what the pattern is and it’s about replicating that.

Aussie Firebug

And I think as while you have to take a risk to get somewhere in life like if it was easy everyone would be doing it so it doesn’t matter what you’re doing. Even if you put savings into a savings account to earn money through interest that’s a very small risk but it still a risk. It slightly annoys me when people have a go at something and that so many people around that are trying to pull them down, you see it all the time not even in investing but also in sports, tall poppy syndrome. Like you said I guess you just have to focus where you want to be, make the plan and just go for it and hey if it doesn’t work out it doesn’t work out. I’m sure this can be bumps along the road but at least you can say you had a go. Even if you fail, even of it all comes crashing down you can say that you had a crack and you’re not going to…

Ben

I think you know the one thing you have is the skill set to rebuild it. If it all comes crashing down and you don’t have the skills to get back on your feet that’s where you see these poor people with marginalised loans that end up on the pension.

When you talk about risk it’s really funny because I used to think about risk as buying a $400,000 property now I see risk as not making that decision because I see that the long-term impact of what not achieving financial independence does and that is less time doing things you love that means less time with your family that means less time doing you know things that you’re passionate about less time contributing to the world. Money comes and it goes, you notice that the people that spend the most time focusing on money are the people that have the least. The people that have the money are pretty happy with everything sort of just it’s really weird that I suppose just been in flow with money and also having the skill set to make it and it is a skill set it’s not something that anyone’s born with unless you come from a family that is worth over $15 million and it’s then brought up to you through family.

Aussie Firebug

Yeah absolutely and I could agree with you any more. When I was younger you think that the guy with the flashy car or the guy that dresses really well they are the ones that are wealthy. But when I got older all my friends whose parents that I know do really well who have businesses in everything, they’re wearing 10-year-old trackies and the driving just normal cars, like what’s going on here? Movies have lied to me my whole life and everything I thought about rich people has been the opposite. Have you ever read the millionaire next door?

Ben

I have actually and that’s an awesome book as well.

Aussie Firebug

Yeah it’s so true though. The people that have to have the latest Mercedes-Benz every year they don’t own any growth assets some of them do. But I know a lot of people in my life that have the latest car and the latest this and the latest that but they don’t actually own anything, they’re not actually wealthy. They have all the latest toys and gadgets and stuff. It’s almost like their living… not a lie. But their portraying themselves as something that they’re not. Because the really wealthy don’t need to do that and half the time they are very simple people and they porbably spend less than most people spend on themselves.

Ben

I don’t think I’ve ever met someone with serious money that cares about too much of things like that. Because most people that have got money realise that those things aren’t what make you happy. Relationships, contributions, doing things you’re passionate about and fulfilling whatever it is you want to do with the world makes me happy personally. I’ve talked to you know, I get to speak to a lot of people and I would say like the high income earners that are earning wages between 200 to 500 grand per year and I probably speak to about 30 of them a month through our business are the ones that may own one property that have the most personal debt, that have the most car debts, that have the most credit card debts. Whether they are earning 80 grand or 500 K a year they still spend that. And their friends think they are absolutely killing that and I look at those people and go why the hell didn’t you retire 5 to 10 years ago and what are you still doing working? And they’re complaining about their job and they could have a way out of that job within two years if they were smart.

Aussie Firebug

That’s crazy. Time is just about wrapping up so my final question to you is if you had to start again let’s rewind back to when you are 19, the stars are aligning in Europe. You’re sitting there in front of the Eiffel tower. What would you do differently knowing what you know now to reach financial independence as quickly as possible?

Ben

I would have not gone to university I would have gone and got a job straight away in real estate and I would become a property investor from that exact moment. The other thing that I would have done is to have the belief in myself that I didn’t need the approval and I didn’t need all these skills that I thought I needed and that I already have those to do what I need to do. Like all that stuff in already in you already like every single person has got unique ability and anything you need to learn along the way you can. Like to have just taken the plunge earlier like I probably would have been ready to start the business five years earlier like but I just didn’t have the confidence and I had all these expectations and limiting beliefs that was stopping me from doing what I was really meant to be doing which is what I’m doing with my life now. Jumping into property straight away and having belief in myself would have been the two biggest things.

Aussie Firebug

That seems to be a common theme with a lot of successful people and businessmen and investors. I wish I had done it years earlier. I think the guy that started KFC in America, he started that franchised at 60 or 65 I think. He has a quote that says, why didn’t I do this 30 years ago! That’s is crazy. I’m sure that a lot of people that are successful that have the same regret, but hey you’re super young so it’s not like you miss the boat by that much. It’s certainly something I think of. You just have to do it, you have to have a go at something because you don’t want to be nearing 60 and having to rely on retiring on the super and have in the back your heard what if I tried something and why didn’t I do it sooner.

