I publish these net worth updates to keep us accountable, have others critique our strategy and show that reaching financial independence in Australia is very doable without winning the lotto, having a high paying job or inheriting a wad of cash. The formula to be able to retire early is simple, the hard part is being consistent and sticking to a plan for many years. The table at the bottom details our entire journey from being $36K in debt all the way until we reach 🔥

And that’s a wrap for 2021!

It’s wild to think that we are already in 2022, just like that meme, I feel like I am still processing 2020 🤯

December was here and gone in a minute for the Firebug household. So many Christmas breakups, family gatherings on both sides, friends coming back to town for the festive season, birthdays, NYE events and so on.

We hosted the annual Christmas day breakfast at our new home this year too. I recently bought a new barbie (I’m obsessed) and really wanted to put it to work.

This is living 🙌😍

I basically have started to barbeque just about everything now. And when the weather is good, it’s damn hard not to crack open a beer. I’m usually pretty strict with alcohol on work nights but I don’t know what it is about barbequing that makes me break the rules. I might have to start buying some non-alcoholic beers to lessen the effect 😅

Mrs FB had a hectic finish for the school year (as is always the case), but is super pumped about dropping down to 4 days a week starting next year 🎉🥳.

2021 was such a whirlwind of a year and I’m stoked that we managed to tick off all the major items we had on our list like buying a house and tying the knot.

Thanks a lot to everyone who reads the blog/listens to the podcast. I’ve got some great ideas for AFB and the Aussie FIRE community in 2022 that I can’t wait to share with you all 👊

Net Worth Update

So we lumped summed ~$210K into the markets in late December/early January. This was surprisingly difficult for us to actually pull the trigger.

The general consensus in the FIRE community is to not get caught up in timing the market. This is easier said than done.

I’m human just like the rest of you and I also read a fair bit of finance mumbo jumbo content too. It’s fun to read opinion pieces and I’ll watch the occasional YouTube video of some doom and gloomer who has put together a pretty slick video with nice editing on why the next recession is about to drop.

The hardest part mentally was the markets being at an all-time high (or close to it). No matter how much I read that it doesn’t matter if you’re in it for the long term, it’s still bloody difficult not to wait for a dip.

So I waited right until the end of December before we invested our lump sum. And right on cue, the markets had a slight tumble afterwards 🙃🔫.

We would have been so much better off if I had just invested that money straight away but such is life. And the downturn right after we invested $210K is a major reason the net worth only grew by $2K in December. The other reason was a pretty expensive month.

The FIRE portfolio actually went down slightly in December due to the market dip after our big investment. December was really expensive for us too with Christmas/holidays.

*Expenses include everything we spend money on to maintain our lifestyle. We do not include paying down our PPoR loan as an expense, only the interest

*Investment income is simply 4% of our FIRE portfolio divided by 12

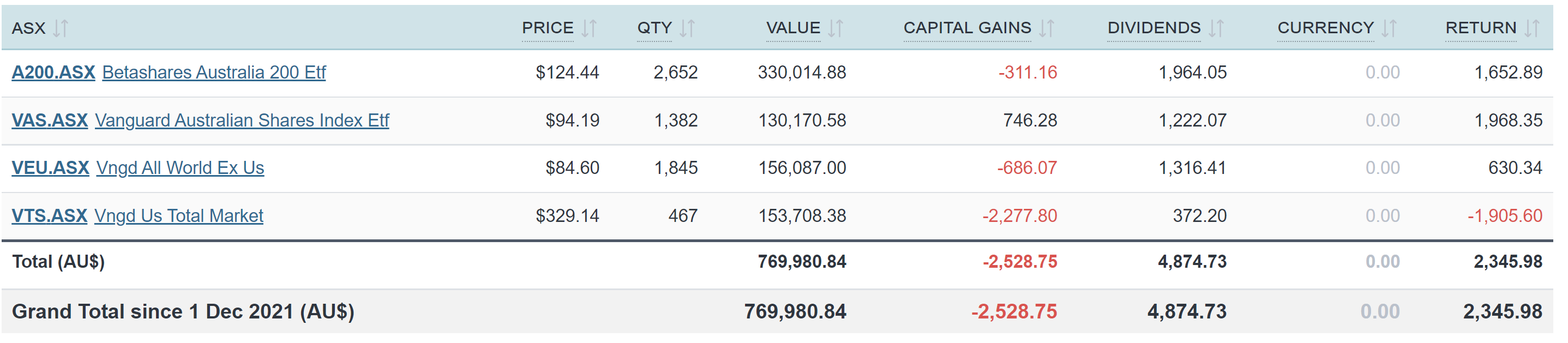

Shares

The above graph is created by Sharesight

We’re all in baby!

$769K all in shares which blows my mind!

Man… it wasn’t too long ago that I was in my mid 20’s and reading US FIRE blogs on a daily, dreaming about reaching financial independence someday in the future. I can’t remember whose blog I was reading but they had just hit $700K in shares and I remember being awestruck by the figure.

It just seemed like so much god damn money to have invested. I thought it was going to take me forever to get anywhere near that amount.

So to see $769K on the screen is a bit surreal to be honest.

But on the flip side, finally investing all that money felt like a weight off our shoulders. It’s in the market now so whatever happens, happens. If there’s a huge recession in 2022… well… that would suck but we’ve just accepted that and it’s back to business DCA’ing each month which is so much easier to do.

We made three huge (for us) purchases in December/early January.

- $53K into VTS

- $62K into VEU

- $95K into A200

This brings the portfolio into the following splits

60% Aussie 40% International

and

43% Betashares 57% Vanguard

Some of you hawkeye readers may have noticed that this is slightly different to our latest strategy explained article (2.5). I’m actually going to write another updated strategy explained article because our investing strategy is very fluid and changes based on our current circumstances and priorities.

There are no major reasons why we went with the splits above, it’s just what we feel comfortable with atm. We also like to spread the management risk around by having a decent chunk of our portfolio in Betashares and not just Vanguard. It also helps that A200 is cheaper than VAS atm too.

Looking forward to hitting the $800K mark in the not so distant future 😁

WOW,Just wow .

And congratulations

And so very impressive

And so very inspirational

Thank you 😊

No worries Richard. I’m glad you’re enjoying the updates 🙂

I have recently moved to Australia and after reading your blog I have started investing in Betashares A200.

I was also interested in VTS vs NDQ (More Tech Focussed but Higher fee and Australia Domiciled).

Do you think it could be gould investment for long term as Tech stocks are going through correction?

I honestly have no idea what tech stocks are going to do mate. I would lean towards them doing well but the truth is no one really knows long term I’m afraid.

Congratulations. Thank you for sharing and inspiring people like me to reach for the stars. Well done and all the best for 2022.

TYSM 🙏

Dude 10 years since you started working full-time. Pretty crazy to think what you have achieved in that period!

I know you won’t go another 10 years FT, but crazy anyway to speculate what you could do financially if you wanted to.

It feels like every other month you’re writing it has been an expensive one for you. Is your actual spending higher than your targeted spend?

Happy 2022!

It’s mental Dickrog. I can’t believe 10 years have already flown by 🤯.

Inflation has definitely taken a toll during the last 18 months. It’s been such a crazy year with the wedding and house that I’m not quite sure where our baseline is atm (it use to be around $4K a month). I’m keen to see where the tracking takes us in 2022.

G’day AFB,

Curious about your debt recycling strategy, would it have been better to pay the 210k off the home loan and then use the split loan to put into the market?

This is what we did do dude! There’s an article coming out that explains it all 🙂

Not going to lie. Buying a Weber BBQ is the 2nd best investment you can make. Alongside DCA into a good ETF like Vanguard each month 😂

Happy New Year, I love the great feelings that you get with the Summer months, BBQ’s and reaching your goals. Thank you for sharing all these years, it has been an inspiration and great way to learn about investing.

Thanks Andrea 🙂

Bro… the Weber is seriously the GOAT barbeque. It’s cooks EVERYTHING better 😂

Thought you mentioned in a podcast that you held some crypto too? Or was it that you were looking at putting some money into it?

We have a tiny bit of Crypto but we’re looking at buying some more… more updates on this to come

Wow! Hitting that buy button must have felt like the moment when the rollet coaster goes up the first big hill and stops for a second before the ride begins. Well done!

Yep! The heart rate was up during the click lol

It is amazing achievement and you are my favourite blogger and I learn so much from you, Yes, I could not believe that the amount invest in ETF. Luckily it is not share pick and I am terrible abut that. I finished my last property development last year and not going to do anymore. Too much hard work. Last year and I began to invest ETF after reading your blog, I built around $70000 and already scared me a lot to buy all the time high. But I need got used to DCA no matter market. Just want to say a big thank and your blog and podcast did amazing and encouraged people.

♥

That’s very kind of you to say Cynthia. It makes me really happy to hear that the AFB blog/podcast can pay the love forward and help out others just like MMM and Mad Fientist helped me out all those years ago.

Congrats on building your snowball and all the best for your journey.

Love the Weber and had a BabyQ for a decade, but found “Grill Grates” take it from good to exceptional with steak and salmon. Have a look 🙂

Just had a look… do they make that much of a difference?

What’s your favourite thing about them?

That is a big brave move, lump summing in $200k.

Kudos to putting your ‘buy’ orders where your overall convictions are about the right approach. As time progresses, the lower the chances that you’ll be every able to consider that the ‘wrong’ call, and all the sooner as the returns should start arriving more quickly.

Getting a proper barbeque is one of my pre-FI goals – you’ve inspired me to go and do some more research!

Cheers mate.

Lump summing is so much easier said than done haha. That’s the psychology at play I guess.

Dude… I did a LOT of research and I gotta say that the Weber came out on top. You’re probably better off setting a search up on Facebook marketplace and waiting for a second hand one. We had a voucher so I just went for it 🙂

Nice work man! Bet it feels good to be fully-invested in a shares-only portfolio. Also, totally with you on the lump sum… easier in theory than practice! Despite being reasonably experienced now, I still prefer the wimpy DCA approach 😉

p.s. Gotta compliment you on your pretty graphs too… my graph game is pretty sad lol.

What is DCA?

Dollar Cost Averaging…adding smaller amounts on a regular basis no matter the current market price. I.E. on a weekly or monthly basis.

It’s just a good habit to follow otherwise you try timing the market and then feel frustrated if you wait then miss it! Or, the market doesn’t dip for sometime. Also, it helps avoid that feeling of regret when putting a large sum in and the market drops! (Though, nine times out of ten a lump sum is the way to go as you have more in the market!)

With lump sums I tend to DCA it in over (many) weeks on a daily basis. If the market does drop by more than 1% then I often double up on that daily investment. I just set up my daily payments with Bpay, with the payments going into my super in advance, then on down days just double up by logging into my bank account and make a second deposit…easy peasy.

Aren’t your gains being eaten up by fees immediately?

Cheers mate!

Yep, scary as shit no matter how much conviction I have lol.

Check out Google graphs if you want free visuals… there’s a little bit of coding behind it though 🤓.

Hey AFB,

Love your work. Quick question, do you know how CGT will work for the the SOL shares you sold a few months ago? Will you have to pay CGT from when you bought MLT up till the merger? I am looking to sell SOL and want to see if it is worth it.

Thanks!

I’m not 100% sure about that. I’ll probably work it out with my accountant at the end of this FY.

congrats. could I also suggest you look into your happiness level. By happiness I mean contented happiness not LOL. Try to track this on your journey to FI. I have seen and met many materially rich folk who are onto their third marriage etc and wonder is this what they aspired to when they were young, idealistic and looking forward to growing up. I think most forget what their aspirations were, hence the position they’re in. BTW could I suggest you buy a coffee machine to go with your BBQ. Such a luxury especially on rainy days when you want a good coffee and don’t want to leave your house.

This is a great idea Pete!

You’re so right about wealthy people being miserable… I mean… what’s the point in that?

I’m more of a tea drinker myself but I love the smell of coffee in the morning.

Wow, congratulations!! This is really inspiring. What a great position to be in before starting a family.

Cheers Mari

Weber Q’s are the best!

PREACH!

I feel you on the lump sum. I’ve been holding a chunk for 6 months now!

I know when I finally pull the trigger I’ll be hitting refresh every 30 seconds haha

Haha we all go through it 😬

Bloody wonderful BBQ weather though isn’t it! Used my new one today to cook up some burgers for lunch!

Good to see you didn’t take too long to just bite the bullet and drop that cash in! It’s done now!

Everyday is a barbeque at our house atm lol

Happy new year mate!, what a massive 12 months it was for you guys! Nice to see the net worth continue to tick up, and congratulations on taking the plunge with the lump sum into the market!

That’s a pretty healthy looking feed on the BBQ, reckon you might need to up the quantities a bit though!

I think he was DCA’ing the sausages, to be honest 😉

lol

Cheers boss.

Rest assured we had some scalloped potatoes on the table outside of this shot 😁

I have always thought that PPOR should be excluded from net worth?

AFB you will need to get a FAQ going for Q’s like this I think, and add it to the start of every Net Worth Update.

Haha yeah I might need to

Well done and keep up the great work, I really appreciate you sharing and I have gained a Lot from your pods, thankyou!

Re beers, I have been home brewing for many years and it has saved me Thousands

No worries Liquid.

I’ve had a few home brews from mates. Some were great, others were… ah… not so great 🤮 lol

I might have to look into it one day

Wow!!! You are inspiring me more to stay invested. 😊. Happy 2022 AFB family !!!!

Time in the market Roweliza 💪

If you really want to go down the rabbit hole of BBQ, get a smoker. You’ll never look back.

Almost a certainty. I’ll focus on mastering the BBQ for now 🙂

Lol, smoking is BBQ. (I’m not talking about cold smoking). Ditch the gas and cook with a real fire. I recommend you try eating some at your local BBQ smokehouse (I’m sure Sydney has plenty) 🙂