by Aussie Firebug | Jan 7, 2024 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

As a relatively new father of three months now, I feel compelled to write about a device that has significantly improved the well-being of both my wife and me.

And I promise I’m in no way, shape, or form affiliated with the company selling this product.

The greatest invention of the 21st century

The bad boy pictured above is called a SNOO, and it’s basically a smart device for your little bambino.

This thing is crazy:

- It has 4 different levels of ‘rocking’, which helps soothe your baby to sleep.

- It has a microphone to detect if your baby is crying (which can then increase the levels up or down depending on what pre-made settings you have assigned in the app).

- It has a speaker for white noise and a ‘hushing’ sound if your baby starts to get upset.

- The app tracks your baby’s sleeping patterns, which apparently is useful if you want to sleep train (we haven’t got this far yet)

But most importantly, it helps you and your partner get better sleep for the first 6 months, which is invaluable.

We got our SNOO second-hand for $800, which might sound like a lot of money (and it is), but good God, that sum seems laughably low compared to the value it has brought us.

Picture this:

It’s 4:30 AM, and you have been jolted awake by your baby’s cries.

You’re smack bang in the middle of some REM goodness and so tired you could nearly throw up. You’re just about to flick the covers off and rock your baby back to sleep when you hear the SNOO’s responsive rocking motion kick it up a notch and start soothing your baby.

You give it a minute or two, and, to your absolute astonishment, your baby goes back to sleep, and you get another glorious sleep cycle.

🙌

Words can’t explain how glad I am that we set ourselves up before having kids. Now, spending nearly $1,000 on a device like this doesn’t cost me a wink of sleep. I would have never done that in my 20’s and it gives me anxiety to think I would have forgone such a great innovation for the sake of getting ahead financially.

The SNOO has been a godsend for us so far, but I’ve also read that it bites you in the ass when you have to take it away… but I’ll take 6 months of sleep and then deal with the consequences any day of the week.

Good luck, future Firebug 😅

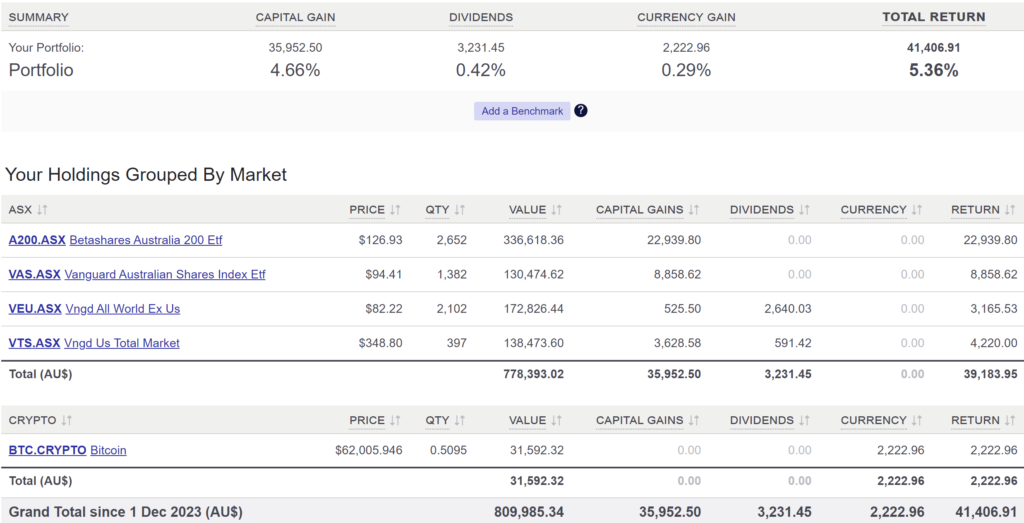

Net Worth Update

Santa came early for us share market investor in December.

A huge month for all asset classes to boost our NW to a record high of $1,283,257.

| Years End |

Net Worth |

| 2021 |

$1,038,417 |

| 2022 |

$1,171,120 |

| 2023 |

$1,283,257 |

We started 2023 at $1,149,655, which means we increased our net worth by $133,602 during the year.

But here’s the astonishing thing… we didn’t make any investments throughout the year, and we spent all of our dividends!

Yeah yeah yeah, I know 2023 was an exceptional year, but still.

The power of compounding is crazy!