Thank you so much than for being on the pod casts and I wish you all the best in the future I hopefully see you again soon.

Ben

Thank you so much and I really appreciate the time and I’m so excited for what you’re trying to do and I can’t wait to continue to listen in and see who else you get to interview.

Photo credit: Colleen AF Venable via Foter.com / CC BY-SA

by Aussie Firebug | Dec 24, 2015 | Mindset, Real Estate

Lets talks about Melbourne and Sydney Real Estate for a second because it pops up in my life at least once a week.

I have a lot of friends renting in Melbourne who are at the age now that they are starting to look at buying a house.

They look around and quickly discover that the prices are outrageous. The median price for a house is Melbourne is well over $700K! Using the common 25% rule for a deposit and closing costs, this would mean that my mates would have to fork out $175K to buy one of those bad boys… That’s a LOT of money to depart with.

As you can imagine, there are plenty of people who can’t afford these prices and they are crying out for something to change. But can something really be done here?

I don’t think anyone can honestly say that prices in Melbourne and Sydney are affordable to the middle class. You either have to be a high income earner or wealthy to buy in these cities.

Sure, the average working class family could take out a huge mortgage but they would be a slave to debt for the rest of their life most likely.

So what’s the deal?

I have been reading COUNTLESS articles and reports for years on why there is a housing bubble and how it’s going to create the mother of all corrections in 2004, 2005, 2006, 2007, 2008, 2009, 2010, 2011, 2012, 2013 ,2014, 2015, 2016.

There are a lot of theories being thrown around:

- Negative Gearing

- Capital Gains Concessions

- Foreign Buyers

- Speculative Investors

I’m not going to pretend that I know exactly why the prices are the price they are or how to bring them down to a more affordable level. But it doesn’t take much to understand the most basic and fundamental rule in economics.

Supply and Demand

It’s so stupidly simple to understand yet so many go looking for more complex answers to justify their reasoning as to why this is happening.

If there are a lot of buyers (demand) and there is only so much land/property available (supply) the price for the land/property soars. And the same can be said if you switch it around. What do you think would happen this very weekend at auctions if no one turned up? The prices would plummet. No doubt about it. If there are less buyers than sellers the price of real estate goes down. This is proven economics 101.

So the question people need to be asking is not how the government can stop the buyers (demand), it should be about how they can free up the land (supply).

Carve it in stone, demand for Melbourne and Sydney real estate will NEVER cease for as long as I live. It would have to take such a colossal implosion of Australia for these two cities to suck. Not completely out of the question, but I will eat my shoe if there is EVER a time where you can’t sell real estate in either Melbourne or Sydney.

They are world class cities. Melbourne was ranked the NUMBER 1 most livable city in the entire world last year and if memory serves me correctly it has been number 1 or 2 for a few years running. Sydney is no slouch either coming in at number 7. I just want to highlight this point because it’s important. If you’re trying to buy a house in Melbourne you are trying to buy real estate in THE MOST LIVABLE CITY IN THE WORLD! The world… not just little old Oz. The entire planet.

What do you think this does to Melbourne and Sydney real estate when they are some of the best places to live in on the planet?

Demand goes through the roof.

You have got to be realistic here. You are trying to compete with not only Australians but the rest of the world when you buy. Throw in limited supply and you have a recipe for exuberant house prices.

I don’t see any measure the government can put in place to stop demand enough for the prices to go back to an affordable level.

The focus is always on the demand, but little gets said about the supply.

Is it unreasonable to assume that if municipalities changed zoning and planning laws and released more land to pave the way for new development that this could potentially deflate some of the house prices? To me it makes sense. If you increase the supply in the market, the current supply will be worth slightly less.

The truth is I don’t really know (no one does), but I’m a realistic person. And when I look at Sydney and Melbourne I don’t see the demand slowing, in fact, with population forecasted to more than double by 2060, if anything, I see demand rising.

If the supply cannot keep up with the demand then it’s only going to get worse.

There may be a correction around the corner, I think there should be. But I doubt that Melbourne/Sydney real estate will ever be cheap, EVER!

Photo credit: szeke via Foter.com / CC BY-NC-SA

Photo credit: CAr Photographies via Foter.com / CC BY-NC-SA