by Aussie Firebug | Oct 21, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

Not a lot to report for this month so I’ll just be posting the basics.

Net Worth Update

Ouch!

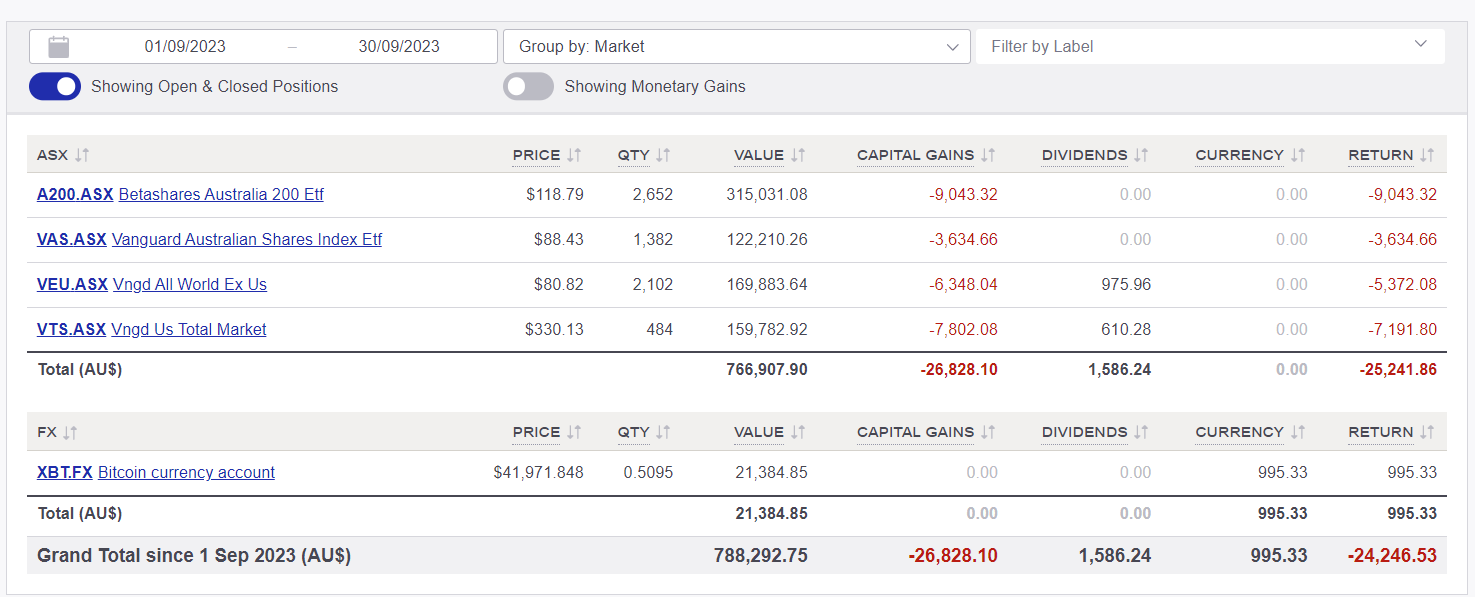

The markets hammered our portfolio in August with Share and Super being hit the hardest.

Honestly, I’ve been quite occupied throughout August, so I haven’t been keeping a close eye on things. Nevertheless, as we begin to withdraw from our portfolio, these somewhat significant downward swings are stinging a bit more.

All good though. My business signed another client in August, so there should be a big PO coming my way in the coming months.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

We hardly left the house in August which was reflected in our low expenses.