We spent all our investment income, took two trips abroad, had a baby, didn’t work for six months, made no new investments, and yet our net worth still grew by over $130K — absolutely mind-blowing! 🤯

For anyone reading this who might be just beginning their journey, I have one message for you:

Keep going.

The snowball is so bloody hard to get going. But once it’s rolling, it gets easier and easier. And you get to a point where it feels like you’re playing this money game on easy mode.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

A pretty normal month spending-wise.

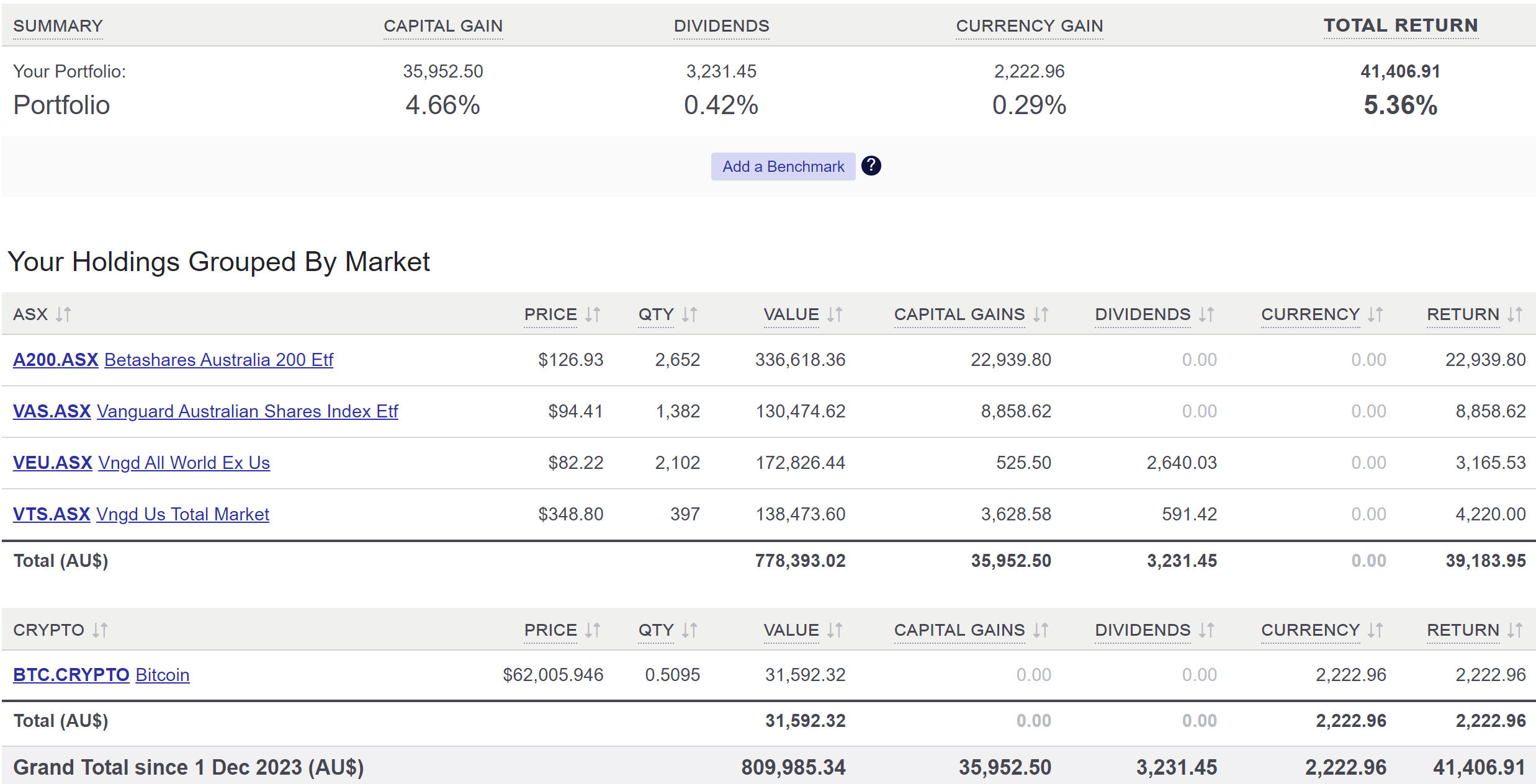

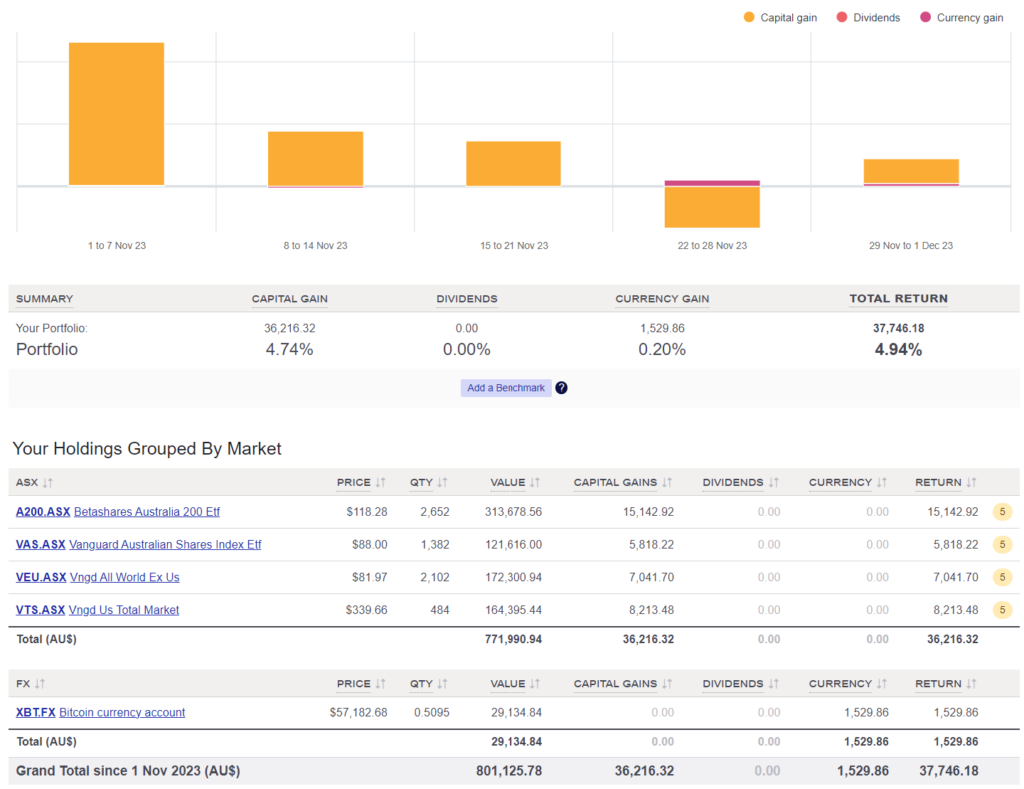

Shares

The above graph was created by Sharesight

For the first time ever, we sold a significant amount of shares in December.

We sold $30K worth of VTS to help seed our co-working dream.

We opted for VTS as it had become the most out-weighted holding compared to VEU.

I didn’t want to sell any of our Australian shares (A200 and VAS) because they will naturally decrease in weight over time as they typically distribute larger dividends.

Mentally, I struggled with the decision to sell such a significant number of shares, but I had to keep reminding myself what was actually important.

Do I care more about missing out on market gains, or is it more important to me to chase a dream?

Given that my family and I are in a comfortable financial position, I believe the above question is rhetorical.

The $30K is going to be used to help set up our space with furniture, management software and security management.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Dec 21, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

We secured the lease for our co-working dream in November 🥳.

Our new Co-working space

This was the first step towards our goal of creating a community-focused shared environment for small business owners and entrepreneurs.

There are so many unknowns when you start a venture like this one.

- What’s the demand?

- How much do you charge?

- What are the ongoing costs?

- What type of permits do you need?

I thought adjusting to life without the stability and assurance of a full-time job was challenging enough. However, pouring money into such an unknown project tops it.

But here’s the rub: it’s so bloody exciting!

There’s a profound sense of fulfilment that comes from being in charge of your own destiny.

I’ve also noticed something very interesting when discussing this idea with friends and family. People love to point out all the things that can go wrong and rarely see the potential upside.

And it’s not like they are doing it deliberatively to be nasty. There seems to be an inherent truth about humans: our operating system is wired more to avoid losses than to actively seek gains.

