March was a month of highs and lows. Mostly highs.

I was asked by the ABC to come on to their national radio program to chat about my journey towards FIRE which was pretty cool. They had a financial planner, audio snippets from someone who was in their mid 30s current enjoying early retirement and yours truly. It was pretty cool going into the studio and getting mic’d up and all that. I can’t lie, I was a bit nervous when the ‘On Air’ light came on haha.

The one question that I wish I could have answered again was when the host asked me what I had to give up to be on this journey. I tried to answer it to the best of my abilities but I sorta just stumbled through the classic stuff of not upgrading your phone and eating out all the time. What I wish I had said was “Nothing! I don’t feel like I give up anything. If I want something enough, I buy it”. And that’s honestly how I feel.

I don’t know about you, but when I discovered financial independence and realized the freedom it can grant you. My wants and needs shifted. I honestly don’t feel as though I restrict myself in the slightest. I splurged here and there but for the most of it, the things I enjoy these days don’t cost a lot of money or are free.

The other one was the whole early retirement thing. Everyone has a different idea of what early retirement actually is. I could tell the host was a bit taken back when I said I don’t plan to stop working ever. What I really mean of course is not working a 9-5 job and unplugging from the matrix of being a wage slave. Meaningful work is a staple of life and without it, I’d be miserable. Even the lady that was on the program with me hasn’t really stopped working. They just do a different type of work. She and her husband grow a lot of their food for example. This is a form of work expect is probably has a lot more meaning and satisfaction to it than sitting in front of a computer screen for 8 hours a day.

You can listen to the program HERE.

I also learned first hand that major online publications are not overly concerned about what an article is about, but mainly what headline will be catchy enough for people to click the link.

Let me explain.

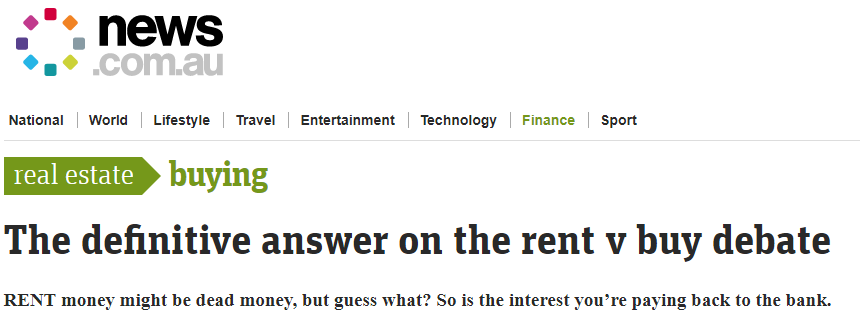

I was contacted by the commissioning editor of new.com.au because they wanted to increase their voice in the finance and money space and must have found me from the ABC radio interview. They asked if they could repost my Rent vs Buy article which I happily obliged.

I didn’t know when they were going to repost it, but I woke up one Saturday and there were something like 20 new comments throughout my blog and I was a bit confused before I realised that the article must have dropped.

First thing I noticed was the headline:

LOL. What! That’s not what the article is about.

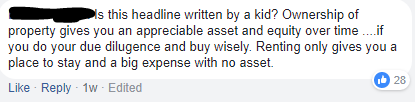

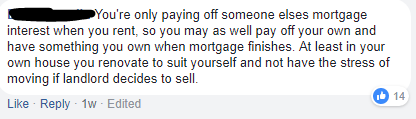

The comments that followed were also extremely amusing.

Had to laugh about headline written by a kid comment 🤣🤣🤣

You can check out the Facebook comments HERE

I lot of people also commented on the actual article here on my site. They were really getting upset about me using 2.5% as a rate of return for capital appreciation on property. I edited the article and stated a source for property only having risen 2.8% (real rate of return) during the last 30 years. But the old ‘Bricks n Mortar’ crowd was out for blood I tell ya.

I also had another publication republish the same article.

Here was the headline

Sigh.

Net Worth Update

So now we have come to the lows for March. ETFs and Super were hit pretty bad to the tune of around $6K. This plus an expensive month results in us just keeping our heads above the $400K mark.

2018 has been pretty lousy for our net worth but here’s hoping for some stronger performances in April!

Properties

No changes in the properties this month.

*DISCLAIMER*

Various data sources (RP data, Domain.com etc.) are used in combination of what similar surrounding properties were sold for to calculate an estimate. This is an official Commonwealth bank estimate and one which they use to approve loans.

ETFs

Down around $3K here. VAS got hit the worst with VEU doing the best (but still down).

Networth

People are funny, aren’t they. What a world we live in.

It’s the clickbait world we live in unfortunately

Next, they will blame you for declining property prices. 🙂

Good on you, I say. FIRE is a worthy goal. Savings enabled me to go part time in my mid 40s – and I’ve never looked back. And – interestingly – I found I actually like going to work now that it’s part time. Huh!

If only I’d been an investor though, not just a saver – still, that’s just coulda woulda shoulda… And good on you – you’ve got this investing thing sorted!

It’s good of you to share your journey, Aussie Firebug – keep going! Loved your spreadsheet too, thanks.

Thanks Sue 🙂

Real growth in Sydney property prices Is worse than 2.8%. When you account for improvements in the overall quality of housing stock, real property price growth in Sydney since 1970 averages about 2%. Net rental yields on some properties are now less than 3%, which means long term real growth prospects on such property investments are less than 5%.

Morning Firebug!

Really, thoroughly, enjoy your podcast and all things AussieFireBug.

I’ve wanted to ask you if you could do it all again, knowing what you know today would you still follow the same investment path that has gotten you to where you are today (Congrats on that btw) (i.e. 3 x IPs first then diversifying from there?)

Good questions Jack. If I could start again knowing what I know today. I would have dumped everything into bitcoin back in 2011 lol!

But seriously, I will have a better answer for you once I sell my properties. They were a lot of work, but the returns so far have been worth it. I will only know the true returns when I sell however.

Fascinating experience you’ve had with the media Aussie Firebug! Really makes me want to have nothing to do with mass media 🙂

Great summary of your net worth – still sitting pretty nicely up around the $400k mark, can’t complain too much!

Cheers, Frankie

Hi Firebug,

Love your work and have had a look at your spreadsheet. Not being of an accounting mindset, one of the things I am trying to sort out is … When you are tracking your rolling networth, how does mortgage debt get factored in? For e.g. You have rolling networth of $400000 – Is this made up of cash + share + IP values etc – (minus) mortgage debt? In other words, do you only add your current equity in your IPs to your rolling networth? If so, I guess it is easily possible to have negative rolling networth if you have a large mortgage, despite having a sizeable cash/share account.

Hi Sue,

I’m glad you’re enjoying the site 🙂

Your assumptions are correct. I only include the equity (value – debt) for the investment properties. And you’re also correct in saying that I could have negative net worth if I had a large mortgage despite having a decent portfolio of cash and shares.

When we buy a house to live in, it’s going to hit our net worth hard. Because I don’t include a PPOR in net worth calculations.

I hope that answers your question.

Morning firebug! I love what you are doing and have achieved – especially espousing ETFs. I too have ‘found the light’ with index and ETFs. Unfortunately, it took a few years of being ripped off by financial advisors and the bank’s vertical integration and commission model, but it did force me to investigate alternatives. Being mid-40s and having a mortgage, (which is really quite small now), I may have missed the boat as far as FIRE goes. But hey, isn’t 50 the new 40?

I’d be interested in your opinion about Acorns – now Raiz – as another way to to get into the ETF and index space. I use it as a means to save for my children as an alternative to the measly interest banks pay. But my left over change and regular contributions into it is beginning to mount up. What are your thoughts to it being a genuine and serious investment vehicle?

Hi Mav,

Thanks for the kind words. I’m glad you’re enjoying the blog mate.

50 IS the new 40 haha! As they say, you’re only as young as you feel. And tbh 50 is young. If you’re anywhere near retirement at 50 you’re killing it.

Now onto Acorns (Raiz). Firstly, I hate the new name, what were they thinking???

My opinion of Raiz is mainly a positive one. This is because they simplify the process of investing and provide a really slick system that encourages people to invest. There investing models is solid too plus they have very low management fees. I really like that they are promoting investing for young people in general.

Would I use them as a serious investment vehicle?

Nope.

I think they are a fantastic entry level investment vehicle and can show investors that investing is ‘cool’ and get you excited about it. But once you have grasped the concepts. There’s no real reason for you to be paying Raiz’s management fee on top of the ETFs that they are investing in.

This is often missed by investors. You’re not only paying Raiz management fee but also the underlying products they bundle with your investment package. In some cases, this means paying double the amount of fees for essentially a nice app, reports, and interface.

If you know how much you’re paying and still want to invest with them, no worries. They have a great platform.

And Kodus to you mate for teaching your kids about investing. Come to think of it. Raiz is perfect for teaching kids about investing because of the rounding feature and the nice app.

Your charts are awesome – I wish I kept something like that as well. It’s interesting you included HECS in your debt figure I have always kind of ignored it as it is indexed at inflation anyways bit I suppose it makes sense.