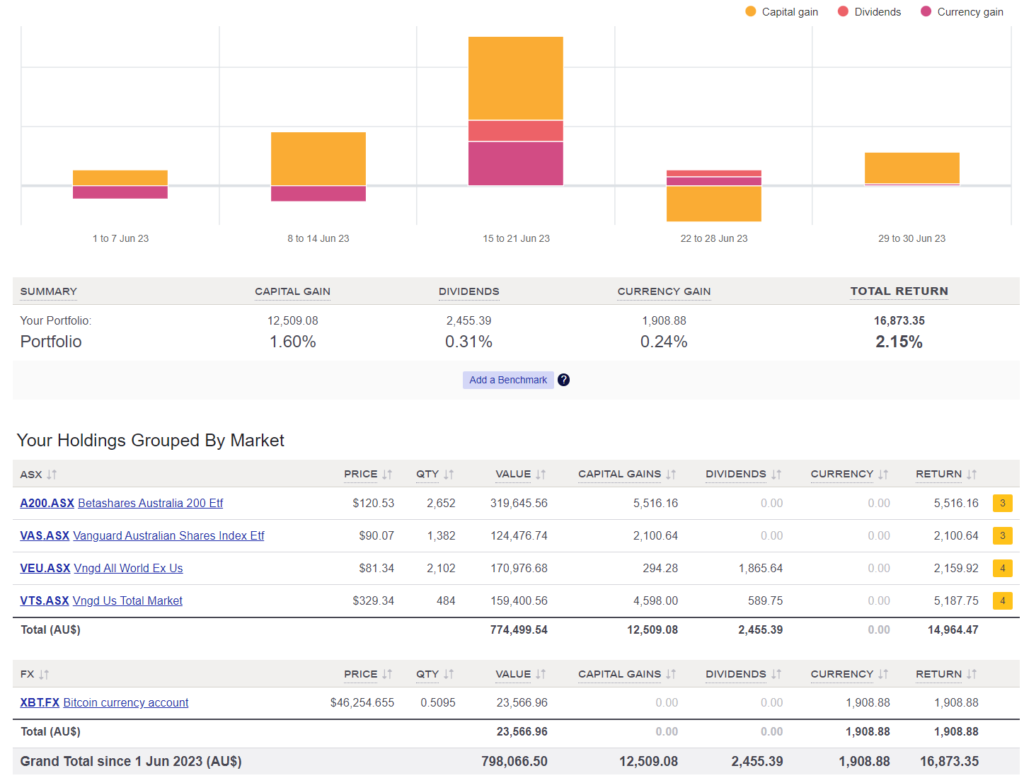

Shares

The above graph was created by Sharesight

Once we get the $$$ from the upcoming PO, I might consider buying more shares, although I find myself leaning towards reinvesting the funds back into the business. Both options are quite tempting.

Growing the business seems way more fun, though haha.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Sep 16, 2023 | Net Worth

I share these net worth updates to stay accountable, seek feedback on our strategy, and prove that achieving financial independence in Australia is feasible without relying on extraordinary luck or wealth. The table below tracks our journey from $36K in debt to reaching our goals. 🔥

I’ve said it before, and I’ll say it again.

As much as I love online communities, nothing beats in-person gatherings with like-minded people.

Which is why it was so awesome to have the guys from the Rask team come down to my hometown and put on a roadshow. The FIRE community in Latrobe Valley showed out, and we had a packed room filled with like-minded individuals, all enjoying a great evening together.

Ana from the GRSC podcast and Captain FI

Owen from Rask

Traralgon crowd

Ana and Emma from The Broke Generation

It was so cool to meet folks who came all the way from the other side of Melbourne to be there too. I really did my best to chat with everyone that night, but if I didn’t get to you, I’m genuinely sorry, and I hope we can catch up at the next meetup.

Shoutout to Adrian from Chartscape for creating this personalised poster that beautifully illustrates our net worth journey (with the blue graph in the background) from the very start up to our July update. It’s an awesome digital art piece, and it’s hanging up in my office mate 🙂

Net Worth Update

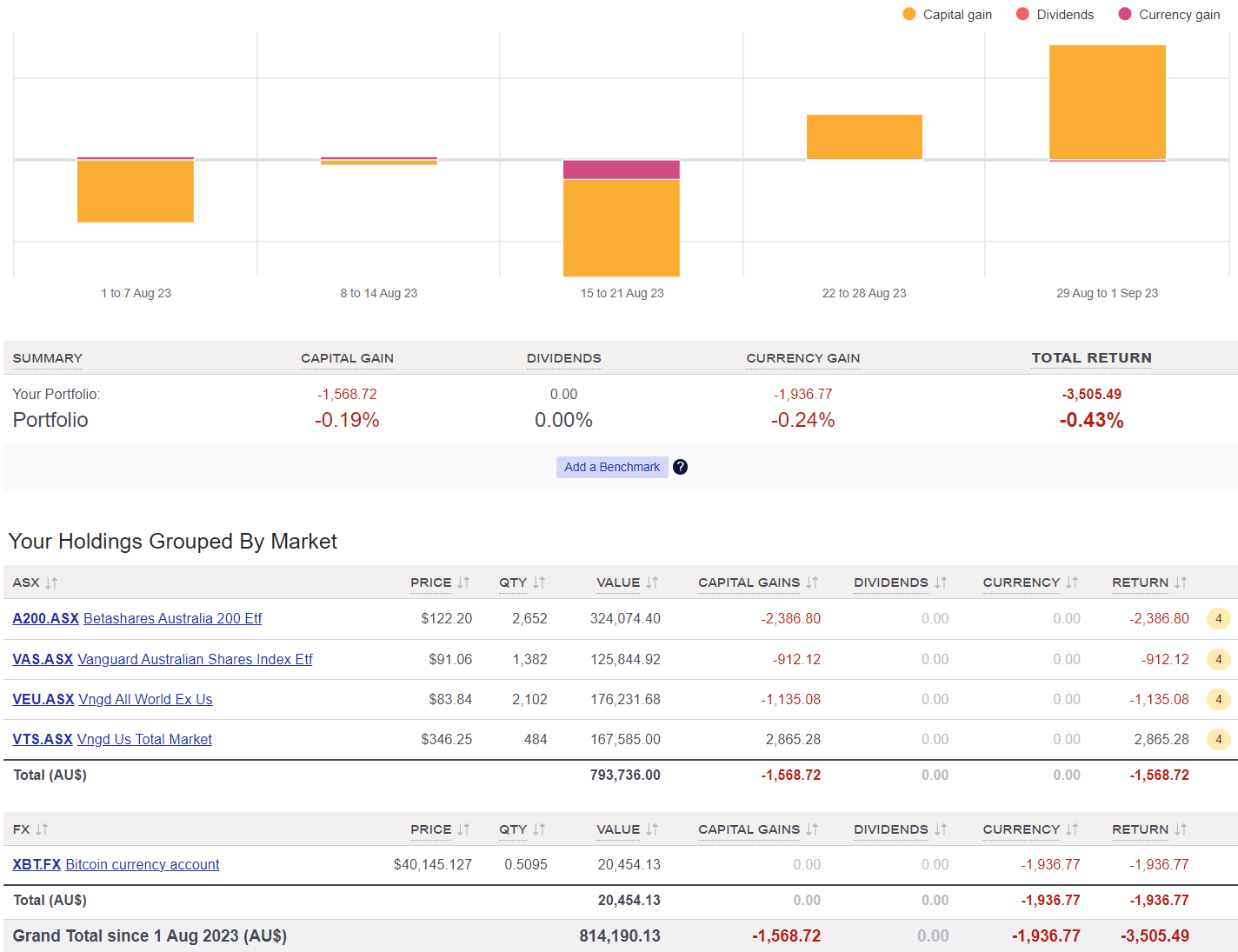

I had a big tax bill for the company, which, along with some other big expenses, was the primary factor behind the substantial loss this month.

All other asset classes went down too except for Super.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

August was a fairly typical month for us.

Shares

The above graph is created by Sharesight

We didn’t buy any shares in August.

I’m currently working on a long-overdue article. It will provide an update on our current strategy and where we stand in the grand scheme of things. You can expect it to be released before the end of the month 🙂

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any impact other than some extra accounting work once a year.

Networth

by Aussie Firebug | Aug 9, 2023 | Net Worth

I publish these net worth updates to keep us accountable, have others critique our strategy, and show that reaching financial independence in Australia is very doable without winning the lotto, having a high-paying job, or inheriting a wad of cash. The formula for retiring early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

In July, I felt fortunate to be blessed with the opportunity to work from the comfort of my home. My social side has been longing for more real-life interactions for a while now (hence my co-working space ambitions) but honestly, in the middle of winter I’m pretty content to be inside in a hoodie and moccasins 😂.

It might sound weird to some but I really enjoy going for a walk first thing in the morning when there’s still ice on the grass (my fellow Victorians will know what I’m talking about). It wakes me up and get’s the blood flowing.

During that 15-minute stroll, my mind tends to wander. On occasion, it’s focused on what I want to get done by day’s end. There are moments when my thoughts drift towards upcoming events and the future. And then there are instances when I find myself fixated on that joke I cracked that nobody laughed at 😅.

My walking shifts into autopilot mode, and since I’m mostly unable to reach for my phone or use my computer, it’s just me and my thoughts for a while. Almost like meditation, I guess.

And then there’s a different type of meditation I get when I’m at the gym. There are times at the gym when the physical demands of exercise completely occupy my mind. In those moments, my brain’s capacity for attention becomes entirely absorbed, leaving no room for any other thoughts.

I’m solely focused on lifting something heavy and placing it back down (it sounds funny when I write it out like that).

Having time to let my mind wander and time, when it’s completely focused, are both important mental exercises I need to feel centred.

In other news…

There’s only one week to go before the RASK roadshow tour in my hometown.

There’s going to be a lot of my local FIRE community joining along with other great guests and speakers.

See y’all next week 🔥

AFB x RASK Traralgon meet-up

Net Worth Update

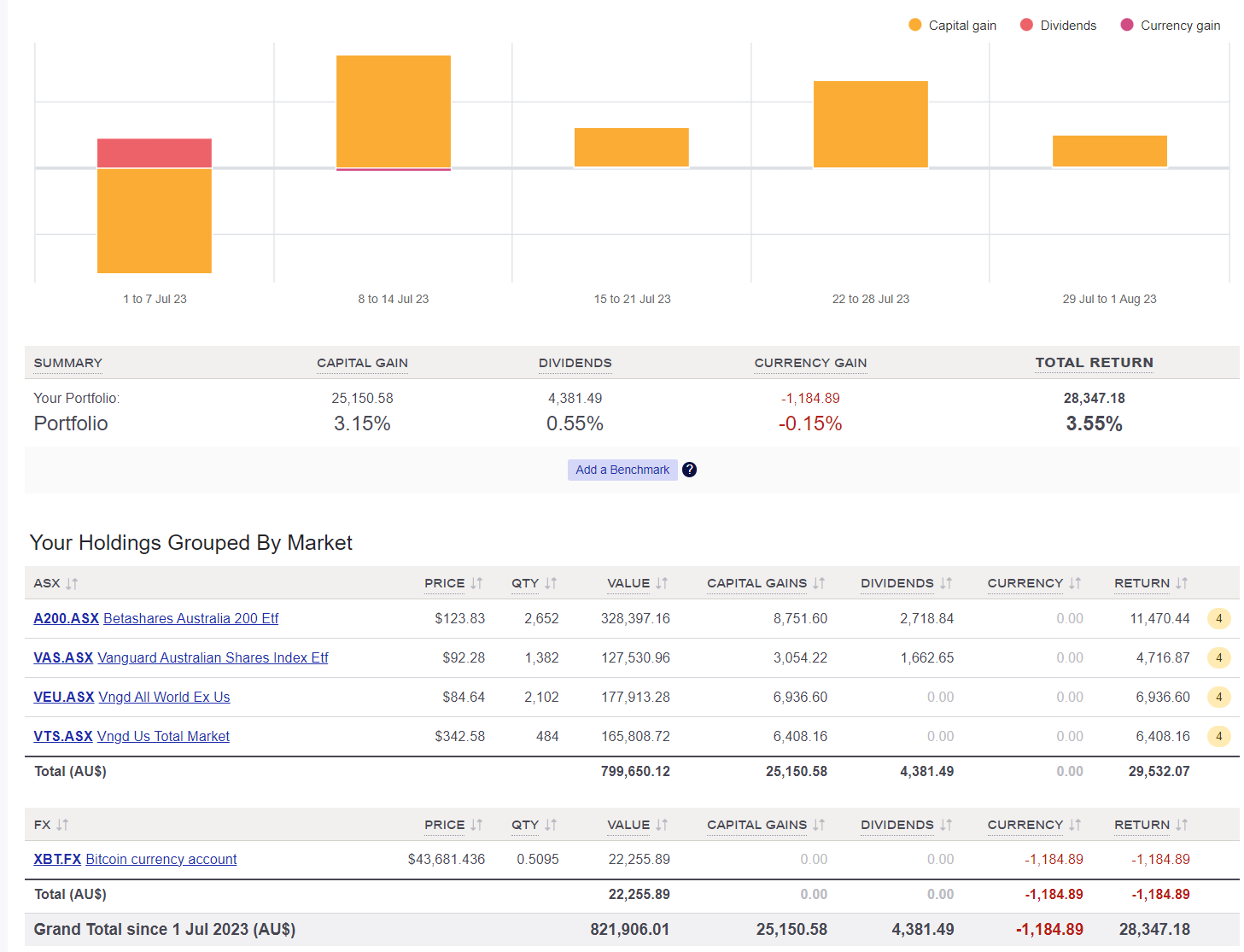

The share market did the heavy lifting in July with BTC being the only asset class that went down.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

It’s been a very, very long time since we had a sub $4K month. This is mainly because we didn’t book any future trips and just stayed home for the whole of July. It’s funny to think that $4K a month was our baseline pre-London.

Shares

The above graph is created by Sharesight

We didn’t buy any shares in July.

I’m planning to record a podcast soon to provide an update on our progress towards FIRE, as I’ve received numerous messages inquiring about it.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any other impact other than some extra accounting work once a year.

Networth

by Adam Preston | Jul 27, 2023 | Podcast

Summary

Today my guest is Carl Jensen who is better known in the FIRE community as Mr. 1500.

He’s a family guy living in Colorado with his wife and two young children and managed to retire at the ripe old age of 43.

Some of the topics we cover in today’s episode are:

- The story behind the name “Mr. 1500” (00:02:06)

- Investment philosophy and strategies (00:07:25)

- Carl’s interest in Tesla and EVs in general (00:18:44)

- Balancing frugality and fulfilment on the path to FI (00:23:49)

- The biggest benefits of achieving FI (00:26:31)

- How Carl handled the cultural challenges of pursuing early retirement (00:39:04)

- What Carl wishes he knew when he started his journey to FI (01:09:58)

Links

by Aussie Firebug | Jul 4, 2023 | Net Worth

I publish these net worth updates to keep us accountable, have others critique our strategy, and show that reaching financial independence in Australia is very doable without winning the lotto, having a high-paying job, or inheriting a wad of cash. The formula for retiring early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

We managed to squeeze in a winter escape to Bali in June.

In my July update from last year, I briefly discussed the extent of Bali’s transformation, and this recent trip only reinforced that impression.

Bali has always been the Bogan capital of the world to me. But that reputation needs serious reform.

Don’t get me wrong, you’ll still occasionally bump into the southern cross-tattooed, foul-talking drunk bogan in Kuta. But further up the coast in Legian and Seminyak lies pure paradise.

I was quite surprised to learn about its stellar reputation worldwide as well. Americans often choose to travel over 20 hours to vacation in Bali instead of opting for more “local” destinations like Mexico or the Caribbean.

Crazy!

Jimbaran Bay

During this trip, I was also on a reconnaissance mission. I have a strong desire to permanently incorporate a Southeast Asian destination into my lifestyle at some point.

In my line of work, I possess a unique superpower: the ability to perform meaningful work without being physically present. This blessing allows me to escape Victoria’s winter for a few weeks every year, all while maintaining a sense of productivity.

During a laid-back holiday like in Bali, I tend to get a bit bored. I reach my limit after a week or two of pure relaxation.

However, incorporating a few weeks of meaningful work into my stay changes that dynamic. That’s why I was eager to find a cool co-working space.

I found a place called GoWork (a rip-off of WeWorks haha) and it was awesome!

It cost me $14 AUD for the day but they have monthly rates which work out a lot cheaper.

Kudos to the interior designers responsible for this space as well. I took numerous pictures, drawing inspiration for when I eventually have the opportunity to venture into starting my own co-working space in Latrobe Valley.

Co-Working Space

In other exciting news, I’m thrilled to announce that I am finally organising a meetup for the FIRE community in my hometown of Traralgon.

The good folk at RASK are coming down as part of their roadshow tour. They’ve asked me to talk at this event and I thought it would be a great opportunity.

There are only 100 tickets available and 28 have already been sold.

You can use the code “15OFF” until this Friday to get 15% off.

AFB x RASK Traralgon meet-up

Net Worth Update

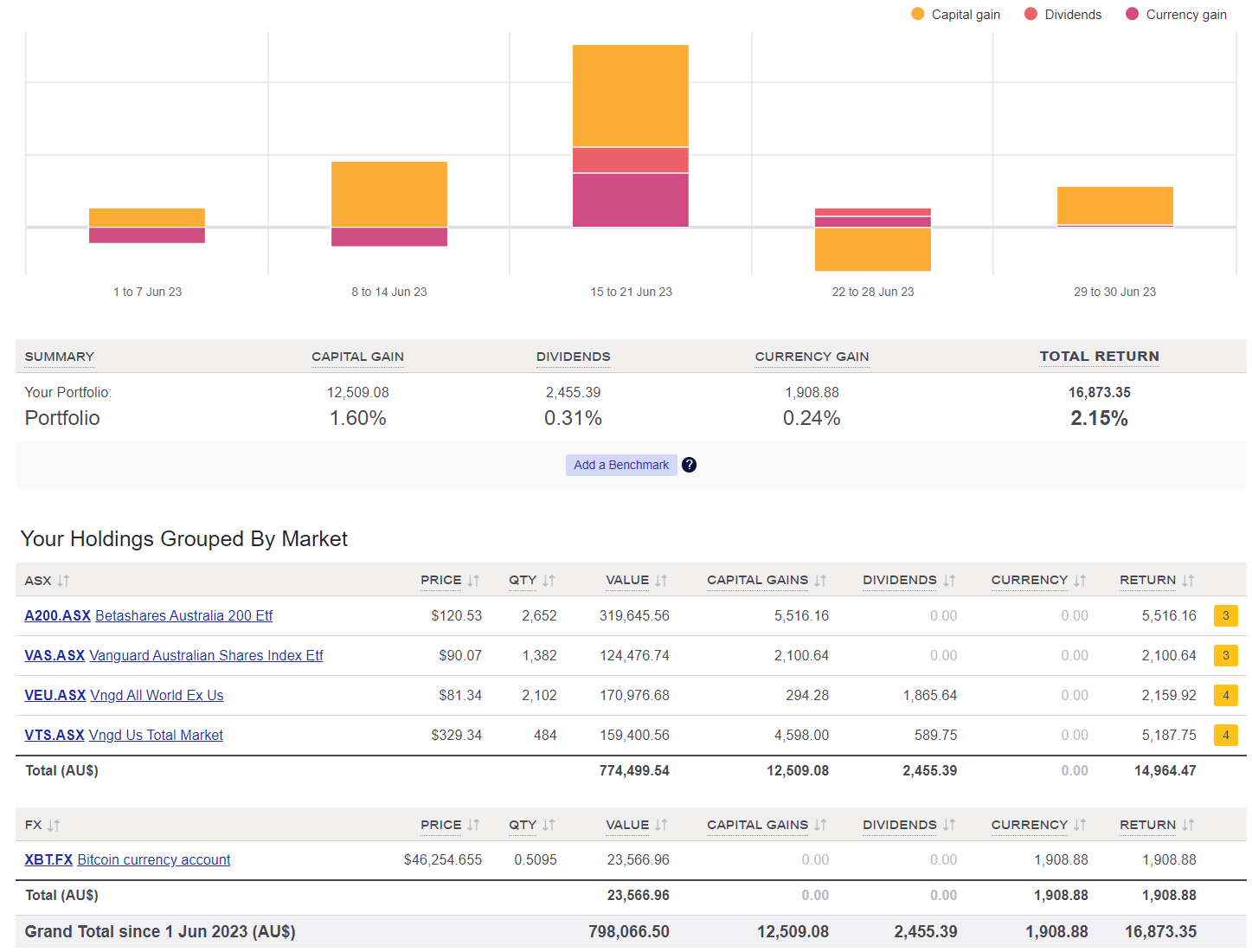

In June, everything experienced an upward trend, but the main increase came from the renewal fees for my data platform license for another year.

I license the platform on an annual basis, and it has been 12 months since my client initially signed up.

I am currently working on two promising leads, and I am hopeful of securing the next contract before the end of the year which might mean another big bump but we’ll see.

.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

The expenses during June were relatively normal, as we had already paid for the Bali trip in the preceding months.

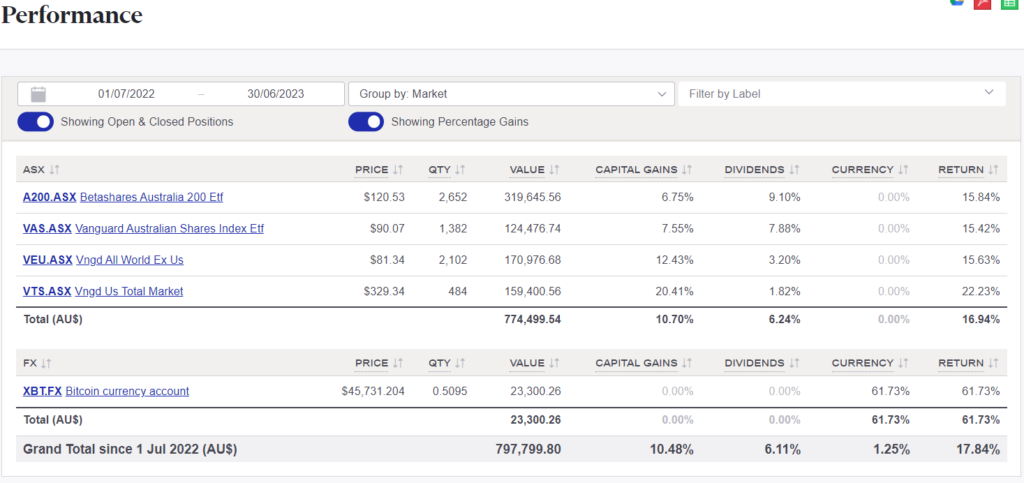

Shares

The above graph is created by Sharesight

Fantastic returns across the board!

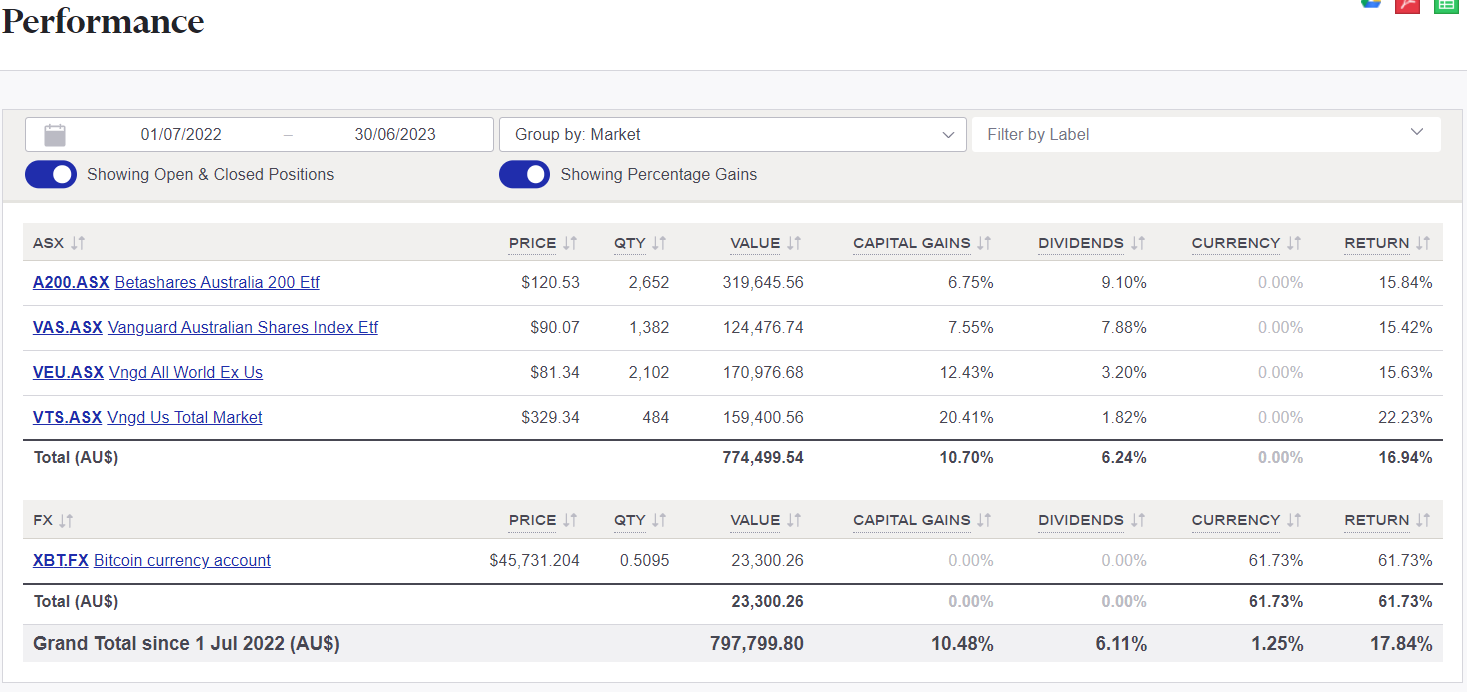

With the fiscal year now concluded, I made the decision to evaluate the performance of my portfolio over the past 12 months, and the results were surprising to me.

22/23 Performance

Nearly 17% from passive ETF’s!!!

Yeah, I know shares had a big year the previous year but still, pretty cool to see.

Question: Why do we have A200 & VAS?

Answer: We started buying A200 in August 2018 after Vanguard didn’t lower their MER to match A200. Practically speaking, A200 and VAS are almost identical so it makes sense to go with the lower MER. As an added benefit, I like the fund diversification between Vanguard and Betashares. We decided to hold both after making the switch since it doesn’t have any other impact other than some extra accounting work once a year.

Networth