Many people are comfortable remaining in their 9-5 jobs, contributing to their boss’s dreams, rather than taking the leap to pursue and build their own.

That’s not to say there’s anything wrong with the old 9-5. But I do wonder how many kick-ass products/services have remained unrealised because those capable of starting them were too risk-averse to take the plunge.

FIRE has given us the financial courage to give this a go without worrying about my family suffering if it fails.

And even if we do fail, the satisfaction of having a crack will remain. In the end, it’s the effort and the journey that counts.

Net Worth Update

Wowee!

What a huge month for our portfolio, Super and BTC.

This is coming off a three-month slide that saw our net worth decrease by over $76k!

That encapsulates the essence of the volatility game in the stock market. It’s the reason we earn the returns we do as investors. Not everyone can withstand these fluctuations, and those who can are rewarded accordingly.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Booking another Bali holiday for next year saw a spike in our spending in November.

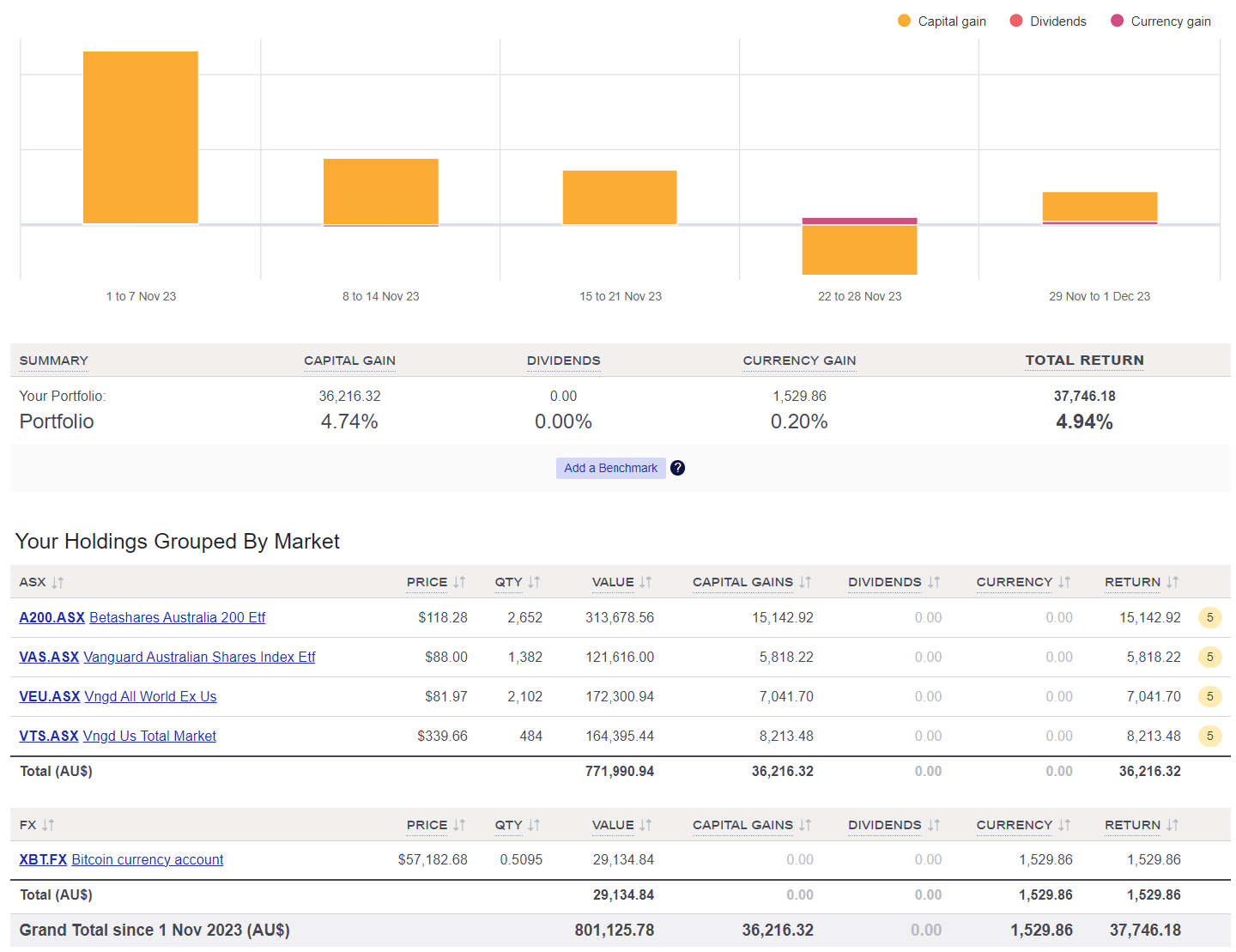

Shares

The above graph was created by Sharesight

It seemed like the entire world was on an absolute tear in November.

VTS has a whopping 5.26% gain in a single month followed by our Aussie shares (~5.05%) and then VEU (4.26%).

BTC continues to climb up and up increasing in value by 6.04%.

We made no purchases in November.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Adam Preston | Dec 18, 2023 | Podcast

Summary

Today, my guest is fellow FIRE enthusiast/podcaster/blogger, Captain FI!

He’s actually been on the podcast before but I had to take that episode down due to ASIC’s 2022 guidelines.

Cap came and stayed at the Firebug household after attending the Rask event in my hometown. It was a lot of fun meeting and greeting others from the FIRE community and it was extra special to do so in my own backyard.

This was very much an improv podcast and I didn’t have any set questions.

We had a general chitchat about Captian Fi’s financial journey and other topics relating to FIRE.

Some of the topics we cover in today’s episode are:

- Who is Captain FI? (00:02:36)

- Investing a big lump sum into the share market (00:04:47)

- Finding a financial planner (00:16:01)

- Investing psychology (00:26:24)

- Reaching financial independence (00:41:26)

- Does your FI number include a paid-off house? (00:43:43)

- Selling shares to pay your living expenses (00:45:46)

- The psychology of spending (00:52:26)

Links

by Adam Preston | Dec 11, 2023 | Podcast

Summary

Today, my guest is none other than my accountant, Clayton!

Clayton and I have talked about doing this podcast for a while. I pay him thousands of dollars each year to help with tax planning, structuring our investments and businesses and other strategic decisions that ultimately help me reach FIRE sooner.

I thought it would be interesting to chat to him about what role an accountant can play when someone is trying to reach FIRE, and explore why certain decisions were recommended for our family in terms of tax advice and planning.

Some of the topics we cover in today’s episode are:

- The difference between an accountant, a tax advisor and a financial planner (00:05:36)

- The role an account can play in someone’s journey to financial independence? (00:09:08)

- Common financial structures for people wanting to improve their situation (00:11:56)

- Some of the advantages of a financial trust structure (00:14:13)

- The difference between tax minimisation and tax evasion (00:16:52)

- How can people get the most out of their accountant? (00:22:30)

- Easy things you can do to help you at tax time (00:26:58)

- How do you find a good accountant who’ll work with you to build wealth? (00:34:33)

- What are the main things to consider when starting a sole trader/freelancer business? (00:36:54)

- How often does the ATO actually audit people? (00:49:10)

Links

by Aussie Firebug | Nov 19, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

My second month of dad life has been going great.

Yes, there are times when getting enough sleep can be difficult. But boy oh boy it’s all worth it when you see your little one’s adorable smile 🙂

I’m not kidding; it’s like black magic. I’m pretty sure evolution has developed this way to give parents an additional gear they can tap into when things get hard haha.

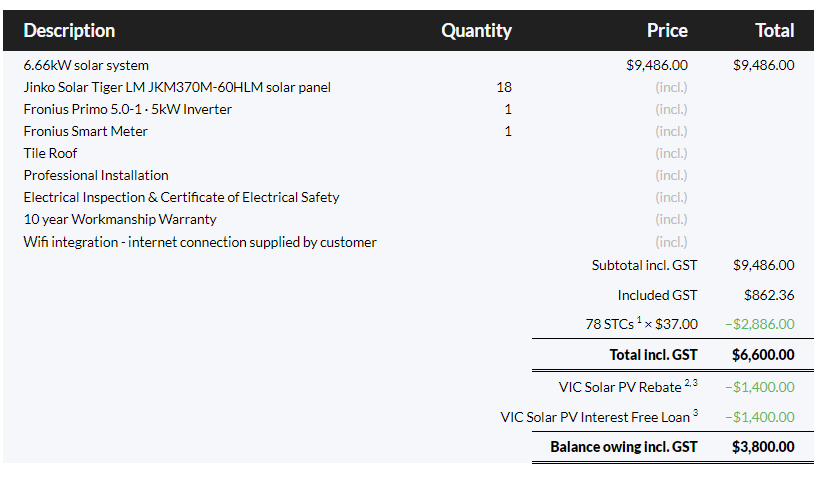

As a data nerd, I’ve been looking forward to seeing how much more electricity we would use when the baby arrives. This was one of my biggest motivators for installing our 6.66 kW solar system in October 2021.

Our out-of-pocket cost for that system was $3,800.

Solar Install

Our usage comparing October last year to October this year has been the following:

| Month |

Grid usage |

Consumed directly from solar |

Total Usage |

Self-sufficiency |

$ Saved (based on 39c/kWh) |

| 22-Oct |

115 kWh |

102 kWh |

217 kWh |

47% |

$40 |

| 23-Oct |

153 kWh |

151 kWh |

304 kWh |

50% |

$59 |

Since the three of us are home most days, our energy usage has increased by over 40%. And I suspect this will only increase as our baby grows up.

The other significant factor is we will be buying an electric car next year (trying to hold out until the new model Y drops). Our solar panel energy consumption will skyrocket from that point onwards and the payback period will significantly speed up.

It’s going to be cool to calculate how much our panels save us in a few years and compare that to how much we would have received if we invested it instead.

Net Worth Update

Another brutal month with our shares and Super being hit the hardest.

On a positive note, Bitcoin increased by 30% in October!

I haven’t used my Bitcoin yet, but I’m interested in finding out where I can spend it. Does anyone know of any cafes or stores in Melbourne that accept BTC or are on the lightning network? I’m curious to see how easy the process will be.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

Another quiet month on the expense front. We’re really not spending a lot of money at the moment.

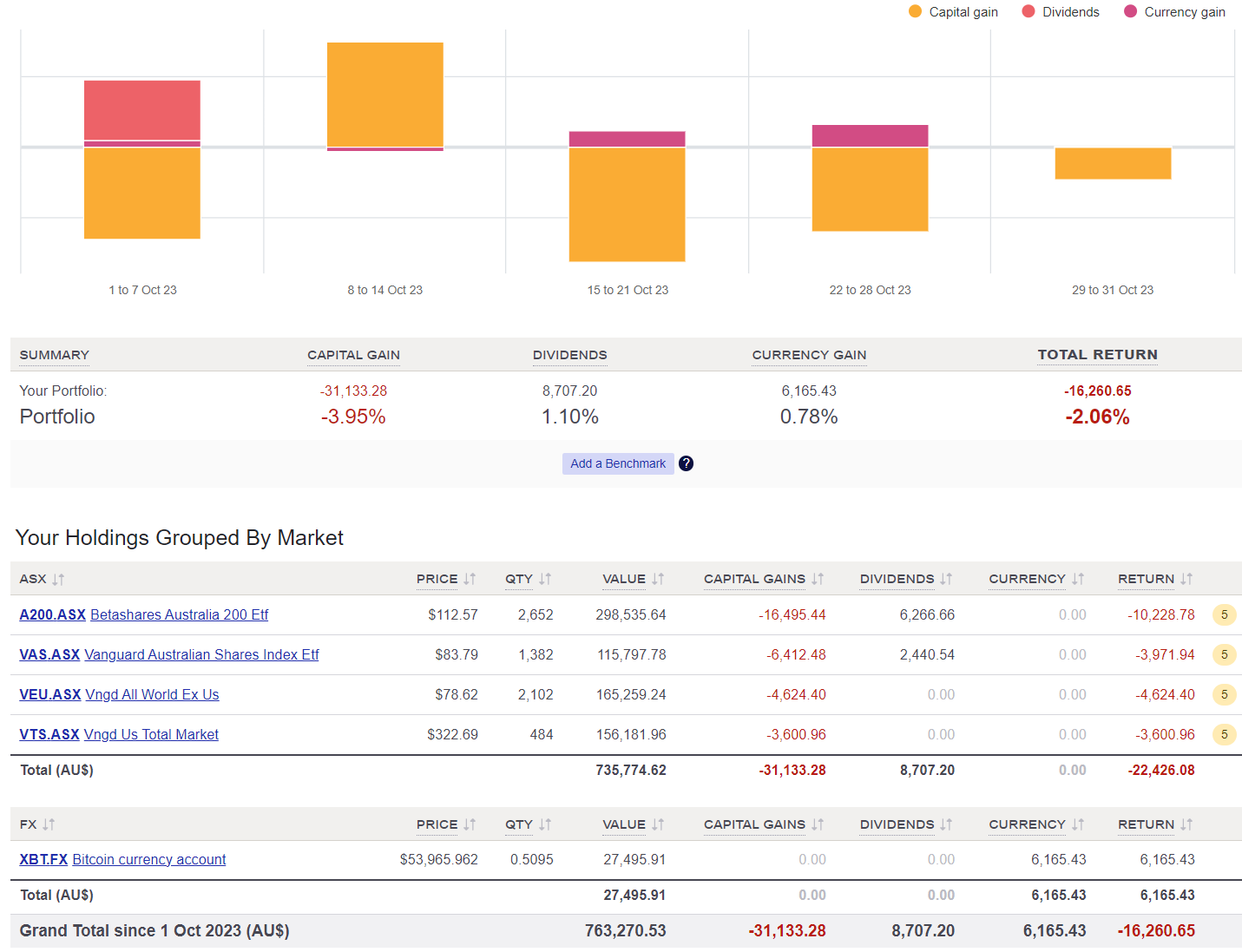

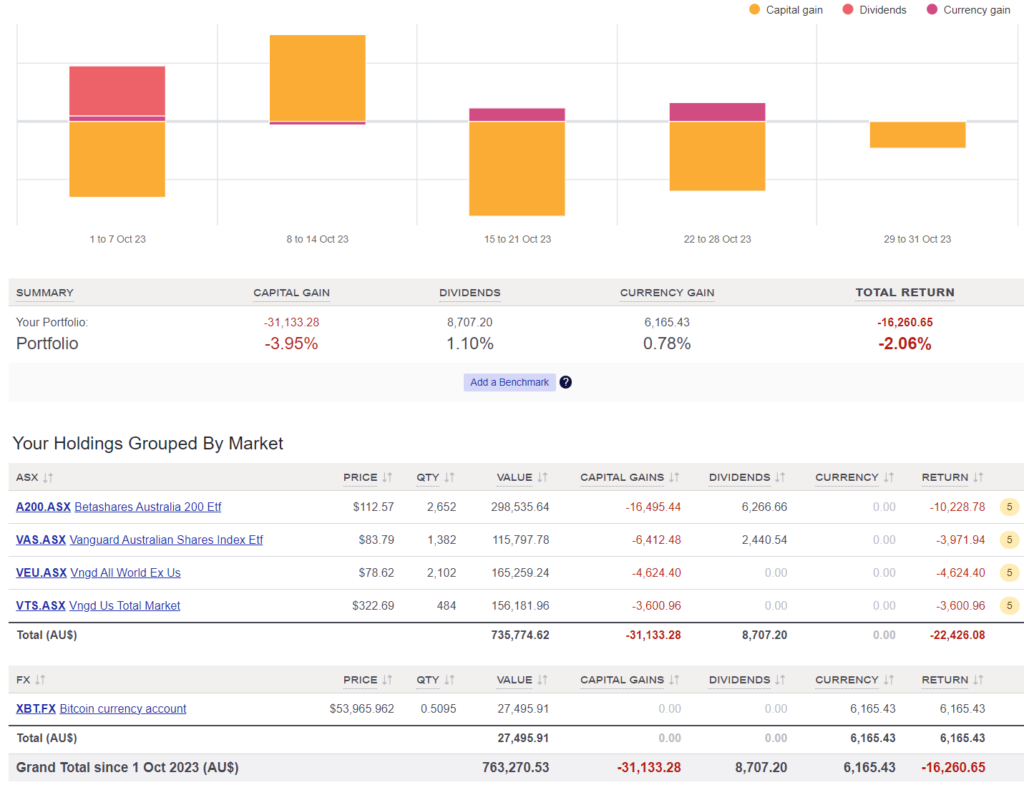

Shares

Monthly Performance

The above graph was created by Sharesight

$8.7K in dividends slightly softens this bad month from a psychological point of view, but still, not great.

We made no purchases in October. We are still keeping our cash position high until I secure some contracts that will be landing in the coming months.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth